There is a unique paradox sitting at the heart of how the mining industry evaluates its projects. It’s called the Inferred Resource—now you see it, now you don’t.

A company can publish a Preliminary Economic Assessment (PEA) showing a mine life, a robust internal rate of return, and a strong net present value. That study can be based on mineral resources that regulators consider too geologically uncertain to support a production decision. These are the infamous Inferred resources: tonnes, grades, and dollars in the economic model, yet with a classification that effectively flags them as educated guesses. The PEA rules permit their inclusion because early-stage projects need a way to test whether chasing more resource certainty is worth the additional cost.

The paradox occurs when that same project advances to the pre-feasibility (PFS) or feasibility (FS) stage. Suddenly the Inferred ore tonnes are gone; they are now waste rock. The mine plan must be based on more certain Measured and Indicated resources. Theoretically, the life-of-mine production profile that looked compelling in the PEA may now shrink—so the NPV and IRR might shrink too. Nothing has gone wrong in any technical sense. The project simply requires a higher standard of certainty now.

Potentially, some investors who focused on the PEA economics may feel the subsequent feasibility study is a disappointment (especially if costs have also escalated). They’ll say the PEA is garbage. In reality, the project has moved from an aspirational study (i.e., the PEA) toward a bank-financeable study. To compensate for the loss of Inferred material, companies will rely of step out drilling to grow the resource to maintain size.

What Are Inferred Resources?

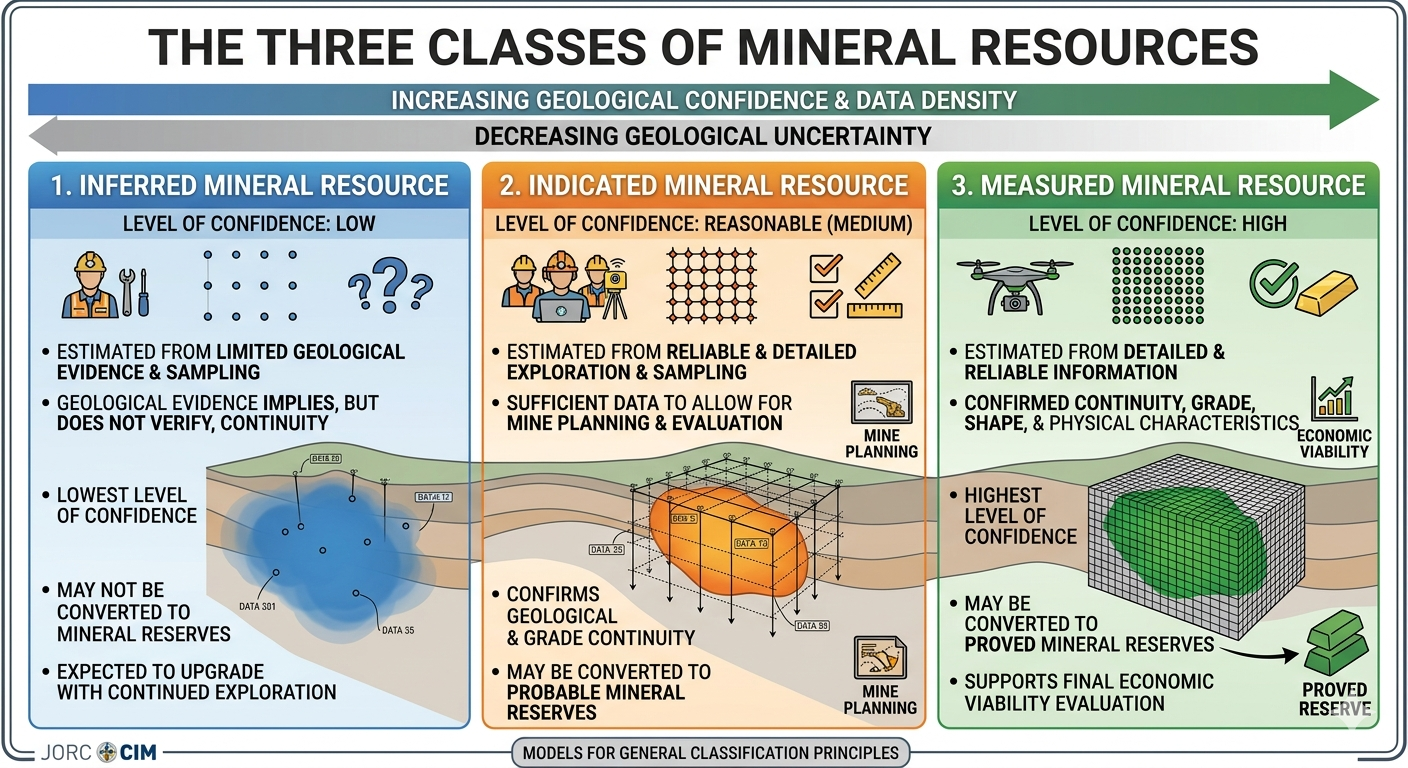

Inferred resources represent the lowest confidence category of mineral resources; typically estimated in zones with limited sampling and unconfirmed geological continuity. They carry the highest geological uncertainty of the three resource categories.

Inferred resources represent the lowest confidence category of mineral resources; typically estimated in zones with limited sampling and unconfirmed geological continuity. They carry the highest geological uncertainty of the three resource categories.

In Preliminary Economic Assessments (PEAs), Inferred resources are allowed—but only under certain conditions:

-

They can be included in mine plans and economic models, which is the reason PEAs exist: to allow early-stage projects to test economic viability using all available resource data.

-

However, any PEA that includes Inferred resources cannot be used to support a production decision and must carry prominent cautionary language. Under NI 43-101, the technical report must explicitly state that the PEA is preliminary in nature, that Inferred resources are too speculative geologically to have economic considerations applied, and that there is no certainty the PEA will be realized. (It seems a PEA without Inferred resources can be used to support a production decision.)

-

Inferred tonnes are routinely used to extend mine life or improve project economics in PEA studies. Investors must understand this risk and should examine the proportion of mined tonnage that is classified as Inferred. This breakdown is normally presented in the Technical Report.

Conversely, in Pre-Feasibility Studies (PFS) and Feasibility Studies (FS), the rules for Inferred material are different:

-

Inferred resources cannot be included in mineral reserve estimates or in the economic analysis underpinning a PFS or FS. Inferred “ore” is treated as waste rock.

-

Only Indicated and Measured resources can be converted to Probable and Proven mineral reserves.

-

Including Inferred material in a PFS mine plan would typically disqualify the study from being used for project financing or a production decision.

-

Some companies might include Inferred material in a PFS as “upside” or as a sensitivity case, but that analysis must be clearly distinguished from the base case.

The resource upgrade requirement (from Inferred to Indicated) creates some interesting dynamics:

-

Companies may need additional funds to drill sufficiently to upgrade the resource before advancing to the PFS/FS stage. The cost and time for this infill drilling can be a major driver of exploration spending and can delay project timelines. Mining projects can take a long time to develop, and this is one reason why.

-

Companies will look at ways to compensate for the Inferred material deduction. Cutoff grade changes and step out drilling are ways to mitigate this impact.

-

A large Inferred resource that cannot be upgraded without great cost (due to depth, remoteness, or lack of ore-zone continuity) can permanently stall a project at the PEA stage. Hence, one may see multiple PEAs completed on the same project (i.e., the PEA loop).

-

In closing, the peculiarity of the Inferred resource is that it is essentially a tiered permission structure. Inferred resources are useful for early economic screening, but they must be converted to higher-confidence categories before they can support a bankable study or project debt financing.

Permitting via a PEA

Companies sometimes will commence the permitting process based on their PEA study. There are some risks to doing this, and the Inferred resource creates one of these risks.

Companies sometimes will commence the permitting process based on their PEA study. There are some risks to doing this, and the Inferred resource creates one of these risks.

With limited capital, a junior miner may not be able to afford the $5–20 million cost of a full feasibility study before determining whether a project is even permittable. A PEA, costing a fraction of a FS, can provide enough technical substance to engage regulators and begin the environmental baseline work that must precede any formal permit application.

Baseline studies for hydrology, ecology, and air quality typically require two to three years of data collection. So starting early makes sense, even with only a PEA-level project layout in hand.

Permitting and ongoing technical study work will run in parallel on most projects. Waiting for a completed FS before starting permitting would add years to the project timeline. Companies routinely will concurrently advance environmental impact assessments, indigenous consultation, and baseline data collection with subsequent PFS and FS work.

Jurisdiction may play a role too. Some areas are more receptive to early-stage permitting engagement. Other permitting processes may be more rigorous such that operators want at least a PFS in hand before committing to a full EIA process.

Now, with respect to the Inferred resource, the risk is that a project permitted around a PEA-scale footprint may shrink in size at the feasibility stage. Some reasons for this size reduction will be discussed in a future blog post, as well as the ways companies avoid this with ever increasing ore tonnage. Project shrinkage can result in a company acquiring permits and bonding for a proposed mine plan that no longer exists.

How Can Inferred Resources Affect Permitting

Let us examine some specific aspects of permitting that can be influenced by Inferred resources.

Let us examine some specific aspects of permitting that can be influenced by Inferred resources.

1. Project Footprint and Disturbance Area: Permits are issued for a defined physical footprint, consisting of pit limits, waste dumps, tailings facilities, and infrastructure corridors. If a PEA mine plan is inflated by Inferred tonnes and defines a large footprint versus the feasibility study, the company faces a choice:

(a) Permit the smaller FS footprint and risk under-permitting if Inferred is later upgraded. Requesting future permit modification for a suddenly larger project is sometimes viewed by regulators as “permitting by stealth”.

(b) Permit the larger PEA footprint to provide flexibility, which may trigger more extensive environmental review and higher bonding requirements.

2. Environmental Impact Assessment (EIA) Scope & Cost: A mine plan that includes Inferred material:

– May define a larger disturbance envelope, larger waste dumps, larger tailings facility, all of which require assessment of broader habitat, hydrology, and community impacts. Perhaps the project must advance into a new watershed. This can add permitting cost and time. If the Inferred material is later excluded, the assessment work may have been unnecessarily extensive.

3. Tailings and Waste Facility Sizing: Tailings storage facilities (TSFs) and waste rock dumps are sized to the life-of-mine tonnage. Inferred tonnes included in a PEA can drive facility sizing significantly. Permitting a TSF for a larger tonnage is:

– More difficult and time-consuming to obtain if the height and footprint increase

– Will be subject to more rigorous dam safety and closure review- However this could be potentially beneficial if the Inferred resource is later confirmed during mining

Conversely, I have seen situations where permitting was done on the pre-feasibility level design, thereby excluding Inferred ore from the plan. The operability of a planned co-disposal waste facility relied on relative ratios of clean waste rock, acid generating rock, and tailings. During production, the conversion of Inferred material from “waste” to “ore” would mean more tailings, less waste rock, and could shift the required material balance for co-disposal in a negative way. Permitting based on a PEA might make more sense here.

4. Financial Assurance and Reclamation Bonding: Regulators require bonds or financial assurances sized to the cost of full site reclamation. A larger mine footprint driven by Inferred tonnes means:

– Higher bonding requirements

– Larger financial burden on the company during the project development phase

– Potential difficulty for junior companies in securing bonds for Inferred-inflated footprints that have not been proven out yet.

5. Water Licences and Discharge Permits: Water use and discharge volumes scale with throughput and mine life. A longer mine life driven by Inferred tonnes may require expanded water licences. If those tonnes are later excluded, the licence may be oversized. Keep in mind that obtaining an amendment to increase a water licence later can be harder than acquiring a larger one initially, so there is a trade-off here.

6. Indigenous and Community Consultation: In jurisdictions with consultation requirements (Canada’s duty to consult, FPIC principles, etc.), the scope of consultation is tied to the project’s impact footprint and duration. A mine life extended by Inferred tonnes:

– Triggers consultation over a longer operational period

– May affect benefit agreement negotiations (royalties, employment commitments) tied to mine life or total tonnage

– If mine life subsequently shrinks at FS stage, it can create credibility and trust issues with communities who were counting on a longer mine life.

In closing, personally I feel that project proponents should try to permit to a footprint somewhat larger than the Pre-Feasibility base case to preserve operation flexibility. For more on the benefits of flexibility, see the blog post “Mining’s Obsession with Optimization – Good or Bad”.

Conclusion

Inferred resources present a unique paradox; they can and can’t be used in mining economic analysis. They can be used to examine project viability but can’t be used to make a production decision.

Inferred resources present a unique paradox; they can and can’t be used in mining economic analysis. They can be used to examine project viability but can’t be used to make a production decision.

The manner in which Inferred resources are viewed can also affect permitting. Although they don’t directly enter the regulatory process, they can shape the physical parameters of the mine plan that regulators will evaluate.

Even if a company grows the resource size between the PEA and PFS, there will still be a component of Inferred material within the PFS mine design that might be considered real tonnage or not.

Getting the permitted footprint right relative to the eventual resource confidence level is an underappreciated skill in project development. Each mining project is unique, and there is no easy one-size fits all solution when considering the impact of Inferred resources on project development.

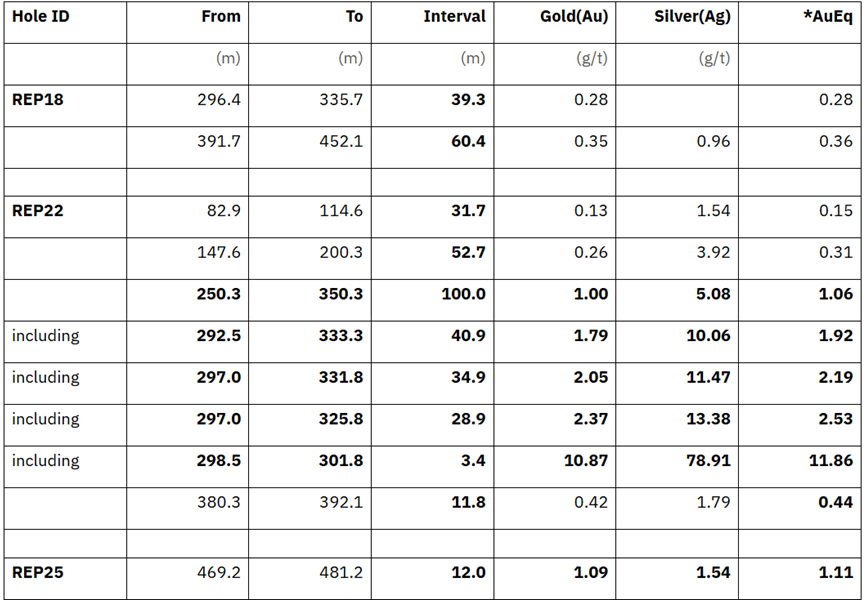

Recently I have been reviewing a few mining projects from an investor’s perspective. This led me to wonder whether junior mining companies should share more than just their drill hole highlights. What about the raw assays? A mining company announces highlighted drill intervals, but what exactly do those numbers represent?

Recently I have been reviewing a few mining projects from an investor’s perspective. This led me to wonder whether junior mining companies should share more than just their drill hole highlights. What about the raw assays? A mining company announces highlighted drill intervals, but what exactly do those numbers represent? There is a sense that many mining investors are becoming more sophisticated, and they want to fully understand the exploration process.

There is a sense that many mining investors are becoming more sophisticated, and they want to fully understand the exploration process.

1. Misinterpretation & “Amateur” Experts: One risk is that someone with a very basic understanding of mining software and limited understanding of the local geology, runs flawed interpretations and publicizes their incorrect conclusions. A company may find that correcting false narratives publicly can be harder than preventing them.

1. Misinterpretation & “Amateur” Experts: One risk is that someone with a very basic understanding of mining software and limited understanding of the local geology, runs flawed interpretations and publicizes their incorrect conclusions. A company may find that correcting false narratives publicly can be harder than preventing them. Once the assay data is public, it may be more difficult for a company to manage the story. A press release lets them frame results in the context of their business plan; a raw data file does not.

Once the assay data is public, it may be more difficult for a company to manage the story. A press release lets them frame results in the context of their business plan; a raw data file does not. For investors trying to assess a junior explorer, or geologists conducting a technical review, or a regulator trying to ensure fair and accurate disclosure, access to raw assay data can play a part in promoting good judgment and accurate disclosure from companies.

For investors trying to assess a junior explorer, or geologists conducting a technical review, or a regulator trying to ensure fair and accurate disclosure, access to raw assay data can play a part in promoting good judgment and accurate disclosure from companies.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening. USER PROMPT: What are the risks of toll milling plan.

USER PROMPT: What are the risks of toll milling plan. RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia.

RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia. The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

The lesson is that QP’s signing off on technical information for clients should be proficient in the nature of their work and need to know the reporting rules very well. Some of these incidents involve error and poor judgment, not outright fraud.

The lesson is that QP’s signing off on technical information for clients should be proficient in the nature of their work and need to know the reporting rules very well. Some of these incidents involve error and poor judgment, not outright fraud. 43-101 regulations state that “An issuer must not file a technical report that contains a disclaimer by any qualified person responsible for preparing or supervising the preparation of all or part of the report that

43-101 regulations state that “An issuer must not file a technical report that contains a disclaimer by any qualified person responsible for preparing or supervising the preparation of all or part of the report that This ends Part 2 of this blog post. It hopefully highlights the importance of QP’s being knowledgably on the disclosure rules and the technical aspects of what they are hired to do.

This ends Part 2 of this blog post. It hopefully highlights the importance of QP’s being knowledgably on the disclosure rules and the technical aspects of what they are hired to do. The focus of this blog is on the types of activities that raised the red flags in the past. I am less interested in naming the people responsible, although the associated web links do provide more detail on the events.

The focus of this blog is on the types of activities that raised the red flags in the past. I am less interested in naming the people responsible, although the associated web links do provide more detail on the events. This ends Part 1 of this blog post. Part 2 will continue with a few more examples, specifically involving Qualified Persons, and can be found at this link

This ends Part 1 of this blog post. Part 2 will continue with a few more examples, specifically involving Qualified Persons, and can be found at this link

So, you just completed your initial PEA cashflow model and the resulting NPV and IRR are a little disappointing. They are not what everyone was expecting. They don’t meet the ideal targets of an IRR greater than 30% and an NPV that is more than 2x the initial capital cost. The project could now be on life support in the eyes of some.

So, you just completed your initial PEA cashflow model and the resulting NPV and IRR are a little disappointing. They are not what everyone was expecting. They don’t meet the ideal targets of an IRR greater than 30% and an NPV that is more than 2x the initial capital cost. The project could now be on life support in the eyes of some. The discounting of cashflows in a cashflow model means that up-front revenues and costs have a bigger impact on the final economics than those far off in the future. This effect is amplified at higher discount rates.

The discounting of cashflows in a cashflow model means that up-front revenues and costs have a bigger impact on the final economics than those far off in the future. This effect is amplified at higher discount rates. ake to the cashflow model. Sometimes several of the small ones, when compounded together, will result in a significant impact. Here are some of the other cashflow model adjustments that I have seen.

ake to the cashflow model. Sometimes several of the small ones, when compounded together, will result in a significant impact. Here are some of the other cashflow model adjustments that I have seen. Don’t let a disappointing NPV get you down. There may be a few ways to boost the NPV by applying some common practices. However, if after applying all of these adjustments, the NPV still isn’t great, something bigger may be required. That could be an entire project scope re-think.

Don’t let a disappointing NPV get you down. There may be a few ways to boost the NPV by applying some common practices. However, if after applying all of these adjustments, the NPV still isn’t great, something bigger may be required. That could be an entire project scope re-think.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times. Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its service, smoothing the ore delivery to the plant.

Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its service, smoothing the ore delivery to the plant. Once the schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

Once the schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate. These two blog posts hopefully give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

These two blog posts hopefully give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

So I thought what better way to explain the mining engineer role than by describing the anatomy of a typical Chapter 16 (MINING) in a 43-101 Technical Report. That chapter is a good example of the range of tasks typically undertaken by mining engineers.

So I thought what better way to explain the mining engineer role than by describing the anatomy of a typical Chapter 16 (MINING) in a 43-101 Technical Report. That chapter is a good example of the range of tasks typically undertaken by mining engineers. There is always a mineral resource estimate available before doing a PEA. The way the resource is reported will indicate what type of mine this likely is. The geologists have already done some of the mining engineer’s work.

There is always a mineral resource estimate available before doing a PEA. The way the resource is reported will indicate what type of mine this likely is. The geologists have already done some of the mining engineer’s work. Before starting pit optimization, we require economic inputs from several people. The base case metal prices must be selected (normally with input from the client). The mining operating cost per tonne must be estimated (by the mining engineer). The processing engineers will provide the processing cost and recovery for each ore type.

Before starting pit optimization, we require economic inputs from several people. The base case metal prices must be selected (normally with input from the client). The mining operating cost per tonne must be estimated (by the mining engineer). The processing engineers will provide the processing cost and recovery for each ore type. Once the optimization is run, a series of nested pit shells are created, each with its own tonnes and grade. These shells are compared for incremental strip ratio, incremental head grade, total tonnes, and contained metal.

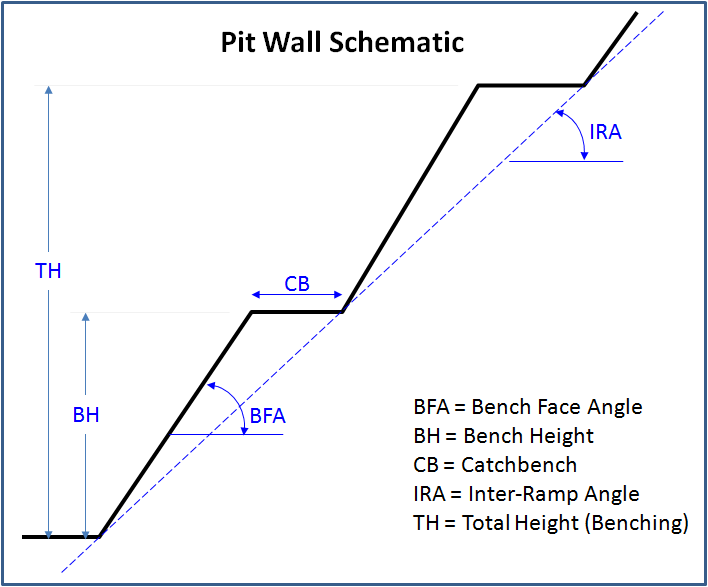

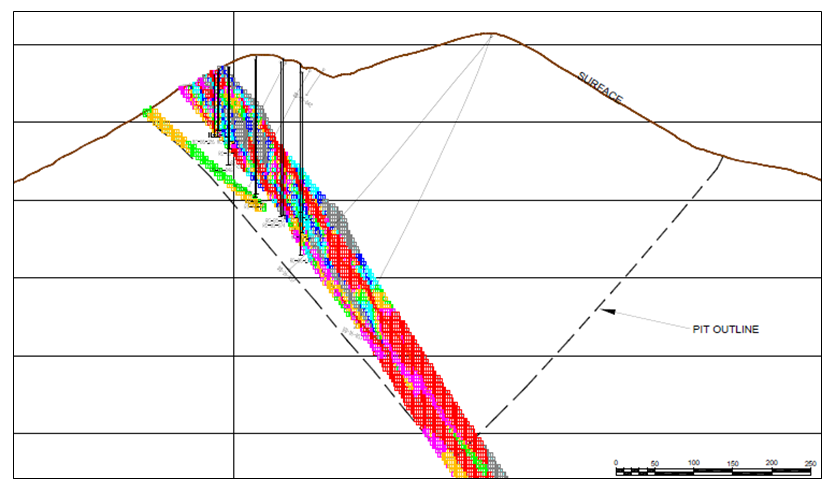

Once the optimization is run, a series of nested pit shells are created, each with its own tonnes and grade. These shells are compared for incremental strip ratio, incremental head grade, total tonnes, and contained metal. The mining engineer is now ready to undertake the pit design. The pit design step introduces a benched slope profile, smooths out the pit shape, and adds haulroads. Hence a couple of key input parameters are required at this time. The mining engineer will need to know the geotechnical pit slope criteria and the truck size & haul road widths. Let’s look at both of these.

The mining engineer is now ready to undertake the pit design. The pit design step introduces a benched slope profile, smooths out the pit shape, and adds haulroads. Hence a couple of key input parameters are required at this time. The mining engineer will need to know the geotechnical pit slope criteria and the truck size & haul road widths. Let’s look at both of these.

Ramps: Next the mining engineer needs to select the truck size, even though the production schedule has not yet been created.

Ramps: Next the mining engineer needs to select the truck size, even though the production schedule has not yet been created.

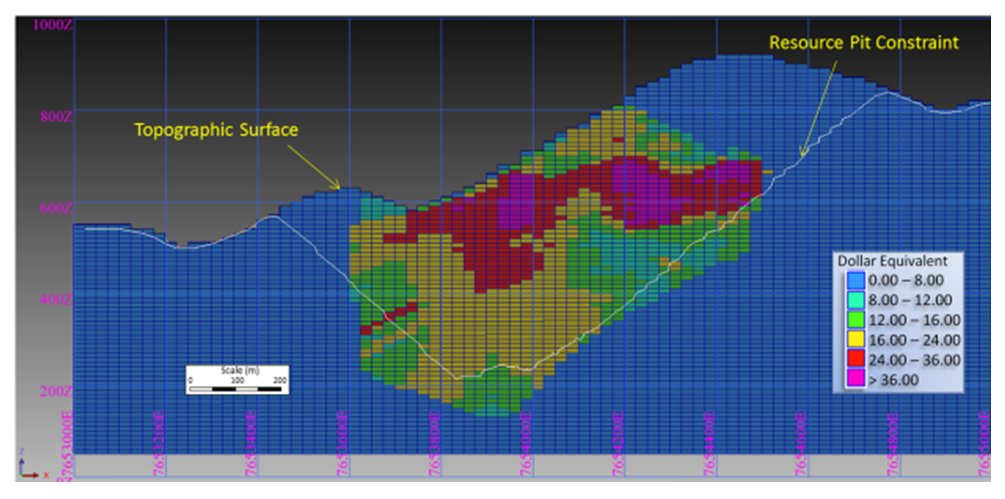

This article is about the benefit of preparing (cutting) more geological cross-sections and the value they bring.

This article is about the benefit of preparing (cutting) more geological cross-sections and the value they bring. Long sections are aligned along the long axis of the deposit. They can be vertically oriented, although sometimes they may be tilted to follow the dip angle of an ore zone.

Long sections are aligned along the long axis of the deposit. They can be vertically oriented, although sometimes they may be tilted to follow the dip angle of an ore zone. When looking at cross-sections, it is always important to look at multiple cross-sections across the orebody. Too often in reports one may be presented with the widest and juiciest ore zone, as if that was typical for the entire orebody. It likely is not typical.

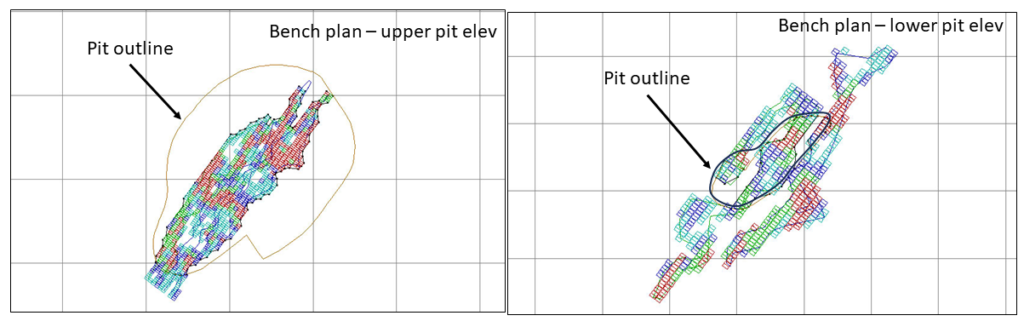

When looking at cross-sections, it is always important to look at multiple cross-sections across the orebody. Too often in reports one may be presented with the widest and juiciest ore zone, as if that was typical for the entire orebody. It likely is not typical. Bench plans (or level plans) are horizontal slices across the ore body at various elevations. In these sections one is looking down on the orebody from above.

Bench plans (or level plans) are horizontal slices across the ore body at various elevations. In these sections one is looking down on the orebody from above. 3D PDF files can be created by some of the geological software packages. They can export specific data of interest; for example topography, ore zone wireframes, underground workings, and block model information. These 3D files allows anyone to rotate an image, zoom in as needed and turn layers off and on.

3D PDF files can be created by some of the geological software packages. They can export specific data of interest; for example topography, ore zone wireframes, underground workings, and block model information. These 3D files allows anyone to rotate an image, zoom in as needed and turn layers off and on. The different types of geological sections all provide useful information. Don’t focus only on cross-sections, and don’t focus only on one typical section. Create more sections at different orientations to help everyone understand better.

The different types of geological sections all provide useful information. Don’t focus only on cross-sections, and don’t focus only on one typical section. Create more sections at different orientations to help everyone understand better.

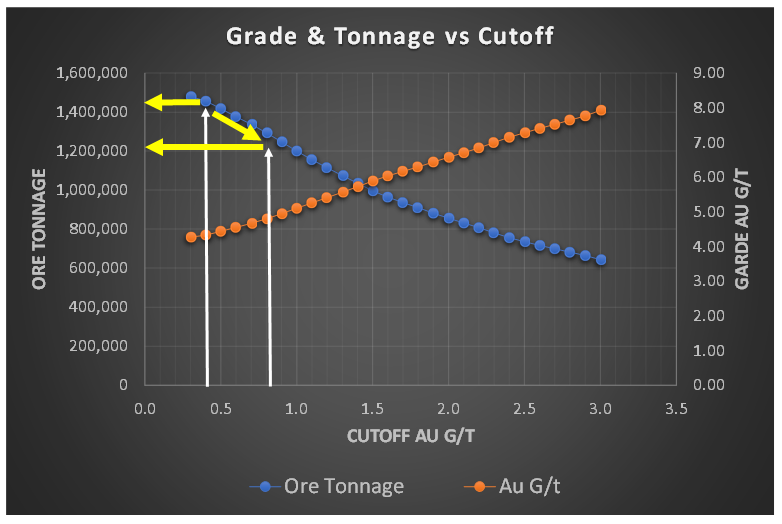

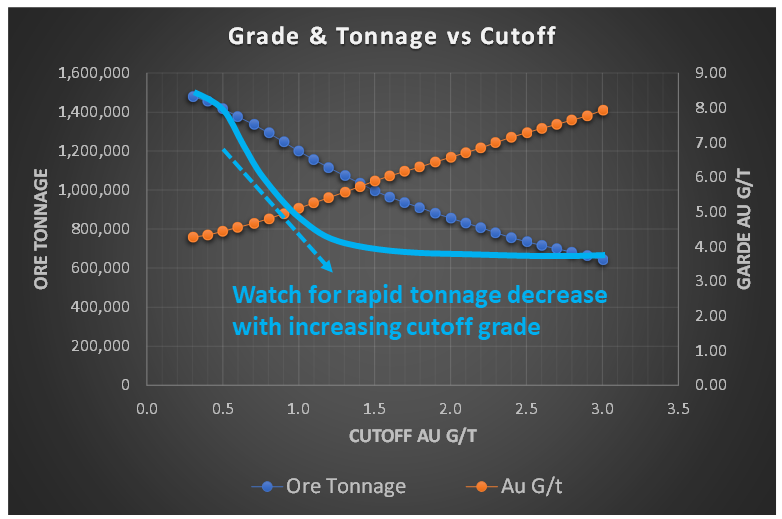

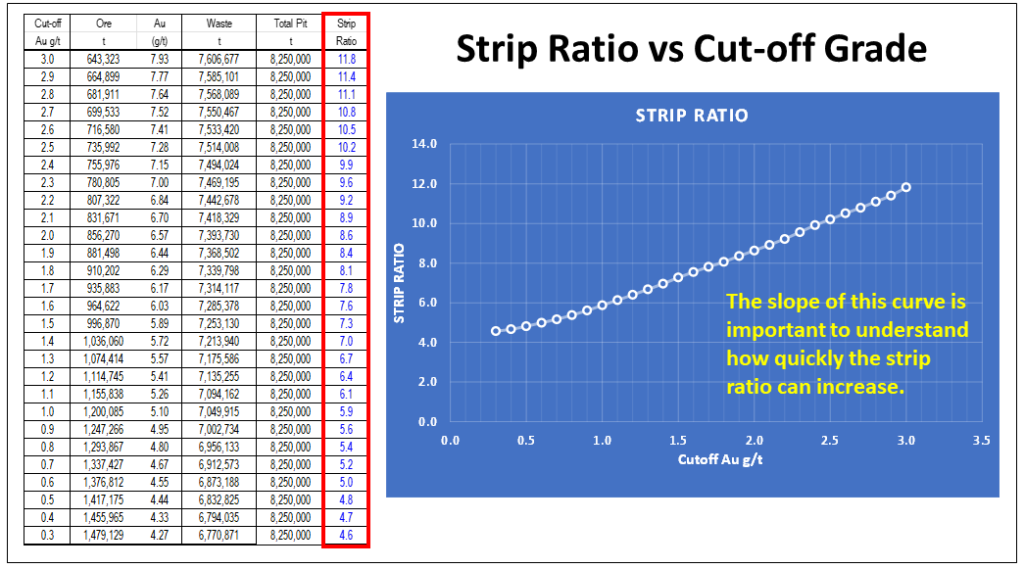

When I am undertaking a due diligence review or working on a study, very early on I like to have a look at the grade-tonnage information. This could be for the entire deposit resource, within a resource constraining shell, or in the pit design.

When I am undertaking a due diligence review or working on a study, very early on I like to have a look at the grade-tonnage information. This could be for the entire deposit resource, within a resource constraining shell, or in the pit design. However, if the tonnage curve profile resembled the light blue line in this image, with a concave shape, the ore tonnage is decreasing rapidly with increasing cutoff grade. This is generally not a favorable situation.

However, if the tonnage curve profile resembled the light blue line in this image, with a concave shape, the ore tonnage is decreasing rapidly with increasing cutoff grade. This is generally not a favorable situation. Regarding mineral resources, one should be required to disclose the waste tonnage and strip ratio when reporting resources inside a constraining shell. The constraining shell and cutoff grade are both based on defined economic factors such as unit mining costs, processing cost, process recoveries, and metal prices. With respect to the mining cost component, the strip ratio is a key aspect of the total mining cost, yet it normally isn’t disclosed.

Regarding mineral resources, one should be required to disclose the waste tonnage and strip ratio when reporting resources inside a constraining shell. The constraining shell and cutoff grade are both based on defined economic factors such as unit mining costs, processing cost, process recoveries, and metal prices. With respect to the mining cost component, the strip ratio is a key aspect of the total mining cost, yet it normally isn’t disclosed. In 43-101 technical reports, the financial Chapter 22 normally presents the project sensitivities expressed in a spider diagram or a table format.

In 43-101 technical reports, the financial Chapter 22 normally presents the project sensitivities expressed in a spider diagram or a table format.