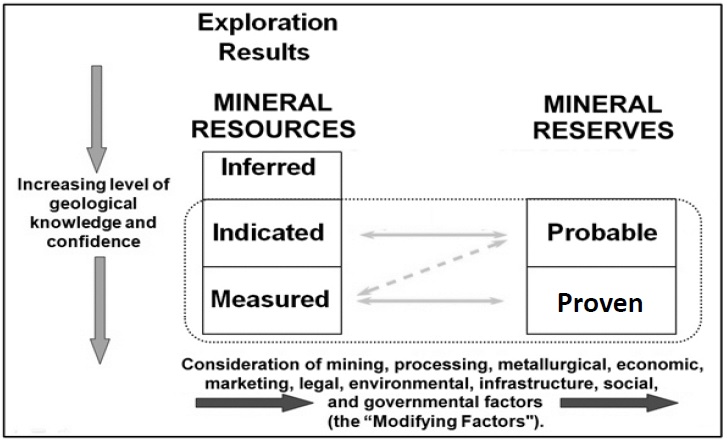

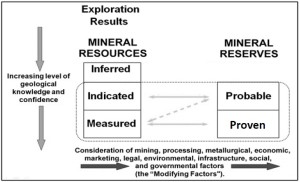

One of the first things we normally look at when examining a resource estimate is how much of the resource is classified as Measured or Indicated (“M+I”) compared to the Inferred tonnage. It is important to understand the uncertainty in the estimate and how much the Inferred proportion contributes. Having said that, I think we tend to focus less on the split between the Measured and Indicated tonnages.

Inferred resources have a role

We are all aware of the regulatory limitations imposed by Inferred resources in mining studies. They are speculative in nature and hence cannot be used in the economic models for pre-feasibility and feasibility studies. However Inferred resource can be used for production planing in a Preliminary Economic Assessment (“PEA”).

Inferred resources are so speculative that one cannot legally add them to the Measure and Indicated tonnages in a resource statement (although that is what everyone does). I don’t really understand the concern with a mineral resource statement if it includes a row that adds M+I tonnage with Inferred tonnes, as long as everything is transparent.

When a PEA mining schedule is developed, the three resource classifications can be combined into a single tonnage value. However in the resource statement the M+I+I cannot be totaled. A bit contradictory.

Are Measured resources important?

It appears to me that companies are more interested in what resource tonnage meets the M+I threshold but are not as concerned about the tonnage split between Measured and Indicated. It seems that M+I are largely being viewed the same. Since both Measured and Indicated resources can be used in a feasibility economic analysis, does it matter if the tonnage is 100% Measured (Proven) or 100% Indicated (Probable)?

The NI 43-101 and CIM guidelines provide definitions for Measured and Indicated resources but do not specify any different treatment like they do for the Inferred resources.

Relationship between Mineral Reserves and Mineral Resources (CIM Definition Standards).

Payback Period and Measured Resource

In my past experience with feasibility studies, some people applied a rule-of-thumb that the majority of the tonnage mined during the payback period must consist of Measure resource (i.e. Proven reserve).

The goal was to reduce project risk by ensuring the production tonnage providing the capital recovery is based on the resource with the highest certainty.

Generally I do not see this requirement used often, although I am not aware of what everyone is doing in every study. I realize there is a cost, and possibly a significant cost, to convert Indicated resource to Measured so there may be some hesitation in this approach. Hence it seems to be simpler for everyone to view the Measured and Indicated tonnages the same way.

Conclusion

NI 43-101 specifies how the Inferred resource can and cannot be utilized. Is it a matter of time before the regulators start specifying how Measured and Indicated resources must be used? There is some potential merit to this idea, however adding more regulation (and cost) to an already burdened industry would not be helpful.

Perhaps in the interest of transparency, feasibility studies should add two new rows to the bottom of the production schedule. These rows would show how the annual processing tonnages are split between Proven and Probable reserves. This enables one to can get a sense of the resource risk in the early years of the project. Given the mining software available today, it isn’t hard to provide this additional detail.

Note: If you would like to get notified when new blogs are posted, then sign up on the KJK mailing list on the website. Otherwise I post notices on LinkedIn, so follow me at: https://www.linkedin.com/in/kenkuchling/.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars. Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members.

Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members. Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there.

Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there. As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

The number of independent mining consultants is increasing daily as more people reach retirement age or are made redundant.

The number of independent mining consultants is increasing daily as more people reach retirement age or are made redundant. GLG (

GLG ( Digbee (

Digbee (

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due.

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due. I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play.

I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play. Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now.

Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now. It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

It’s always open to debate who these 43-101 technical reports are intended for. Generally we can assume correctly that they are not being written mainly for geologists. However if they are intended for a wider audience of future investors, shareholders, engineers, and C-suite management, then (in my view) greater focus needs to be put on the physical orebody description.

It’s always open to debate who these 43-101 technical reports are intended for. Generally we can assume correctly that they are not being written mainly for geologists. However if they are intended for a wider audience of future investors, shareholders, engineers, and C-suite management, then (in my view) greater focus needs to be put on the physical orebody description. I would like to suggest that every technical report includes more focus on the operational aspects of the orebody.

I would like to suggest that every technical report includes more focus on the operational aspects of the orebody. Improving the quality of information presented to investors is one key way of maintaining trust with investors. Accordingly we should look to improve the description of the mineable ore body for everyone. In many cases it is the key to the entire project.

Improving the quality of information presented to investors is one key way of maintaining trust with investors. Accordingly we should look to improve the description of the mineable ore body for everyone. In many cases it is the key to the entire project.

In the past there would be binders with detailed calculations and backup for the different parts of the study. Typically there was a binder for the Executive Summary and separate sections (i.e. binders) for Geology, Mining, Processing, Infrastructure, Capital Cost, Operating Cost, Environmental, Project Execution, and Economic Analysis, etc.

In the past there would be binders with detailed calculations and backup for the different parts of the study. Typically there was a binder for the Executive Summary and separate sections (i.e. binders) for Geology, Mining, Processing, Infrastructure, Capital Cost, Operating Cost, Environmental, Project Execution, and Economic Analysis, etc. The original intent of the 43-101 Technical Report was for it to be a summary document, only about 80-150 pages in length. The intent was to simplify all the technical work for the benefit of non-technical investors. Currently I have noticed that in many cases the 43-101 report is now the entire feasibility study document.

The original intent of the 43-101 Technical Report was for it to be a summary document, only about 80-150 pages in length. The intent was to simplify all the technical work for the benefit of non-technical investors. Currently I have noticed that in many cases the 43-101 report is now the entire feasibility study document. My recommendation is that, where budgets permit, mining companies return to the days of preparing the comprehensive feasibility study document. It’s the right thing to do.

My recommendation is that, where budgets permit, mining companies return to the days of preparing the comprehensive feasibility study document. It’s the right thing to do. If any mining industry credibility has been lost, re-establishing it should be important. One way to start doing this is to focus on creating the type of reports that best serve the needs of the industry stakeholders.

If any mining industry credibility has been lost, re-establishing it should be important. One way to start doing this is to focus on creating the type of reports that best serve the needs of the industry stakeholders.

I am not going into detail on Paul’s paper, however some of my key takeaways are as follows. Download the paper to read the rationale behind these ideas.

I am not going into detail on Paul’s paper, however some of my key takeaways are as follows. Download the paper to read the rationale behind these ideas. The bottom line is that not everyone will necessarily agree with all the conclusions of Paul’s paper on underground dilution. However it does raise many issues for technical consideration on your project.

The bottom line is that not everyone will necessarily agree with all the conclusions of Paul’s paper on underground dilution. However it does raise many issues for technical consideration on your project.

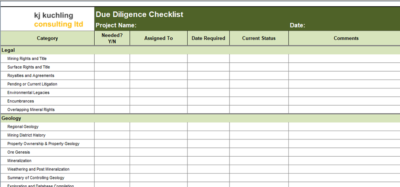

You a create your own checklist but if you would like a copy of mine just email me at KJKLTD@rogers.com and let me know a bit about how you plan to use it (for my own curiosity). Specify if you would prefer the Excel or PDF versions.

You a create your own checklist but if you would like a copy of mine just email me at KJKLTD@rogers.com and let me know a bit about how you plan to use it (for my own curiosity). Specify if you would prefer the Excel or PDF versions. Mining due diligence exercises can be interesting and great learning experiences, even for senior people that have seen it all. However they can also be mentally taxing due to the volumes of information that one must find, review, and comprehend, all in a short period of time.

Mining due diligence exercises can be interesting and great learning experiences, even for senior people that have seen it all. However they can also be mentally taxing due to the volumes of information that one must find, review, and comprehend, all in a short period of time.