After having worked in the mining industry for over 40 years, it is interesting to experience the herd mentality that exists. Its fascinating to see how easily the industry gets caught chasing the latest fads and loses focus on the long term picture.

After having worked in the mining industry for over 40 years, it is interesting to experience the herd mentality that exists. Its fascinating to see how easily the industry gets caught chasing the latest fads and loses focus on the long term picture.

All it takes is a short term spike in a certain commodity price, or a big discovery somewhere, and then off goes the herd in that direction. It doesn’t matter the rationale driving the event, companies just know they need to be in there. Investors also know they need to be in there. Its classic FOMO; the fear of missing out.

These fad events, or crazes, can be based on certain commodities, jurisdictions, or technologies. The mining industry is flexible. Here are a few examples that I have seen; you may have others in your own experience.

Commodity Fads

Often as soon as there is a price spike or positive market narrative, commodity specific projects can take on a life of their own. The following are few examples, and when you reflect back on them, how many actually were a success for more than but a few.

Often as soon as there is a price spike or positive market narrative, commodity specific projects can take on a life of their own. The following are few examples, and when you reflect back on them, how many actually were a success for more than but a few.

-

Potash: several years ago potash prices spiked and acquiring potash leases was the fad. It didn’t matter where they were located around the globe, be it Canada, Russia, Ethiopia, Thailand, Brazil, etc. BHP even jumped in with both feet. The potash craze has largely fizzled out as prices returned to normal. We may be seeing a resurgence these days but not to the same level as in the past.

-

Lithium / Graphite: as soon as green battery technology started to be promoted in the news in 2016, miners couldn’t run fast enough to pick up the lithium properties. The same held for battery metals such graphite, vanadium, cobalt, and also rare earth categories. That was 2016. After a lull for a few years, the process restarted itself in 2022, although it seems the graphite – lithium excitement is now calming down in 2026.

-

Uranium: years ago uranium prices spiked and uranium properties were hot everywhere. Prices have dropped but seem to be ramping up again in late 2018 and the commodity is still somewhat hot in 2026.

-

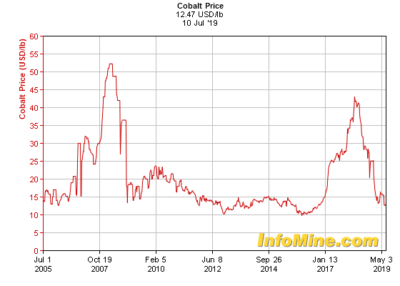

Cobalt Excitement Curve

Cobalt: see the price chart on the right to see how cobalt went into a craze and then out of it. Companies jumped into cobalt projects, then jumped out when the price dropped.

-

Nickel: years ago a spike in nickel prices caused a surge in nickel properties, whether it was sulphide nickel, laterite nickel, or other forms. Lately in 2026 nickel is given some credit as battery metal, but not as hot as it was.

-

Iron Ore: in conjunction with the Chinese construction boom decades ago, iron ore properties were hot around the globe, whether in high cost or low cost jurisdictions, it didn’t matter where the property was. Iron is still being pursued but its a lot quieter today in 2026.

-

Diamonds: in conjunction with the first diamond discoveries in Canada in the 1990’s, diamond properties became super hot, whether in the Canada or around the globe. If you couldn’t get a property in Canada’s NWT boom area, places like Alberta, Sask, Ontario or anywhere globally was fine too. The luster of diamonds seems to be gone now.

-

China in general: decades ago every base metal project was thought of as either a potential supplier to China or a potential acquisition for Chinese companies. As long as it could meet Chinese investor interest the project was good. That is not the norm now, but China is still seen as a potential target for many junior miner liquidity events.

-

In mid 2026, it seems that everyone is starting to look at tungsten and rare earths. We will see how this enfolds going forward.

Regional Exploration Fads

We have all seen the staking rushes that occur when a world class prospect is discovered. I’m sure we can all recall getting the large claim maps (as shown in Ring of Fire map) with their multicolored graphics showing the patchwork of acquisitions around a discovery. PDAC was great for distributing these. They were well done and always interesting to study.

We have all seen the staking rushes that occur when a world class prospect is discovered. I’m sure we can all recall getting the large claim maps (as shown in Ring of Fire map) with their multicolored graphics showing the patchwork of acquisitions around a discovery. PDAC was great for distributing these. They were well done and always interesting to study.

Picking up properties in hot areas (i.e. near-ology) became the fad and share prices would move upwards regardless of whether there was any favorable geology on the property, as long as it was in the region and made it onto the colorful map. Who recalls the following?

-

Voisey’s Bay: with a mad staking rush around Newfoundland, with nothing else really paying off in the long run.

-

Saskatchewan: the potash staking rush where almost every inch of the potash zone was staked with only a couple of companies eventually moving forward and only one or two going into production.

-

Indonesia: during Bre-X people could not acquire properties in Indonesia fast enough.

-

NWT: where the diamond property staking rush was crazy in the mid 1990’s.

-

BC Golden Triangle: where this seems to have been the hot area for the last few years.

Have I missed any areas that you see as hot?

Mining Technology Fads

Even mining or processing technologies could get caught up in somewhat of a wave and move the herd. Sometimes it was driven by suppliers or consultants. For the engineers out there, who can recall…

Even mining or processing technologies could get caught up in somewhat of a wave and move the herd. Sometimes it was driven by suppliers or consultants. For the engineers out there, who can recall…

-

Paste Tailings: with numerous conferences and consultants promoting thickened or paste tailings technology as the panacea. This lead to numerous studies related to thickening, pumping, and disposal at each mine. The paste fad has now ended as companies moved toward filtered tailings instead.

-

Block Caving: whereby in order to deliver high tonnages at low cost, bulk underground mining was being promoted. Everyone wanted their underground project to be a low cost caving style operation. This block cave concept is still in play today, but higher metal prices may make conventional open pits a bit more economic.

-

High Pressure Grinding Rolls (HPGR): where process consultants would highlight HPGR as the new replacement for conventional grinding mills. I’m not sure this technology has taken the industry by storm as they were hoping in the 1990’s.

-

IPCC: whereby inpit crushing and conveying systems were being promoted in many articles and global conferences as the solution to operating cost issues. I think implementation of IPCC technology isn’t as simple as envisioned and I’m not aware of many cases of its successful implementation.

-

Dot.com: in the early 2000’s many junior miners left exploration behind and transitioned to the dot.com boom, a fad that essentially went nowhere for most.

-

Pre-concentration: this seems to be a growing technology that may be gaining momentum. It isn’t new technology and it will definitely have its benefits. However a big stumbling block is how many deposits are actually suitable for its application. I have written more about this technology “Pre-Concentration – Savior or Not?“

-

Stochastic Modelling: many proponents are pushing towards the use of probabilities in mine planning. Its still the early stage here, so we will see if this gains traction. The herd is not running in this direction .. yet.

-

AI: The use of AI to summarize reports, compile, and analyze data is now being promoted by several online platforms. As the previous example, we will see if this gains traction since the herd are not chasing this yet.

Have I missed any that you see as growing trends?

Conclusion

Voisey’s Bay….based on no new discoveries, probably true, but the best place to find a new orebody is next to an orebody.

Saskatchewan Potash – Early mines had troubles producing. Several have been lost over the years. I lost a job when Cominco flooded back in 1970. Nevertheless there are quite a few mines in production right now.

Bre-Ex – it was a scam and it entrapped a lot of people.

Diamonds – up until Chuck Fipke came along they were a pipe (no pun intended) dream. Now that we know they are there…why not look for more?

Paste fill – definitely a winner for geotechnical reasons, although it took quite a bit of time to sort out the transportation issues. Kidd Creek would be closed without paste.

Block cave – Afton is an example of a mine where block cave has renewed its life. My first exposure to block cave was San Manuel, where they took 650 million tonnes of 0.6% copper from underground. That’s a huge economic and logistical success!

HPGR – maybe the jury is still out, but conventional technologies have not helped Mt Milligan, or Copper Mountain. Hard ores are especially difficult and SAG may not be the best process.

IPCC – agreed that it’s complicated, but it works and reduces truck fleets considerably.

Dot.com – right on! Most companies were destined to failure. Even today we have some highly overpriced ones like Amazon or Netflix, but at least they have a business plan and earnings.

Medical marijuana – it’s a “growth” industry!

Pre-concentration – with low grade orebodies it may be a way to keep mining in BC. We need someone with the courage to try it.

Here are a couple of my bugaboos.

Consensus metal prices – everyone uses them but no one believes them, particularly banks.

Government’s demands for consultant opinions – companies hire professionals who then hire consultants to do the dirty work. It’s a growing trend, yet companies usually possess the requisite skills in house.

For future articles…why not do something on the high cost of mining software? It’s driving the little guy right out of the business.