How long does it take to turn a mineral discovery into a producing mine. Also how long does permitting really take? These are questions that I see asked frequently in mining circles. The answer often thrown around is “18 years.” Is that really true or is it just a much-repeated industry myth?

How long does it take to turn a mineral discovery into a producing mine. Also how long does permitting really take? These are questions that I see asked frequently in mining circles. The answer often thrown around is “18 years.” Is that really true or is it just a much-repeated industry myth?

Answering these questions is one reason we created a new online App called Timeline Viewer, hosted on the Drilling Down website (https://sites.google.com/view/drillingdown).

What Is the Timeline Viewer

The Timeline Viewer is a online application where anyone can take a look at the milestone history of selected mining projects. Key milestones are laid out chronologically from initial exploration, through studies, permitting, and sometimes even up to production.

The Viewer puts it all in one place: a visual, browsable record of what happened and when. This information is derived from corporate press releases, and weblinks are provided.

This App was vibe coded using the Zite platform (https://www.zite.com/). Just explain to the AI what you want to create, and it then writes all the code for you. Very simple to use and fast.

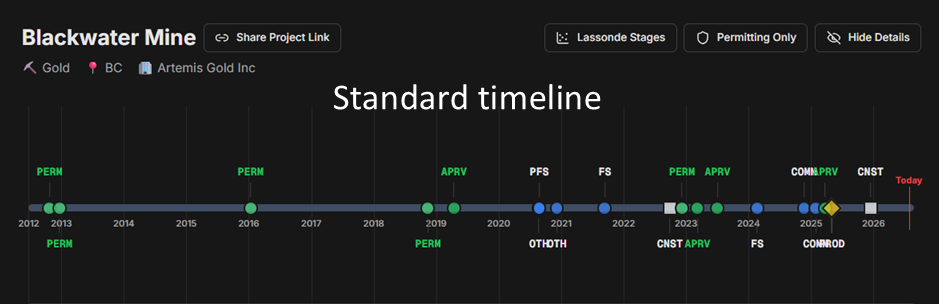

Let’s look at some Viewer output. The example below is the standard timeline view for the Brucejack Project in BC. One can see the sequence of activities that occurred over time as the mine moved into production. A details table (not shown) provides a brief description of each event. Hover over a point to see the details.

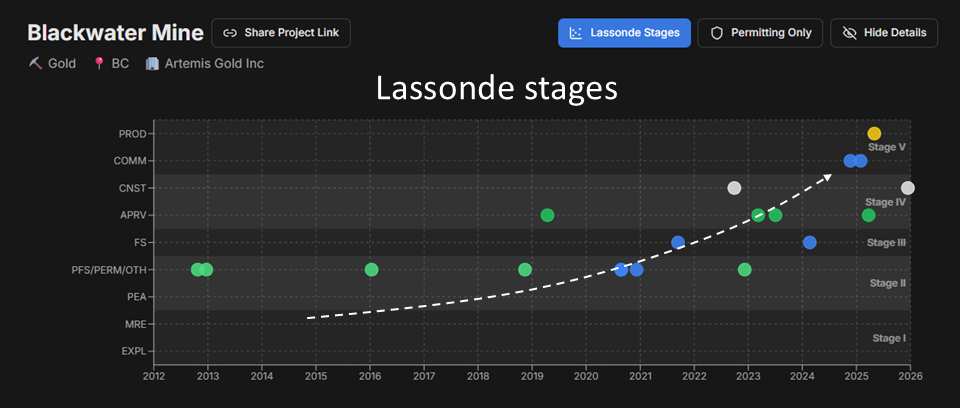

An alternate way to examine the same timeline is to view the development progress in stages. In the Viewer app, we loosely use the term the “Lassonde Stages”, related to the Lassonde Curve (for more info). The Timeline Viewer lets you toggle on a view of the stages over time. Is it advancing towards production or flat lining at the same Stage.

An alternate way to examine the same timeline is to view the development progress in stages. In the Viewer app, we loosely use the term the “Lassonde Stages”, related to the Lassonde Curve (for more info). The Timeline Viewer lets you toggle on a view of the stages over time. Is it advancing towards production or flat lining at the same Stage.

For example, the image below shows the same Brucejack project with the Stages on the right side and milestones on the left axis. One can see the rapid rise as the project accelerates from exploration & studies (Stage II) to construction, commissioning, and production (Stage V). For comparison, the next image after Brucejack is the chart for the KSM Project. Do you notice any difference in the profile of the Stages?

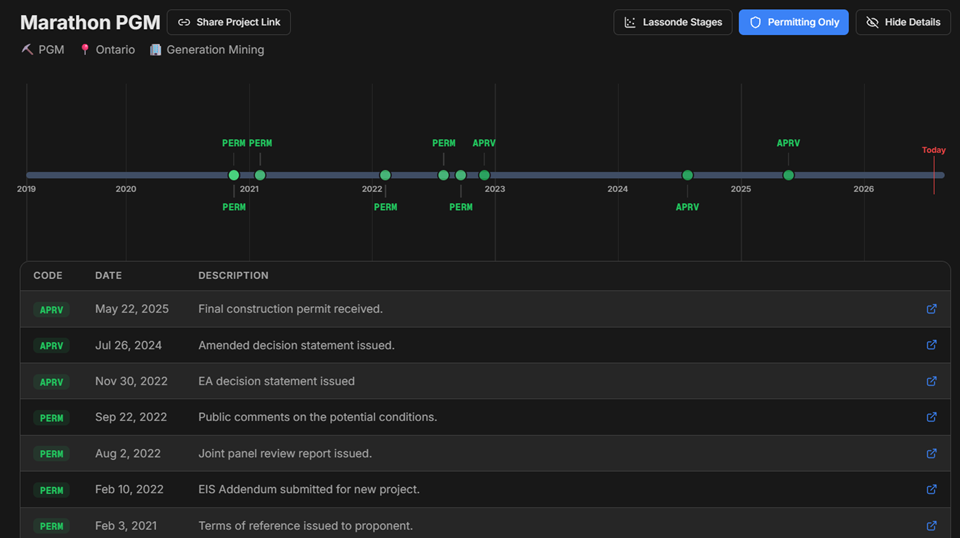

The Viewer also allows one to see only the “permitting” events to focus on those. When was permitting initiated and when were approvals received? As an example, the timeline below is for the Generation Mining Marathon project, permitting activities only. They started the process in 2021 and received their federal final permit in 2025. The ball is in their court now.

The Viewer also allows one to see only the “permitting” events to focus on those. When was permitting initiated and when were approvals received? As an example, the timeline below is for the Generation Mining Marathon project, permitting activities only. They started the process in 2021 and received their federal final permit in 2025. The ball is in their court now.

Getting Started: The List of Projects

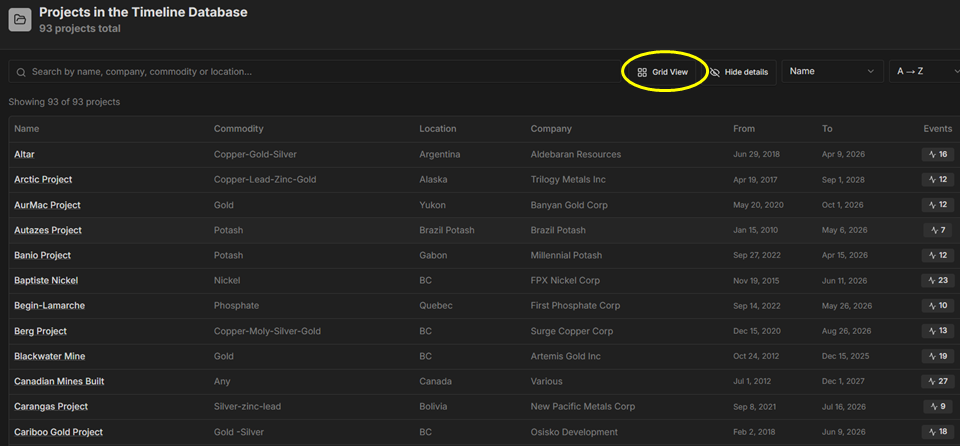

Before diving into an individual timelines, the obvious starting point is the List of Projects (https://jcrkyl7eju.zite.so/). This list gives you an overview of every project currently logged in the database (over 90 as of today).

You can browse the list in either Grid view or List view. Once you find a project of interest, clicking on it takes you to its timeline in the Viewer.

In the Viewer, (https://sites.google.com/view/drillingdown/timeline-viewer) you can trace the entire arc of a project’s development: when exploration drilling began, when a resource estimate was published, when studies (Preliminary Economic Assessment, Prefeasibility, Feasibility) were completed, when permits were approved, and when construction and commissioning eventually led to production. It’s a straightforward way to answer that “18 years” question for yourself, project by project.

Every milestone is categorized. The available categories cover the full lifecycle of a mining project: Exploration, Mineral Resource Estimate, Preliminary Economic Assessment, Prefeasibility Study, Feasibility Study, Permitting Activity, Permit Approval, Construction Start, Commissioning, Production, and a catch-all “Other” category for things like metallurgical testing, mergers, or partnerships that don’t fit neatly into the technical stages but are still significant to a project’s storyline.

All of the companies currently in the database (as of July 2026) are TSX listed. Many of their projects are in Canada, since government websites provide additional permitting timeline information as a backup. I noticed that some companies are much better at disclosing permitting steps than others. Its not often that I saw a company announce when public meetings were being held or when the public review period starts. I wonder why.

Why The Timeline Matters

For anyone following the mining sector, whether as an investor – analyst – geologist -engineer, the value of the Timeline Viewer is that it simplifies a series of press releases into a visual record.

You can look at different projects and start to notice patterns: which companies moved efficiently through permitting, which projects stalled for years at the exploration or pre-feasibility stage, and which ones sailed from discovery to production. Are there lifestyle companies out there in no hurry to get anywhere?

The Viewer is a tool for answering the “how long does it really take” question with actual information.

The Companion Piece: The Timeline Editor

The Timeline Viewer database is fed by a companion tool called the Timeline Editor, which is what allows the database to keep growing and stay current. The Editor is where the content gets compiled and maintained

If you’ve been following a specific project that isn’t in the database yet, you can add it yourself. Just send a message to KJKLTD@gmail.com to get access to the Editor. There is even a blank template available in Excel CSV format, so you can organize the project milestones on your own time and then upload them in the Editor.

One important thing to understand about this system is that it’s intended to be open source. Anyone who is given Editor access can modify a project’s timeline, which means there’s no absolute guarantee of accuracy on every entry. The information should be treated as crowdsourced rather than officially verified. Do not make investment decisions based on what you see here – this is for entertainment purposes only.

If you encounter a bug, issue or inaccuracy, please flag it by email (KJKLTD@gmail.com). We’re open to hearing comments, since nobody expects AI-written code to be 100% perfect.

Conclusion

The Timeline Viewer is a simple tool for seeing how mining projects actually move (or don’t move) from discovery through to production. Over time as more projects get logged, the database becomes a richer resource for answering that original question honestly: does it really take 18 years to build a mine or how long does it take to permit? With enough timelines in the database, you can decide for yourself.

The Timeline Viewer is a simple tool for seeing how mining projects actually move (or don’t move) from discovery through to production. Over time as more projects get logged, the database becomes a richer resource for answering that original question honestly: does it really take 18 years to build a mine or how long does it take to permit? With enough timelines in the database, you can decide for yourself.

Note: You can sign up for the KJK mailing list to get notified when new blogs are posted. Follow me on Twitter at @KJKLtd for updates and other mining posts. The entire blog post library can be found at https://kuchling.com/library/

For some free mining calculator apps, including project timelines and a simplified cashflow modeller, check out this website https://sites.google.com/view/drillingdown

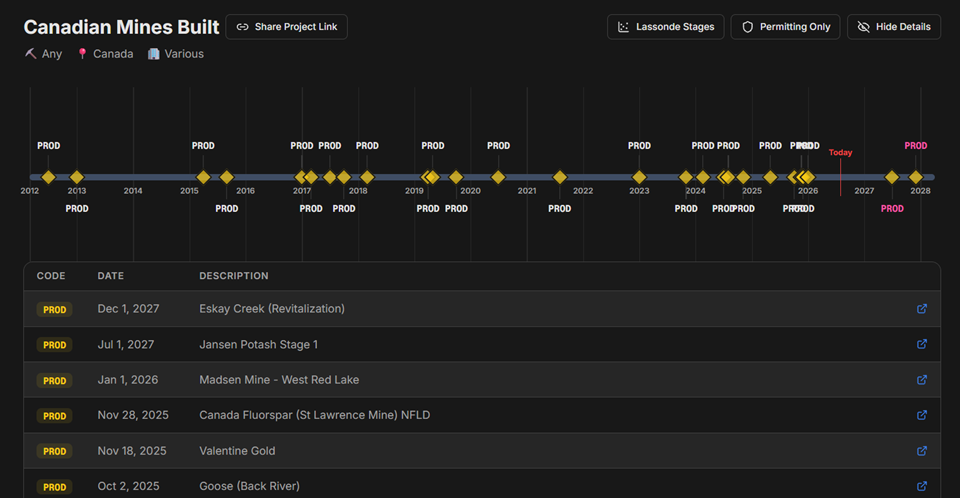

In closing, here is a summary timeline of all the mines coming into production in Canada over the last decade (from what I could find). The link to the timeline is https://neeovjtd7t.zite.so/project/3cd8bd8a-148f-4bc9-9bc3-fa56617f12d8

Every few weeks we see another feasibility study completed. Normally the numbers will look fantastic. The feasibility study shows that a project could work, but will it really work?

Every few weeks we see another feasibility study completed. Normally the numbers will look fantastic. The feasibility study shows that a project could work, but will it really work? Stalled projects will experience several of the roadblocks simultaneously. A single roadblock might be surmountable, but multiple roadblocks may not be.

Stalled projects will experience several of the roadblocks simultaneously. A single roadblock might be surmountable, but multiple roadblocks may not be. The list of potential production roadblocks is extensive. Moving from the study stage to production is very difficult and very few can do it successfully. A positive feasibility study is a necessary but far from sufficient condition for production.

The list of potential production roadblocks is extensive. Moving from the study stage to production is very difficult and very few can do it successfully. A positive feasibility study is a necessary but far from sufficient condition for production.

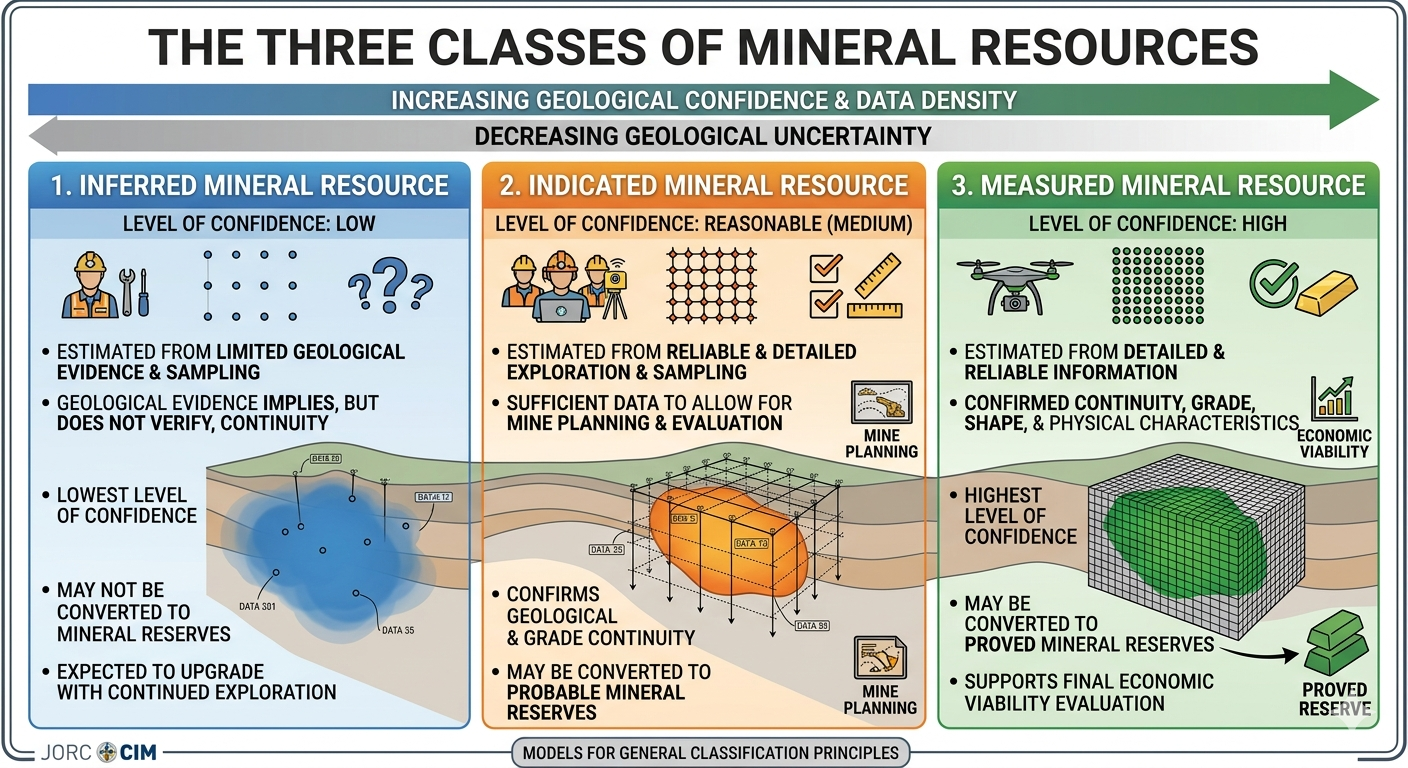

Inferred resources represent the lowest confidence category of mineral resources; typically estimated in zones with limited sampling and unconfirmed geological continuity. They carry the highest geological uncertainty of the three resource categories.

Inferred resources represent the lowest confidence category of mineral resources; typically estimated in zones with limited sampling and unconfirmed geological continuity. They carry the highest geological uncertainty of the three resource categories. Companies sometimes will commence the permitting process based on their PEA study. There are some risks to doing this, and the Inferred resource creates one of these risks.

Companies sometimes will commence the permitting process based on their PEA study. There are some risks to doing this, and the Inferred resource creates one of these risks. Let us examine some specific aspects of permitting that can be influenced by Inferred resources.

Let us examine some specific aspects of permitting that can be influenced by Inferred resources. Inferred resources present a unique paradox; they can and can’t be used in mining economic analysis. They can be used to examine project viability but can’t be used to make a production decision.

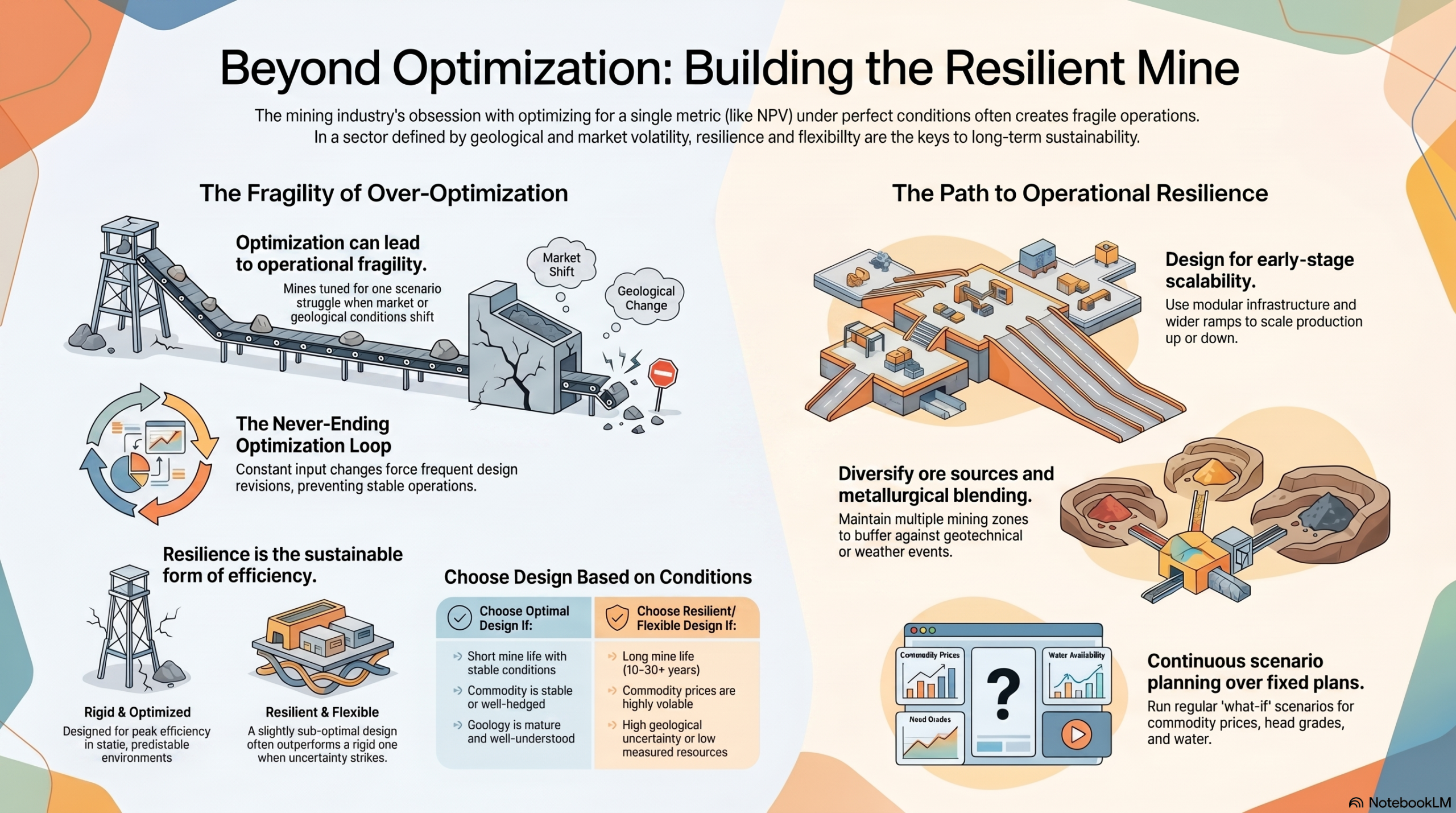

Inferred resources present a unique paradox; they can and can’t be used in mining economic analysis. They can be used to examine project viability but can’t be used to make a production decision. Is the concept of optimization the most important factor in a project’s design? If so, which aspect is the most important to optimize? A danger is optimizing for a single criteria, for example NPV, at the expense of everything else. Selecting the optimal design for one aspect will likely result in being sub-optimal in some of the others.

Is the concept of optimization the most important factor in a project’s design? If so, which aspect is the most important to optimize? A danger is optimizing for a single criteria, for example NPV, at the expense of everything else. Selecting the optimal design for one aspect will likely result in being sub-optimal in some of the others. Optimization of a mining project can yield meaningful cost and efficiency gains. However mines face inherent constraints, such as ore grade variability, geological surprises, equipment life cycles, and regulatory issues.

Optimization of a mining project can yield meaningful cost and efficiency gains. However mines face inherent constraints, such as ore grade variability, geological surprises, equipment life cycles, and regulatory issues. If one decides to pursue the path of operational flexibility, what are the things that help make it happen?

If one decides to pursue the path of operational flexibility, what are the things that help make it happen? Rather than focus on constant optimization in design, it may be wiser to focus on a flexible design. Adaptability, flexibility, and resilience may be more important than being fully optimized.

Rather than focus on constant optimization in design, it may be wiser to focus on a flexible design. Adaptability, flexibility, and resilience may be more important than being fully optimized.

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems.

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems. Exploration spending shares some of the same characteristics of more commonly R&D.

Exploration spending shares some of the same characteristics of more commonly R&D.

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

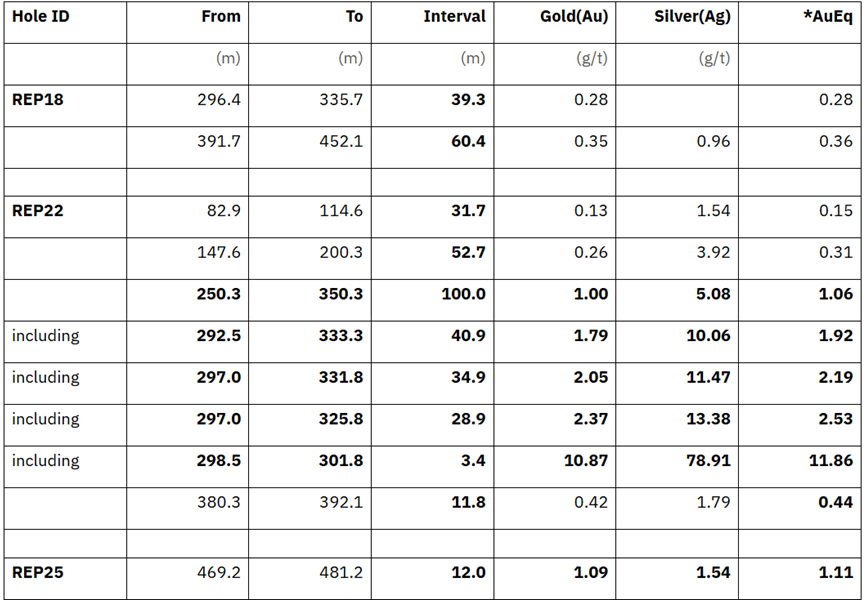

Recently I have been reviewing a few mining projects from an investor’s perspective. This led me to wonder whether junior mining companies should share more than just their drill hole highlights. What about the raw assays? A mining company announces highlighted drill intervals, but what exactly do those numbers represent?

Recently I have been reviewing a few mining projects from an investor’s perspective. This led me to wonder whether junior mining companies should share more than just their drill hole highlights. What about the raw assays? A mining company announces highlighted drill intervals, but what exactly do those numbers represent? There is a sense that many mining investors are becoming more sophisticated, and they want to fully understand the exploration process.

There is a sense that many mining investors are becoming more sophisticated, and they want to fully understand the exploration process.

1. Misinterpretation & “Amateur” Experts: One risk is that someone with a very basic understanding of mining software and limited understanding of the local geology, runs flawed interpretations and publicizes their incorrect conclusions. A company may find that correcting false narratives publicly can be harder than preventing them.

1. Misinterpretation & “Amateur” Experts: One risk is that someone with a very basic understanding of mining software and limited understanding of the local geology, runs flawed interpretations and publicizes their incorrect conclusions. A company may find that correcting false narratives publicly can be harder than preventing them. Once the assay data is public, it may be more difficult for a company to manage the story. A press release lets them frame results in the context of their business plan; a raw data file does not.

Once the assay data is public, it may be more difficult for a company to manage the story. A press release lets them frame results in the context of their business plan; a raw data file does not. For investors trying to assess a junior explorer, or geologists conducting a technical review, or a regulator trying to ensure fair and accurate disclosure, access to raw assay data can play a part in promoting good judgment and accurate disclosure from companies.

For investors trying to assess a junior explorer, or geologists conducting a technical review, or a regulator trying to ensure fair and accurate disclosure, access to raw assay data can play a part in promoting good judgment and accurate disclosure from companies.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening. USER PROMPT: What are the risks of toll milling plan.

USER PROMPT: What are the risks of toll milling plan. RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia.

RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia. The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

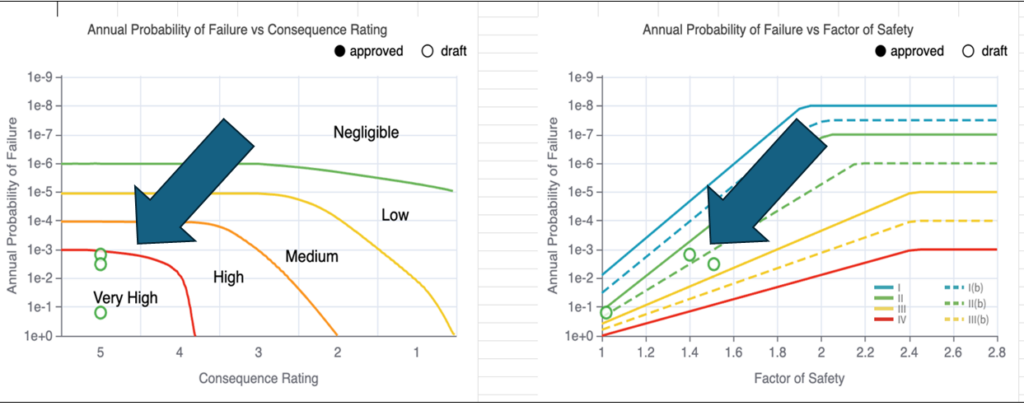

In my view, having a single industry platform for critical infrastructure risk management provides several benefits. These are:

In my view, having a single industry platform for critical infrastructure risk management provides several benefits. These are: Each mine site is unique with its own set of “Facilities”. For example, the individual Facilities could include Tailing Management Area #1, TMA #2, the Heap Leach Pad, Waste Dump #1, Waste Dump #2, etc.

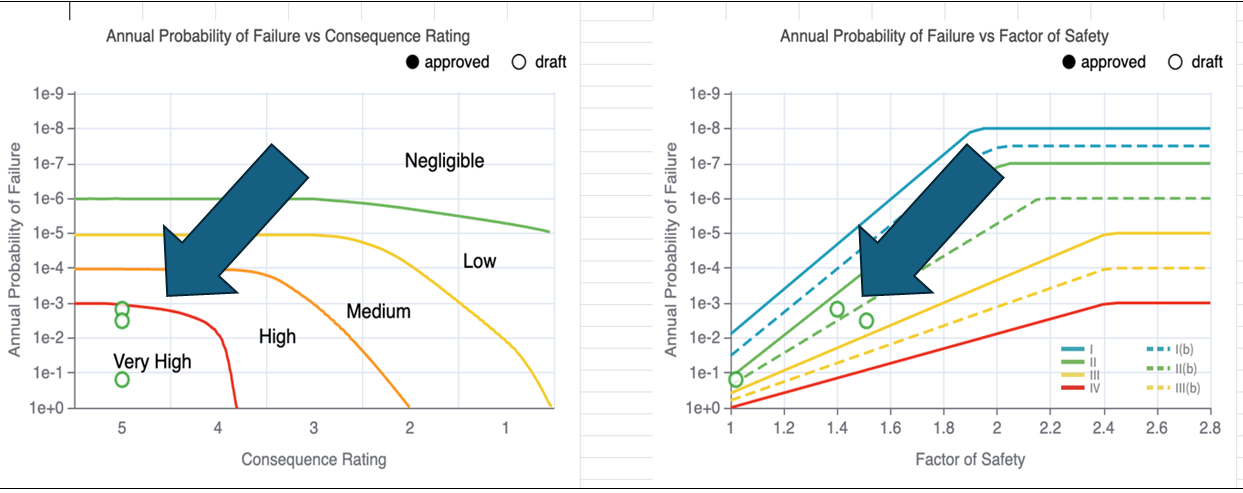

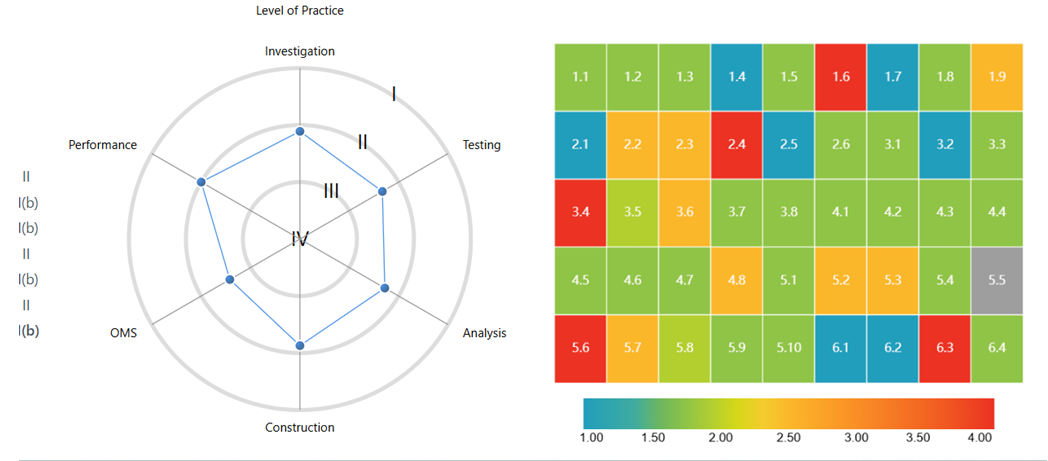

Each mine site is unique with its own set of “Facilities”. For example, the individual Facilities could include Tailing Management Area #1, TMA #2, the Heap Leach Pad, Waste Dump #1, Waste Dump #2, etc. The Level of Practice (LOP) is a measure of the integrity and quality of data used to design and manage a mine facility. The CI-RiskDB platform currently uses 45 criteria to evaluate the LOP associated with a facility. For example, these quality criteria include items such as: current understanding of soil profile; testing & verification between lab and field investigations; stability analysis detail; construction QA/QC undertaken, monitoring programs, etc.

The Level of Practice (LOP) is a measure of the integrity and quality of data used to design and manage a mine facility. The CI-RiskDB platform currently uses 45 criteria to evaluate the LOP associated with a facility. For example, these quality criteria include items such as: current understanding of soil profile; testing & verification between lab and field investigations; stability analysis detail; construction QA/QC undertaken, monitoring programs, etc.

Over confidence of personnel is something that can unfortunately play a role in risk management. However, the more eyes involved with reviews and signoffs, as well as occasional third party audits, the less likely that this occurs (hopefully).

Over confidence of personnel is something that can unfortunately play a role in risk management. However, the more eyes involved with reviews and signoffs, as well as occasional third party audits, the less likely that this occurs (hopefully). In closing, as of this month December 2025, I understand the Critical Infrastructure Risk Decision Basis platform is currently being piloted and implemented at a number of mine sites in Canada, including Agnico Eagle at a corporate level. Additional pilots may be forthcoming in 2026.

In closing, as of this month December 2025, I understand the Critical Infrastructure Risk Decision Basis platform is currently being piloted and implemented at a number of mine sites in Canada, including Agnico Eagle at a corporate level. Additional pilots may be forthcoming in 2026.

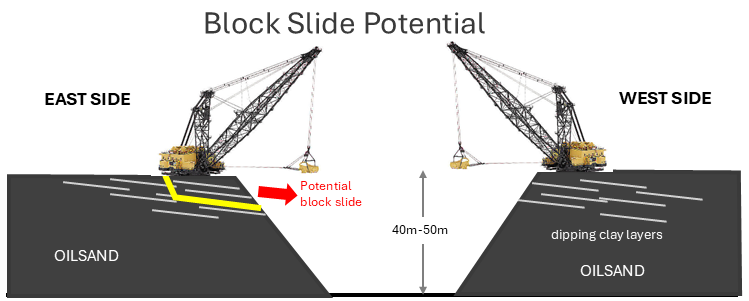

Syncrude had four large walking draglines, each with a 80 cubic metre bucket and 110 metre operating radius. These were very big machines; you could sit one in the end zone of a football field and the bucket would be digging (or dumping) in the other end zone. Two draglines were on the East side of the mine and two were on the West, mining the oilsand in 25 m wide strips.

Syncrude had four large walking draglines, each with a 80 cubic metre bucket and 110 metre operating radius. These were very big machines; you could sit one in the end zone of a football field and the bucket would be digging (or dumping) in the other end zone. Two draglines were on the East side of the mine and two were on the West, mining the oilsand in 25 m wide strips. There were numerous instances of East mine block slides, where large portions of the upper slope would fail as large blocks, 50 metres long and up to 30 metres back from the crest. The fear was that if a dragline happened to be sitting on one of these failing blocks, the entire machine would slide along into the pit. Many block slides did occur over the years, but only a few came close to jeopardizing a machine. The geotechnical monitoring programs in place were successful (described later).

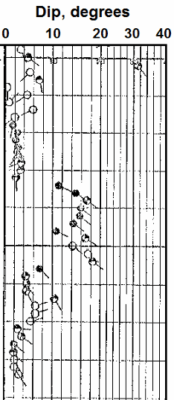

There were numerous instances of East mine block slides, where large portions of the upper slope would fail as large blocks, 50 metres long and up to 30 metres back from the crest. The fear was that if a dragline happened to be sitting on one of these failing blocks, the entire machine would slide along into the pit. Many block slides did occur over the years, but only a few came close to jeopardizing a machine. The geotechnical monitoring programs in place were successful (described later). The insitu clay structures were identified using oil and gas borehole logging technology, with tadpole dipmeter plots (see image) used to analyse the bedding (the tail on the tadpole shows the dip direction). The vertical axis is depth from surface or elevation. The geotech engineers would use this information, combined with structural mapping of previously mined faces, to forecast potentially unstable areas.

The insitu clay structures were identified using oil and gas borehole logging technology, with tadpole dipmeter plots (see image) used to analyse the bedding (the tail on the tadpole shows the dip direction). The vertical axis is depth from surface or elevation. The geotech engineers would use this information, combined with structural mapping of previously mined faces, to forecast potentially unstable areas. The main geotechnical issue on the West side were basal slope failures, termed this due to sliding along weak clays and muds at the base of the highwall. This photo shows a typical basal failure. Basal failures also occured on the East side.

The main geotechnical issue on the West side were basal slope failures, termed this due to sliding along weak clays and muds at the base of the highwall. This photo shows a typical basal failure. Basal failures also occured on the East side. Once our engineer-in-training rotation program was complete, we were to be assigned to a more permanent position. For me, that was going to be as an East side geotechnical engineer – ugh!. It’s at that time I decided to look for greener pastures. Three years was long enough from 1980 to 1983; given the amount of learning and responsibility I had undertaken. Other colleagues left the same time, while many other friends stayed in Ft McMurray for their entire careers.

Once our engineer-in-training rotation program was complete, we were to be assigned to a more permanent position. For me, that was going to be as an East side geotechnical engineer – ugh!. It’s at that time I decided to look for greener pastures. Three years was long enough from 1980 to 1983; given the amount of learning and responsibility I had undertaken. Other colleagues left the same time, while many other friends stayed in Ft McMurray for their entire careers.

In Part 1 of this two part blog post I would like to share some stories from the early days of my career working in Fort McMurray.

In Part 1 of this two part blog post I would like to share some stories from the early days of my career working in Fort McMurray. At the time Syncrude had an excellent engineer-in-training program for new graduates. Every six months they would rotate engineers into different technical areas.

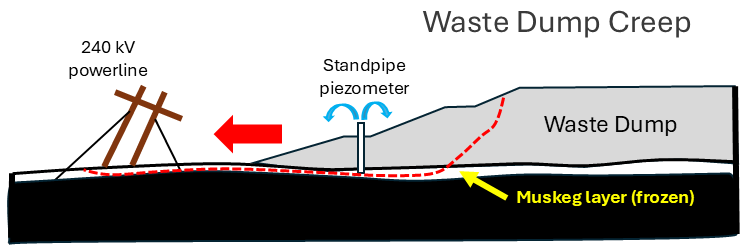

At the time Syncrude had an excellent engineer-in-training program for new graduates. Every six months they would rotate engineers into different technical areas. Next we sampled that depth carefully, revealing that frozen muskeg layers were present. When we installed standpipe piezometers in these holes, we saw water flowing out of the top of the pipes. This means the foundation pore pressure is high, way too high.

Next we sampled that depth carefully, revealing that frozen muskeg layers were present. When we installed standpipe piezometers in these holes, we saw water flowing out of the top of the pipes. This means the foundation pore pressure is high, way too high. For example, one project I had was to monitor the performance of different brands and styles of conveyor idlers. We would track about 2,000 individual idlers; when they were installed on the conveyors; when they were removed, why they were removed (bearing failure, cover failure, something else).

For example, one project I had was to monitor the performance of different brands and styles of conveyor idlers. We would track about 2,000 individual idlers; when they were installed on the conveyors; when they were removed, why they were removed (bearing failure, cover failure, something else).