This is Part 2 of the blog post discussing junior mining scams and the sanctioning of those responsible. Part 1 can be found at this link “Junior Mining Shams and Scams – Part 1” and can be read first to get some background.

This is Part 2 of the blog post discussing junior mining scams and the sanctioning of those responsible. Part 1 can be found at this link “Junior Mining Shams and Scams – Part 1” and can be read first to get some background.

Part 2 provides examples involving professional Qualified Persons (QPs). We may have the feeling that QP’s are never held accountable for their work, but that is not always the case. There are numerous instances of QP’s being hauled off in front of their professional organizations for unprofessionalism. This blog will highlight some of those cases.

The lesson is that QP’s signing off on technical information for clients should be proficient in the nature of their work and need to know the reporting rules very well. Some of these incidents involve error and poor judgment, not outright fraud.

These examples involve in-house QP’s that work for a company while others involve independent QP’s that have been contracted by the company.

In most of these cases, any sanctions, if applied, were mainly doled out by the professional engineering or geological associations. The legal courts are often not involved.

Examples (Part 2)

Inaccurate QP Resource Estimate: This example relates to the Barkerville Gold Mines resource estimate complete in 2012. The mineral resource estimate had numerous errors and issues related to assays, capping, cutoff grades, etc. The allegation was the QP had demonstrated incompetence, unprofessional conduct, and negligence. The sanctions on the QP included a $15,000 fine, $20,000 legal costs, re-training, and license suspension.

Link 1:

Link 2:

False QP Statements: Here is an example from 2011. The QP / company Director was charged with multiple allegations, including stating the mine was in commercial production (when it wasn’t), leaving the impression there were mineral resource (which there weren’t any), and generally approving information that was not accurate. Ultimately the allegation was demonstrating incompetence, unprofessional conduct, and negligence. The resulting sanctions included 2 year license suspension, re-training, payment of $80,000 to the professional association.

Link 1:

False QP Statements: This is case were a resource QP failed to comply with the NI43-101, Form 43-101F1, CIM Standards, and CIM Guidelines. The Panel concluded that the Member was guilty of non-compliance with the standards and hence guilty of professional misconduct. Its not clear what specifically was not complied with, but this illustrates that QP’s will be held accountable for their work. The two reports in question were either amended or withdrawn to address the concerns of the regulator in British Columbia, although there had been no intentional non-compliance and no economic impact. The penalty was 2 months suspension (deferred), and the QP had to work under a mentor for 9 months and pay a maximum $10,000 for the mentor’s fees.

Link 1:

False QP Statements: Here is another example of sanctioning a QP in 2018. The person was charged with unprofessional conduct and incompetence. He stated that he was responsible for the preparation of the technical report, had no prior involvement in the project, and was independent of the issuer. This was false. Sanctions included three month license suspension, taking some re-training, require peer review of the report. In 2022, further sanctions consisted of a $75,000 penalty, further sanctioned along with an executive in the company for insider trading issues (see Link 3 below).

Link 1:

Link 2:

Link 3:

False QP Statements: This is an example for 2017 when an independent QP took responsibility for the resource estimation work in section 14 of the report, yet they did not have the experience to take responsibility. They also misrepresented that the Report complied with 2014 CIM standards, yet it didn’t, resulting in an overestimation of the mineral resource in both confidence and magnitude. Other claims include relying on non-QP experts but not stating that, failing to adequately discuss the nature of sample quality control procedures as required. The sanctions included license suspension of 3 months, must work with a technical supervisor, re-training, and $7,500 in legal fees.

Link 1:

False QP Statements: This is another example from 2019, when the QP / Director permitted the disclosure of information to the public in multiple news releases where they should have known that that information was misleading. An example is the disclosure of inferred reserves when there were no reserves and “inferred” is not even a classification of reserves. The sanctions were a license suspension of 4 months, $5,000 legal costs, re-training, and requirement not to act as a QP again.

Link 1:

QP Resource Estimate Error: This occurred in 2012 when a QP and consulting firm delivered a incorrect resource estimate and reportedly withheld negative opinions on the project from the client. The company spent $3 million on a feasibility study during which the resource estimate error was discovered. The “corrected” resource made the project uneconomic, meaning the feasibility study should not have been done. The mining company sought compensation from the consulting firm, ultimately receiving $1.25 million. The Link 3 references is interesting in that it states “As this case demonstrates, it is critically important for professional service firms to be forthcoming about any reservations they may have regarding the work they are being employed to undertake.” Whatever that really means?

Link 1:

Link 2:

Link 3:

Disclaimers

Many QP’s realize the legal responsibility and liability they have. Hence in 43-101 reports QP’s sometimes attempt to mitigate this by putting in broad disclaimers to limited that liability. If the securities commission notices such disclaimers, they will require that they be removed.

For example, sometimes the QP of a chapter may have other geologists or engineers (i.e. experts) assisting them. They may then put in disclaimers saying “They disclaim responsibility for such expert content” for the work done by the others. A QP essentially has to sign off on the work of others in the sections they are responsible for. A recent example is a Generation Mining technical report prepared by G-Mining, that had to be amended from (March 31_2023 to May 31_2024) removing several QP liability limiting disclaimers.

43-101 regulations state that “An issuer must not file a technical report that contains a disclaimer by any qualified person responsible for preparing or supervising the preparation of all or part of the report that

43-101 regulations state that “An issuer must not file a technical report that contains a disclaimer by any qualified person responsible for preparing or supervising the preparation of all or part of the report that

(a) disclaims responsibility for, or limits reliance by another party on, any information in the part of the report the qualified person prepared or supervised the preparation of;

or (b) limits the use or publication of the report in a manner that interferes with the issuer’s obligation to reproduce the report by filing it on SEDAR.“

” These disclaimers are also potentially misleading disclosure because, in certain circumstances, securities legislation provides investors with a statutory right of action against a qualified person for a misrepresentation in disclosure that is based upon the qualified person’s technical report.

That right of action exists despite any disclaimer to the contrary that appears in the technical report. The securities regulatory authorities will generally require the issuer to have its qualified person remove any blanket disclaimers in a technical report that the issuer uses to support its public offering document.“

Ramp and Dumps

In April 2026, the Canadian Securities Administrators warned investors about a surge in “ramp-and-dump” schemes. These involve online groups coordinating purchases of thinly traded junior mining stocks, promoting them aggressively on social media, then selling into the price spike. Its not too hard to find these people on Twitter X; they never have a bad thing to say about a company.

Altough I have not come across these, Canadian regulators have warned of fraudulent websites and investment groups pretending to offer investments in mining companies or claiming insider access to exploration projects. These scams can use fake drilling results, forged technical reports, or fabricated takeover rumours to lure investors.

The Canadian Investment Regulatory Organization has also continued warning investors about fake mining investment firms impersonating legitimate brokers and requesting additional deposits before releasing supposed profits (see link here).

The BSCS has recently clarified that if one is paid to promote/recommend stocks on social media or message boards it could be considered a ‘promotional activity’ that still falls under securities law. Whenever they share information about a company that could encourage the buying or selling a company’s shares, they must follow securities law. BSC has issued a checklist to determining if one must abide by the rules (see link here).

Conclusion

This ends Part 2 of this blog post. It hopefully highlights the importance of QP’s being knowledgably on the disclosure rules and the technical aspects of what they are hired to do.

This ends Part 2 of this blog post. It hopefully highlights the importance of QP’s being knowledgably on the disclosure rules and the technical aspects of what they are hired to do.

In April 2024 Red Pine Exploration issued several press releases highlighting that some assays in their geological database were found to have been manipulated. Numerous assays input into their database did not match the original lab certificates. Is this another mining scam?

In April 2024 Red Pine Exploration issued several press releases highlighting that some assays in their geological database were found to have been manipulated. Numerous assays input into their database did not match the original lab certificates. Is this another mining scam? The focus of this blog is on the types of activities that raised the red flags in the past. I am less interested in naming the people responsible, although the associated web links do provide more detail on the events.

The focus of this blog is on the types of activities that raised the red flags in the past. I am less interested in naming the people responsible, although the associated web links do provide more detail on the events. This ends Part 1 of this blog post. Part 2 will continue with a few more examples, specifically involving Qualified Persons, and can be found at this link

This ends Part 1 of this blog post. Part 2 will continue with a few more examples, specifically involving Qualified Persons, and can be found at this link

Part 2 of this blog post will focus on the remaining engineering work to finish Chapter 16 of the Technical Report. We only wrote about half of it in Part 1. The mining engineer can generally handle the rest of these tasks in this Chwithout requiring a lot of external input. You can read Part 1 at this link “

Part 2 of this blog post will focus on the remaining engineering work to finish Chapter 16 of the Technical Report. We only wrote about half of it in Part 1. The mining engineer can generally handle the rest of these tasks in this Chwithout requiring a lot of external input. You can read Part 1 at this link “ Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times. Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its value, smoothing the ore delivery to the plant.

Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its value, smoothing the ore delivery to the plant. Once the production schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

Once the production schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate. These two blog posts give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

These two blog posts give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

On YouTube, there are also a lot of educational videos related to mining. Some of the same audio podcast episodes are also available on the YouTube platform. Given an option, I prefer the audio-only podcast format over YouTube.

On YouTube, there are also a lot of educational videos related to mining. Some of the same audio podcast episodes are also available on the YouTube platform. Given an option, I prefer the audio-only podcast format over YouTube. Pick and choose. One can’t listen to all the podcast episodes available or else you wouldn’t have time to do anything else in life. You would also become bored since much of it can be repetitive.

Pick and choose. One can’t listen to all the podcast episodes available or else you wouldn’t have time to do anything else in life. You would also become bored since much of it can be repetitive. Mining Stock Education (680 episodes)

Mining Stock Education (680 episodes)  Fresh Thinking by Optiro-Snowden (53 episodes) This podcast is hosted by Snowdon – Optiro consultants. They typically focus on resource modelling and grade reconciliation aspects. The episodes are fairly short (15 mins), which is nice. Although I am not a resource modeller, I can always learn more about the black art of resource modelling.

Fresh Thinking by Optiro-Snowden (53 episodes) This podcast is hosted by Snowdon – Optiro consultants. They typically focus on resource modelling and grade reconciliation aspects. The episodes are fairly short (15 mins), which is nice. Although I am not a resource modeller, I can always learn more about the black art of resource modelling. There is no shortage of material in the podcast world about the mining industry. It all depends on what interests you the most. There is even more mining information available on YouTube, if you have the time to sit and watch videos. Nevertheless the audio-only platform is great, although you don’t get to see the charts being discussed. That’s fine with me, particularly if they take a few seconds to describe the chart.

There is no shortage of material in the podcast world about the mining industry. It all depends on what interests you the most. There is even more mining information available on YouTube, if you have the time to sit and watch videos. Nevertheless the audio-only platform is great, although you don’t get to see the charts being discussed. That’s fine with me, particularly if they take a few seconds to describe the chart.

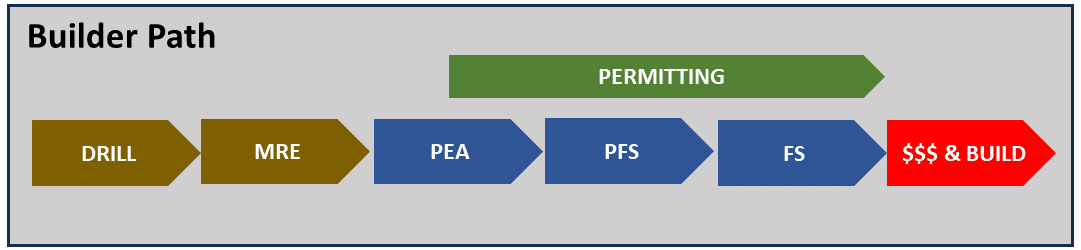

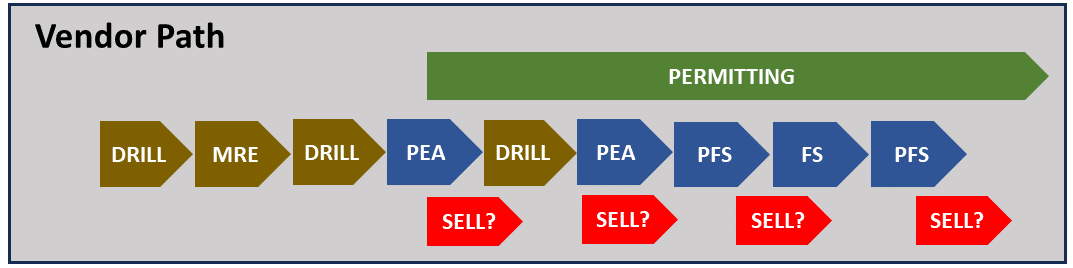

If an engineer understands that a Mine Builder’s project will move from PEA to PFS to FS in rapid succession, then there is more incentive to ensure each study is somewhat integrated.

If an engineer understands that a Mine Builder’s project will move from PEA to PFS to FS in rapid succession, then there is more incentive to ensure each study is somewhat integrated. The objective of the Mine Vendor is to make the project attractive to potential buyers. There is less urgency in fast tracking detailed engineering and permitting.

The objective of the Mine Vendor is to make the project attractive to potential buyers. There is less urgency in fast tracking detailed engineering and permitting. As an engineer, it is helpful to understand the objectives of the project owner and then tailor the technical studies to meet those objectives. This does not mean low balling costs to make the study a promotional tool. It means focusing on what is important. It means recognizing the path, and what doesn’t need to be engineered in detail at this time. This may save the client time, money, and improve credibility in the long run.

As an engineer, it is helpful to understand the objectives of the project owner and then tailor the technical studies to meet those objectives. This does not mean low balling costs to make the study a promotional tool. It means focusing on what is important. It means recognizing the path, and what doesn’t need to be engineered in detail at this time. This may save the client time, money, and improve credibility in the long run. This post is just a brief discussion of mining project timelines. For those interested, there a few additional project timelines for curiosity purposes. Each path is unique because no two mining projects are the same. You can find these examples at this link “

This post is just a brief discussion of mining project timelines. For those interested, there a few additional project timelines for curiosity purposes. Each path is unique because no two mining projects are the same. You can find these examples at this link “

This article is about the benefit of preparing (cutting) more geological cross-sections and the value they bring.

This article is about the benefit of preparing (cutting) more geological cross-sections and the value they bring. Long sections are aligned along the long axis of the deposit. They can be vertically oriented, although sometimes they may be tilted to follow the dip angle of an ore zone.

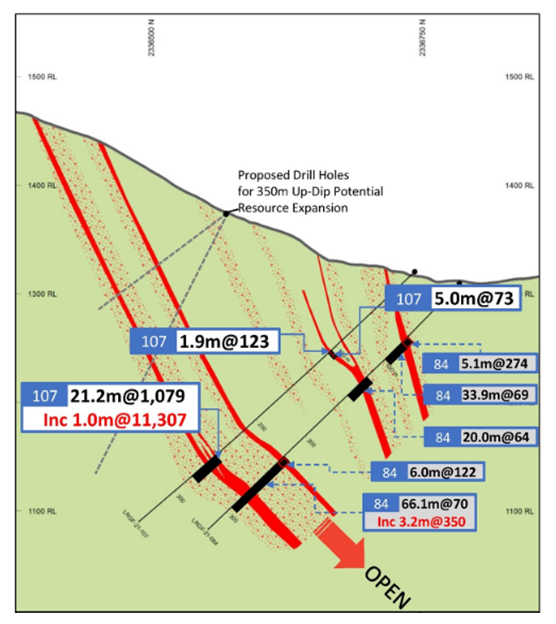

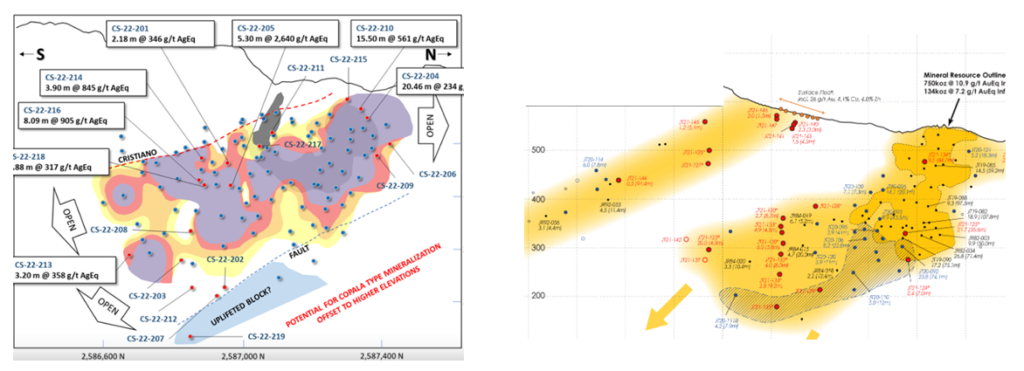

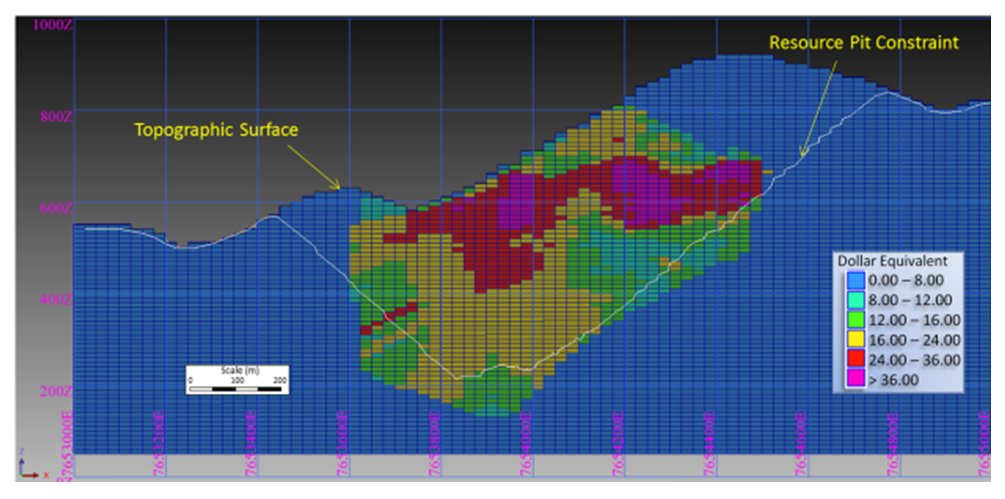

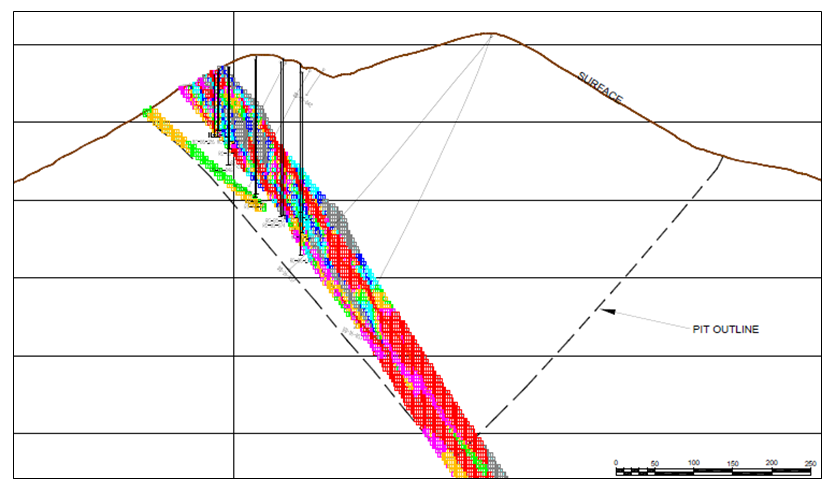

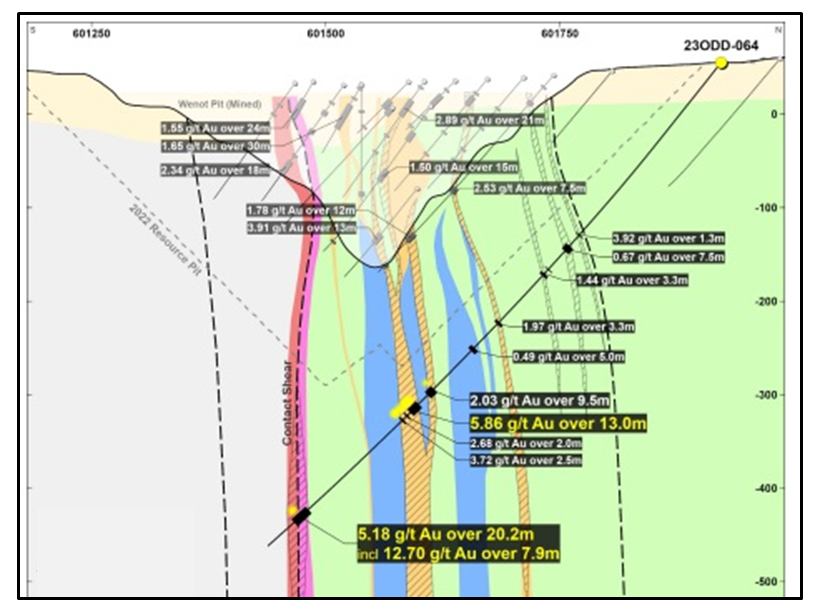

Long sections are aligned along the long axis of the deposit. They can be vertically oriented, although sometimes they may be tilted to follow the dip angle of an ore zone. Cross-sections are generally the most popular geological sections seen in presentations. These are vertical slices aligned perpendicular to the strike of the orebody. They can show the ore zone interpretation, drill holes traces, assays, rock types, and/or color-coded resource block grades.

Cross-sections are generally the most popular geological sections seen in presentations. These are vertical slices aligned perpendicular to the strike of the orebody. They can show the ore zone interpretation, drill holes traces, assays, rock types, and/or color-coded resource block grades. When looking at cross-sections, it is always important to look at multiple cross-sections across the orebody. Too often in reports one may be presented with the widest and juiciest ore zone, as if that was typical for the entire orebody. It likely is not typical.

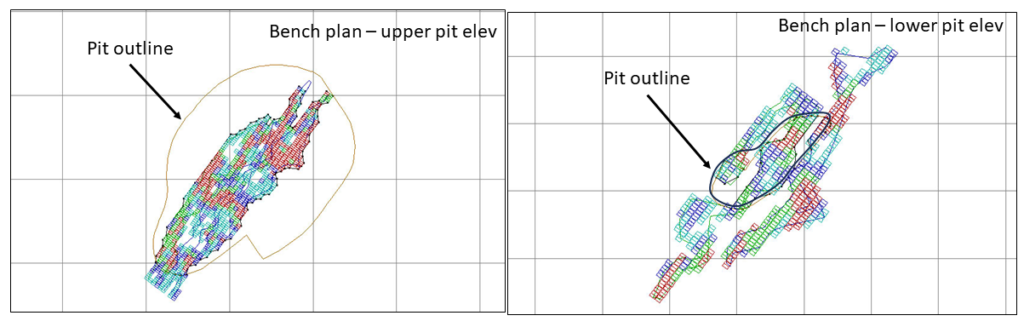

When looking at cross-sections, it is always important to look at multiple cross-sections across the orebody. Too often in reports one may be presented with the widest and juiciest ore zone, as if that was typical for the entire orebody. It likely is not typical. Bench plans (or level plans) are horizontal slices across the ore body at various elevations. In these sections one is looking down on the orebody from above.

Bench plans (or level plans) are horizontal slices across the ore body at various elevations. In these sections one is looking down on the orebody from above. 3D PDF files can be created by some of the geological software packages. They can export specific data of interest; for example topography, ore zone wireframes, underground workings, and block model information. These 3D files allows anyone to rotate an image, zoom in as needed and turn layers off and on.

3D PDF files can be created by some of the geological software packages. They can export specific data of interest; for example topography, ore zone wireframes, underground workings, and block model information. These 3D files allows anyone to rotate an image, zoom in as needed and turn layers off and on. The different types of geological sections all provide useful information. Don’t focus only on cross-sections, and don’t focus only on one typical section. Create more sections at different orientations to help everyone understand better.

The different types of geological sections all provide useful information. Don’t focus only on cross-sections, and don’t focus only on one typical section. Create more sections at different orientations to help everyone understand better.

When disclosing polymetallic drill results, many companies will convert the multiple metal grades into a single equivalent grade. I am not a big proponent of that approach.

When disclosing polymetallic drill results, many companies will convert the multiple metal grades into a single equivalent grade. I am not a big proponent of that approach. The three aspects that interest me the most when looking at early-stage drill results are:

The three aspects that interest me the most when looking at early-stage drill results are:

The “NSR factor” would now be 85% x 85% or 75%. Therefore, if the breakeven cost is $14/t, then one should target to mine rock with an insitu value greater than $20/tonne (i.e. $14 / 0.75). This would be the approximate ore vs waste cutoff. It is still only ballpark estimate at this early stage, but good enough for this type of review.

The “NSR factor” would now be 85% x 85% or 75%. Therefore, if the breakeven cost is $14/t, then one should target to mine rock with an insitu value greater than $20/tonne (i.e. $14 / 0.75). This would be the approximate ore vs waste cutoff. It is still only ballpark estimate at this early stage, but good enough for this type of review.

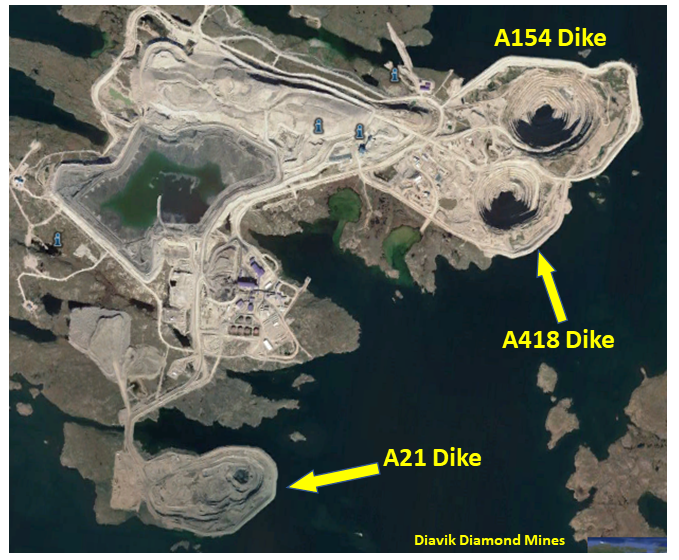

The primary question to be answered is whether one can mine safely and economically without creating significant impacts on the environment.

The primary question to be answered is whether one can mine safely and economically without creating significant impacts on the environment. Lake Turbidity: Dike construction will need to be done through the water column. Works such as dredging or dumping rock fill will create sediment plumes that can extend far beyond the dike. Is the area particularly sensitive to such turbidity disturbances, is there water current flow to carry away sediments?

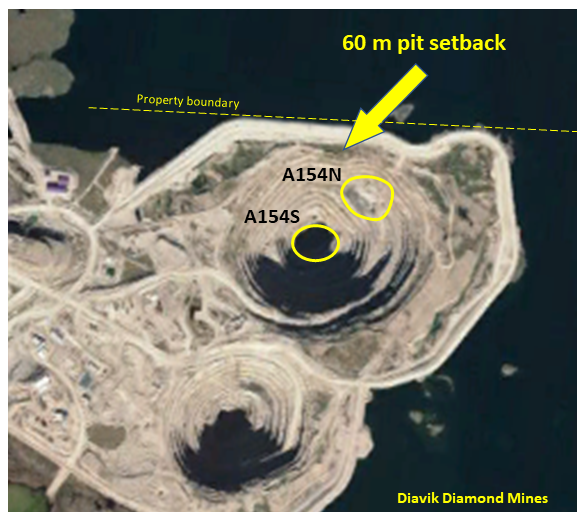

Lake Turbidity: Dike construction will need to be done through the water column. Works such as dredging or dumping rock fill will create sediment plumes that can extend far beyond the dike. Is the area particularly sensitive to such turbidity disturbances, is there water current flow to carry away sediments? Pit wall setback: Given the size and depth of the open pit, how far must the dike be from the pit crest? Its nice to have 200 metre setback distance, but that may push the dike out into deeper water.

Pit wall setback: Given the size and depth of the open pit, how far must the dike be from the pit crest? Its nice to have 200 metre setback distance, but that may push the dike out into deeper water. Once the approximate location of the dike has been identified, the next step is to examine the design of the dike itself. Most of the issues to be considered relate to the geotechnical site conditions.

Once the approximate location of the dike has been identified, the next step is to examine the design of the dike itself. Most of the issues to be considered relate to the geotechnical site conditions. Each mine site is different, and that is what makes mining into water bodies a unique challenge. However many mine operators have done this successfully using various approaches to tackle the challenge.

Each mine site is different, and that is what makes mining into water bodies a unique challenge. However many mine operators have done this successfully using various approaches to tackle the challenge.

NPV One is targeting to replace the typical Excel based cashflow model with an online cloud model. It reminds me of personal income tax software, where one simply inputs the income and expense information, and then the software takes over doing all the calculations and outputting the result.

NPV One is targeting to replace the typical Excel based cashflow model with an online cloud model. It reminds me of personal income tax software, where one simply inputs the income and expense information, and then the software takes over doing all the calculations and outputting the result. Pros

Pros Like anything, nothing is perfect and NPV may have a few issues for me.

Like anything, nothing is perfect and NPV may have a few issues for me. The NPV One software is an option for those wishing to standardize or simplify their financial modelling.

The NPV One software is an option for those wishing to standardize or simplify their financial modelling.