There have been recent heap leach pad failures in the Yukon and Turkey and tailings dam failures in Chile and the Philippines. As a result I have been seeing more posts on LinkedIn about the application of satellite based InSAR deformation monitoring. Prior to that I had never heard of InSAR, so thought a little bit of background study might be worthwhile.

The following are my observations on what InSAR is and where it may be going. I am by no means an expert in this technology. I am merely viewing it from the perspective of a mine design engineer.

What is InSAR

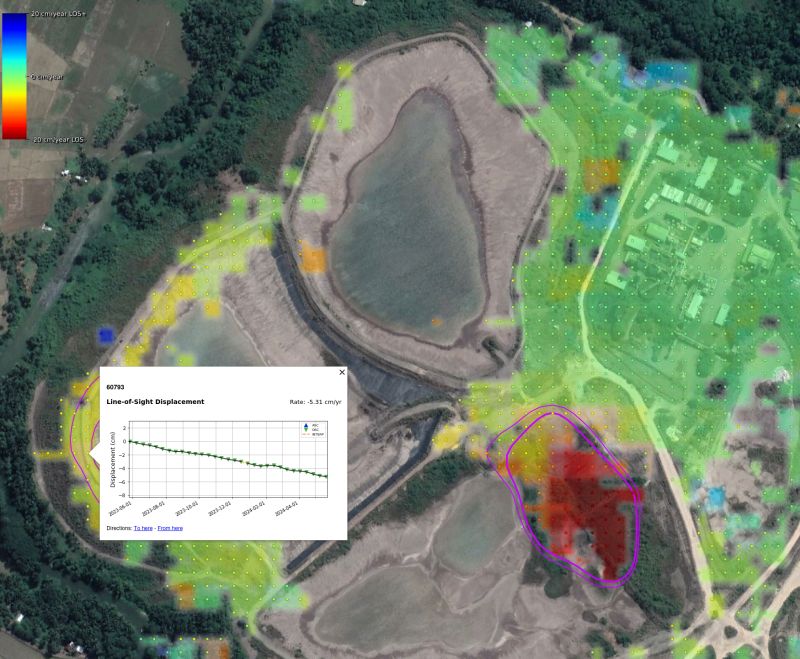

InSAR is satellite-based “Interferometric Synthetic Aperture Radar”. It can measure the distance from a satellite to a ground feature. With repeated imaging it is used to detect changes in distance and measure displacements to within 5-10 millimetre accuracy. Hence it can be used as a potentially cost-effective slope monitoring tool, albeit it cannot be the only tool, as discussed later.

The relevant satellite images have been available for years. Currently the availability of analytical software to interpret the satellite data is improving. It can detect millimeter-scale displacements, however only in the line-of-sight (LOS) direction of the satellite. Using two or more satellites in different orbits, displacements in horizontal and vertical directions can be defined.

An example of a satellite being used is the Sentinel-1, launched in mid-2015 by the European Space Agency. This satellite information is open-source data. It will have a 6 to 12 day revisit cycle in many locations.

An example of a satellite being used is the Sentinel-1, launched in mid-2015 by the European Space Agency. This satellite information is open-source data. It will have a 6 to 12 day revisit cycle in many locations.

The results of an InSAR displacement survey are typically shown as a series of colored data points, typically coloured green for the stable points, trending to yellow and red for points that are moving.

This blog has some example images.

Some Limitations With InSAR

There are some limitations with InSAR, so it can only be part of a monitoring program. These limitations are:

-

The displacement direction is only measured in the direction of the satellite. Hence one may not know in which direction the movement is occurring. The magnitude of displacement could be underestimated depending on the apparent angle of measurement.

-

The movement being measured could consist of vertical settlement due to material consolidation and may not be horizontal and related to impending failure.

-

The displacement magnitude measured on opposite sides of a facility may have different accuracy, depending on the slope orientation versus the line-of-sight.

-

Areas with heavy vegetation may be difficult to monitor

-

Areas with heavy or persistent cloud cover can be difficult to monitor.

-

Areas with snow cover will be difficult to monitor.

-

The satellite return period may be weekly or every two weeks, so one is not able to analyze daily movements if a situation is critical. If the return visit day has cloud cover, there will be no new satellite data collected.

-

Areas with on-going construction or tailings deposition will lead to erroneous results.

-

Due to the line of sight, not all slope failure modes may be detectible (for example piping failure).

Regardless of these limitations, InSAR can still play a role in any monitoring program since it is able to monitor large areas quickly. Consider it as a pre-screening tool, being aware that not all failure modes may be detectible with it.

Discussion

On LinkedIn, one can see numerous posts where independent experts are examining historical InSAR data for recent failures to see whether early movement should have been detected. The results seem to be quite positive in that areas that have failed might have been red-flagged prior to failure.

On LinkedIn, one can see numerous posts where independent experts are examining historical InSAR data for recent failures to see whether early movement should have been detected. The results seem to be quite positive in that areas that have failed might have been red-flagged prior to failure.

There are also zones that showed critical displacements but have not failed.

Typically, there are four ways to monitor displacement in pit slopes, tailings dams, heap leach pads, and waste dumps. They are:

-

Insitu monitoring using embedded instruments, for example slope indicators, extensometers, and settlement gauges. These instruments provide information on what is happening internally within a slope, where actual movement is occurring, and they can be used in warning alert systems.

-

Surface monitoring using radar (ground based InSAR) systems and survey prisms. These tools measure only surface movements in selected areas, can be monitored as frequently as needed on an automated basis, and integrated into warning alert systems.

-

Drone or aerial surveys can be used to measure topography and monitor movements over large areas. This method requires a data processing delay (not real time) to derive the movement information, but such surveys can be done as frequently as needed.

-

InSAR from satellite can be used over very large regions to highlight areas with movement. That should trigger the implementation of one or more of the other monitoring approaches (if not already in place).

Conclusion

A mining site consists of numerous constructed embankments and slopes of all types and heights. Many of these slopes may be creeping and moving all the time – it’s a living beast.

A mining site consists of numerous constructed embankments and slopes of all types and heights. Many of these slopes may be creeping and moving all the time – it’s a living beast.

Recently I have been seeing more mining studies proposing to use the dry stack approach. In some cases, they no longer even do the typical tailings trade-off study that look at different options. The decision is made upfront that dry stack is the preferred route due to its environmental acceptability and positive perceptions.

Recently I have been seeing more mining studies proposing to use the dry stack approach. In some cases, they no longer even do the typical tailings trade-off study that look at different options. The decision is made upfront that dry stack is the preferred route due to its environmental acceptability and positive perceptions. The Guide covers several topics, including tailings characterization; site closure concepts; filtered tailings stack design; material transport, stacking systems; and tailings dewatering methods. The Guide covers all the basics very well. The one area that jumped out at me is the tailings characterization and testing aspect.

The Guide covers several topics, including tailings characterization; site closure concepts; filtered tailings stack design; material transport, stacking systems; and tailings dewatering methods. The Guide covers all the basics very well. The one area that jumped out at me is the tailings characterization and testing aspect. Major miners, such as BHP and Rio Tinto, typically spare no expense on material testing for metallurgical or geotechnical purposes. They have the funds available to test and engineer to a high level to adequately de-risk the project to meet their investment thresholds.

Major miners, such as BHP and Rio Tinto, typically spare no expense on material testing for metallurgical or geotechnical purposes. They have the funds available to test and engineer to a high level to adequately de-risk the project to meet their investment thresholds.

The lesson is that QP’s signing off on technical information for clients should be proficient in the nature of their work and need to know the reporting rules very well. Some of these incidents involve error and poor judgment, not outright fraud.

The lesson is that QP’s signing off on technical information for clients should be proficient in the nature of their work and need to know the reporting rules very well. Some of these incidents involve error and poor judgment, not outright fraud. 43-101 regulations state that “An issuer must not file a technical report that contains a disclaimer by any qualified person responsible for preparing or supervising the preparation of all or part of the report that

43-101 regulations state that “An issuer must not file a technical report that contains a disclaimer by any qualified person responsible for preparing or supervising the preparation of all or part of the report that This ends Part 2 of this blog post. It hopefully highlights the importance of QP’s being knowledgably on the disclosure rules and the technical aspects of what they are hired to do.

This ends Part 2 of this blog post. It hopefully highlights the importance of QP’s being knowledgably on the disclosure rules and the technical aspects of what they are hired to do. The focus of this blog is on the types of activities that raised the red flags in the past. I am less interested in naming the people responsible, although the associated web links do provide more detail on the events.

The focus of this blog is on the types of activities that raised the red flags in the past. I am less interested in naming the people responsible, although the associated web links do provide more detail on the events. This ends Part 1 of this blog post. Part 2 will continue with a few more examples, specifically involving Qualified Persons, and can be found at this link

This ends Part 1 of this blog post. Part 2 will continue with a few more examples, specifically involving Qualified Persons, and can be found at this link

So, you just completed your initial PEA cashflow model and the resulting NPV and IRR are a little disappointing. They are not what everyone was expecting. They don’t meet the ideal targets of an IRR greater than 30% and an NPV that is more than 2x the initial capital cost. The project could now be on life support in the eyes of some.

So, you just completed your initial PEA cashflow model and the resulting NPV and IRR are a little disappointing. They are not what everyone was expecting. They don’t meet the ideal targets of an IRR greater than 30% and an NPV that is more than 2x the initial capital cost. The project could now be on life support in the eyes of some. The discounting of cashflows in a cashflow model means that up-front revenues and costs have a bigger impact on the final economics than those far off in the future. This effect is amplified at higher discount rates.

The discounting of cashflows in a cashflow model means that up-front revenues and costs have a bigger impact on the final economics than those far off in the future. This effect is amplified at higher discount rates. ake to the cashflow model. Sometimes several of the small ones, when compounded together, will result in a significant impact. Here are some of the other cashflow model adjustments that I have seen.

ake to the cashflow model. Sometimes several of the small ones, when compounded together, will result in a significant impact. Here are some of the other cashflow model adjustments that I have seen. Don’t let a disappointing NPV get you down. There may be a few ways to boost the NPV by applying some common practices. However, if after applying all of these adjustments, the NPV still isn’t great, something bigger may be required. That could be an entire project scope re-think.

Don’t let a disappointing NPV get you down. There may be a few ways to boost the NPV by applying some common practices. However, if after applying all of these adjustments, the NPV still isn’t great, something bigger may be required. That could be an entire project scope re-think.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times. Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its service, smoothing the ore delivery to the plant.

Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its service, smoothing the ore delivery to the plant. Once the schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

Once the schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate. These two blog posts hopefully give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

These two blog posts hopefully give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

So I thought what better way to explain the mining engineer role than by describing the anatomy of a typical Chapter 16 (MINING) in a 43-101 Technical Report. That chapter is a good example of the range of tasks typically undertaken by mining engineers.

So I thought what better way to explain the mining engineer role than by describing the anatomy of a typical Chapter 16 (MINING) in a 43-101 Technical Report. That chapter is a good example of the range of tasks typically undertaken by mining engineers. There is always a mineral resource estimate available before doing a PEA. The way the resource is reported will indicate what type of mine this likely is. The geologists have already done some of the mining engineer’s work.

There is always a mineral resource estimate available before doing a PEA. The way the resource is reported will indicate what type of mine this likely is. The geologists have already done some of the mining engineer’s work. Before starting pit optimization, we require economic inputs from several people. The base case metal prices must be selected (normally with input from the client). The mining operating cost per tonne must be estimated (by the mining engineer). The processing engineers will provide the processing cost and recovery for each ore type.

Before starting pit optimization, we require economic inputs from several people. The base case metal prices must be selected (normally with input from the client). The mining operating cost per tonne must be estimated (by the mining engineer). The processing engineers will provide the processing cost and recovery for each ore type. Once the optimization is run, a series of nested pit shells are created, each with its own tonnes and grade. These shells are compared for incremental strip ratio, incremental head grade, total tonnes, and contained metal.

Once the optimization is run, a series of nested pit shells are created, each with its own tonnes and grade. These shells are compared for incremental strip ratio, incremental head grade, total tonnes, and contained metal. The mining engineer is now ready to undertake the pit design. The pit design step introduces a benched slope profile, smooths out the pit shape, and adds haulroads. Hence a couple of key input parameters are required at this time. The mining engineer will need to know the geotechnical pit slope criteria and the truck size & haul road widths. Let’s look at both of these.

The mining engineer is now ready to undertake the pit design. The pit design step introduces a benched slope profile, smooths out the pit shape, and adds haulroads. Hence a couple of key input parameters are required at this time. The mining engineer will need to know the geotechnical pit slope criteria and the truck size & haul road widths. Let’s look at both of these.

Ramps: Next the mining engineer needs to select the truck size, even though the production schedule has not yet been created.

Ramps: Next the mining engineer needs to select the truck size, even though the production schedule has not yet been created.

On YouTube, there are also a lot of educational videos related to mining. Some of the same audio podcast episodes are also available on the YouTube platform. Given an option, I prefer the audio-only podcast format over YouTube.

On YouTube, there are also a lot of educational videos related to mining. Some of the same audio podcast episodes are also available on the YouTube platform. Given an option, I prefer the audio-only podcast format over YouTube. Mining Stock Education (680 episodes)

Mining Stock Education (680 episodes)  Fresh Thinking by Optiro-Snowden (53 episodes) This podcast is hosted by Snowdon – Optiro consultants. They typically focus on resource modelling and grade reconciliation aspects. The episodes are fairly short (15 mins), which is nice. Although I am not a resource modeller, I can always learn more about the black art of resource modelling.

Fresh Thinking by Optiro-Snowden (53 episodes) This podcast is hosted by Snowdon – Optiro consultants. They typically focus on resource modelling and grade reconciliation aspects. The episodes are fairly short (15 mins), which is nice. Although I am not a resource modeller, I can always learn more about the black art of resource modelling. There is no shortage of material in the podcast world about the mining industry. It all depends on what interests you the most. There is even more mining information available on YouTube, if you have the time to sit and watch videos. Nevertheless the audio-only platform is great, although you don’t get to see the charts being discussed. That’s fine with me, particularly if they take a few seconds to describe the chart.

There is no shortage of material in the podcast world about the mining industry. It all depends on what interests you the most. There is even more mining information available on YouTube, if you have the time to sit and watch videos. Nevertheless the audio-only platform is great, although you don’t get to see the charts being discussed. That’s fine with me, particularly if they take a few seconds to describe the chart.

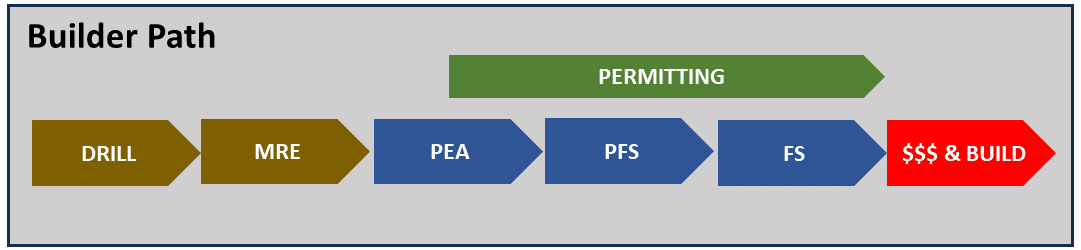

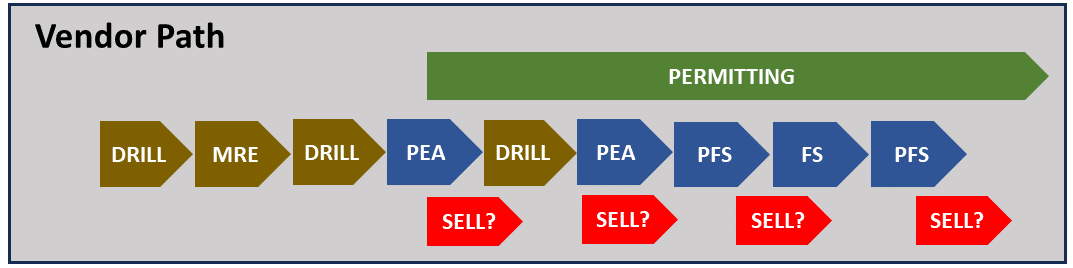

If an engineer understands that a Mine Builder’s project will move from PEA to PFS to FS in rapid succession, then there is more incentive to ensure each study is somewhat integrated.

If an engineer understands that a Mine Builder’s project will move from PEA to PFS to FS in rapid succession, then there is more incentive to ensure each study is somewhat integrated. This post is just a brief discussion of mining project timelines. For those interested, there a few additional project timelines for curiosity purposes. Each path is unique because no two mining projects are the same. You can find these examples at this link “

This post is just a brief discussion of mining project timelines. For those interested, there a few additional project timelines for curiosity purposes. Each path is unique because no two mining projects are the same. You can find these examples at this link “

This article is about the benefit of preparing (cutting) more geological cross-sections and the value they bring.

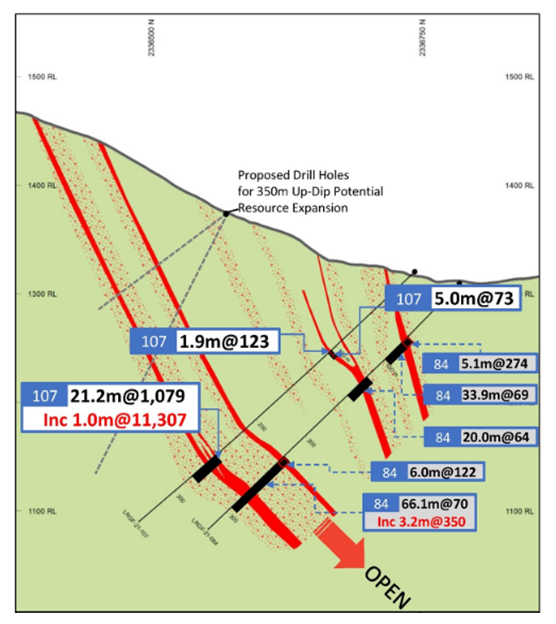

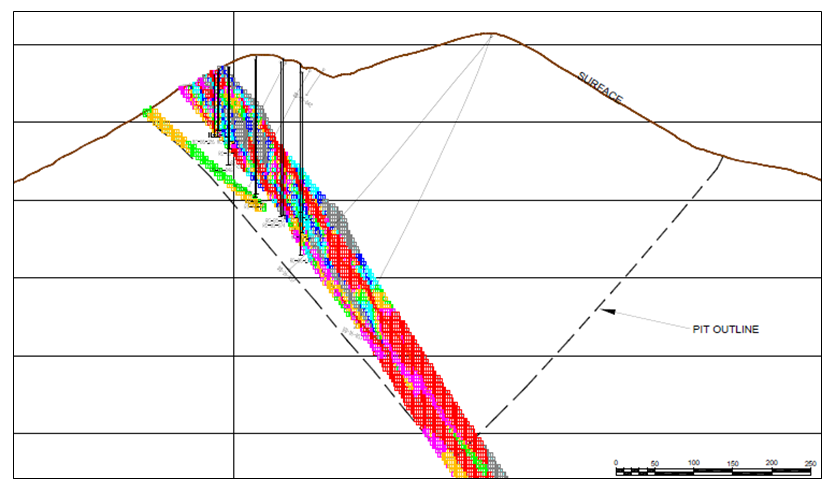

This article is about the benefit of preparing (cutting) more geological cross-sections and the value they bring. Long sections are aligned along the long axis of the deposit. They can be vertically oriented, although sometimes they may be tilted to follow the dip angle of an ore zone.

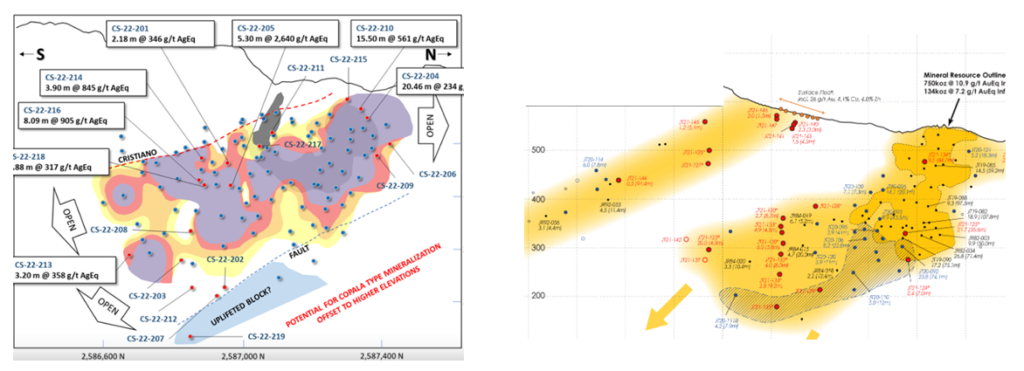

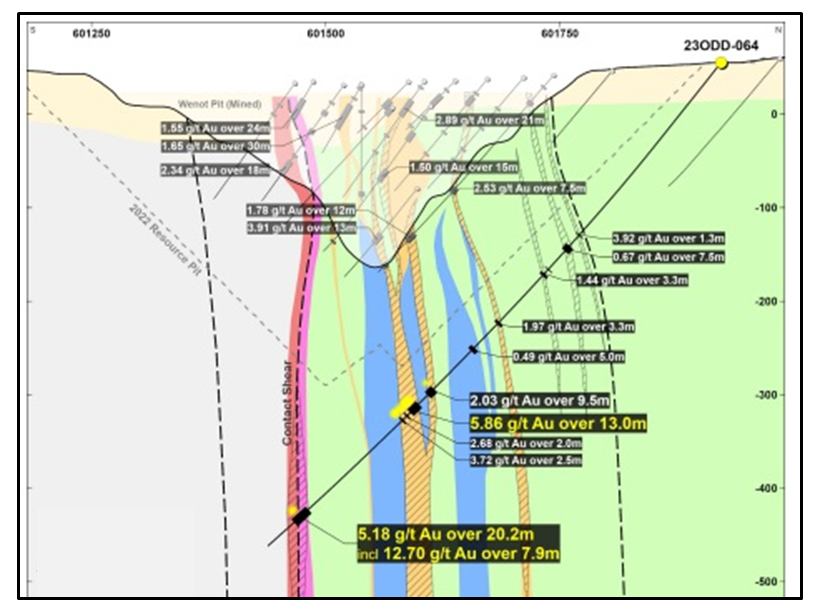

Long sections are aligned along the long axis of the deposit. They can be vertically oriented, although sometimes they may be tilted to follow the dip angle of an ore zone. When looking at cross-sections, it is always important to look at multiple cross-sections across the orebody. Too often in reports one may be presented with the widest and juiciest ore zone, as if that was typical for the entire orebody. It likely is not typical.

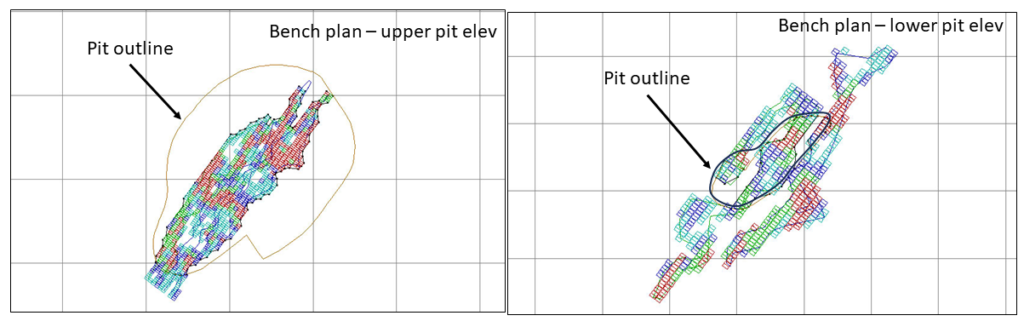

When looking at cross-sections, it is always important to look at multiple cross-sections across the orebody. Too often in reports one may be presented with the widest and juiciest ore zone, as if that was typical for the entire orebody. It likely is not typical. Bench plans (or level plans) are horizontal slices across the ore body at various elevations. In these sections one is looking down on the orebody from above.

Bench plans (or level plans) are horizontal slices across the ore body at various elevations. In these sections one is looking down on the orebody from above. 3D PDF files can be created by some of the geological software packages. They can export specific data of interest; for example topography, ore zone wireframes, underground workings, and block model information. These 3D files allows anyone to rotate an image, zoom in as needed and turn layers off and on.

3D PDF files can be created by some of the geological software packages. They can export specific data of interest; for example topography, ore zone wireframes, underground workings, and block model information. These 3D files allows anyone to rotate an image, zoom in as needed and turn layers off and on. The different types of geological sections all provide useful information. Don’t focus only on cross-sections, and don’t focus only on one typical section. Create more sections at different orientations to help everyone understand better.

The different types of geological sections all provide useful information. Don’t focus only on cross-sections, and don’t focus only on one typical section. Create more sections at different orientations to help everyone understand better.