A while back I wrote a blog titled “Pre-Concentration – Savior or Not?”. That blog was touting the benefits of pre-concentration. More recently I attended a webinar where the presenter stated that the economics of pre-concentration may not necessarily be as good as we think they are.

My first thought was “this is blasphemy”. However upon further reflection I wondered if it’s true. To answer that question, I modified one of my old cashflow models from a Zn, Pb project using pre-concentration. I adjusted the model to enable running a trade-off, with and without pre-con by varying cost and recovery parameters.

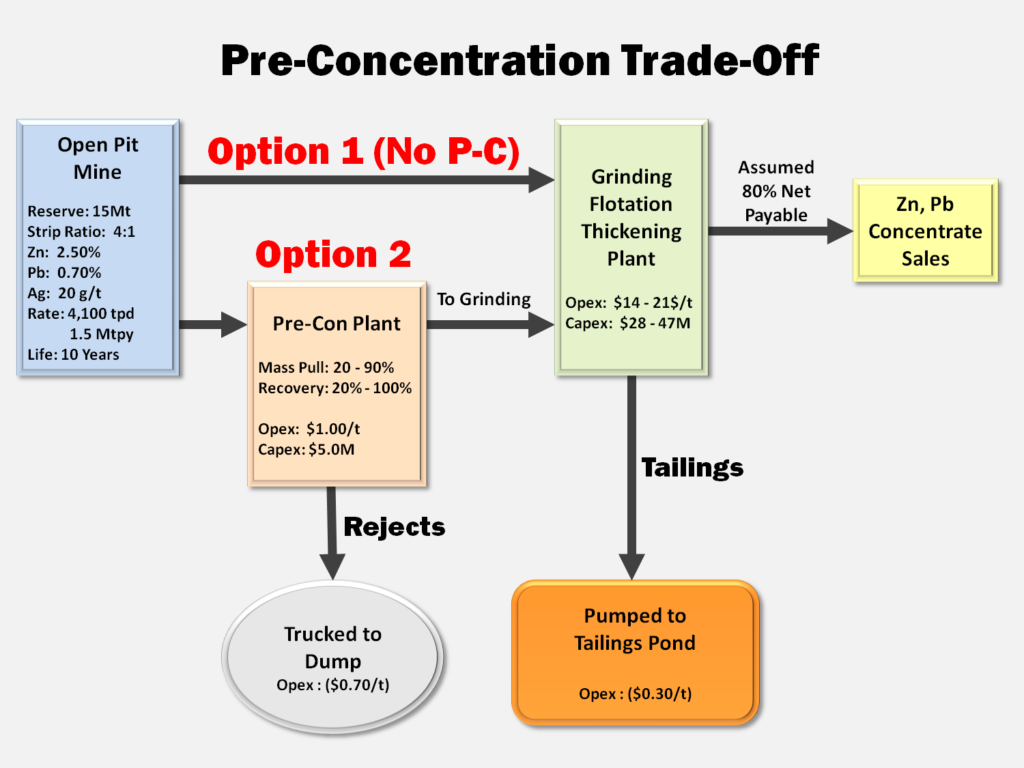

Main input parameters

The trade-off model and some of the parameters are shown in the graphic below. The numbers used in the example are illustrative only, since I am mainly interested in seeing what factors have the greatest influence on the outcome.

The term “mass pull” is used to define the quantity of material that the pre-con plant pulls and sends to the grinding circuit. Unfortunately some metal may be lost with the pre-con rejects. The main benefit of a pre-con plant is to allow the use of a smaller grinding/flotation circuit by scalping away waste. This will lower the grinding circuit capital cost, albeit slightly increase its unit operating cost.

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

Another one of the cost differences is tailings handling. The pre-con rejects likely must be trucked to a final disposal location while flotation tails can be pumped. I assumed a low pumping cost, i.e to a nearby pit.

The pre-con plant doesn’t eliminate a tailings pond, but may make it smaller based on the mass pull factor. The most efficient pre-concentration plant from a tailings handling perspective is shown on the right.

The outcome

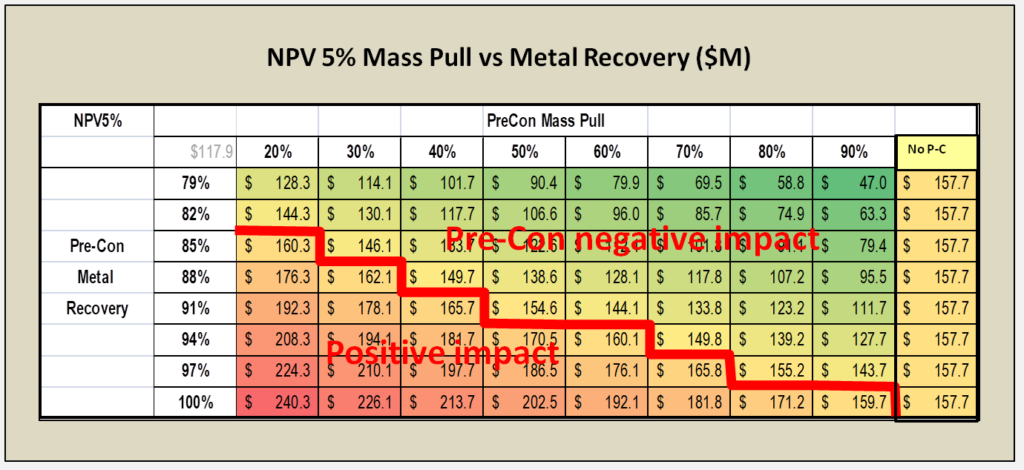

The findings of the trade-off surprised me a little bit. There is an obvious link between pre-con mass pull and overall metal recovery. A high mass pull will increase metal recovery but also results in more tonnage sent to grinding. At some point a high mass pull will cause one to ask what’s the point of pre-con if you are still sending a high percentage of material to the grinding circuit.

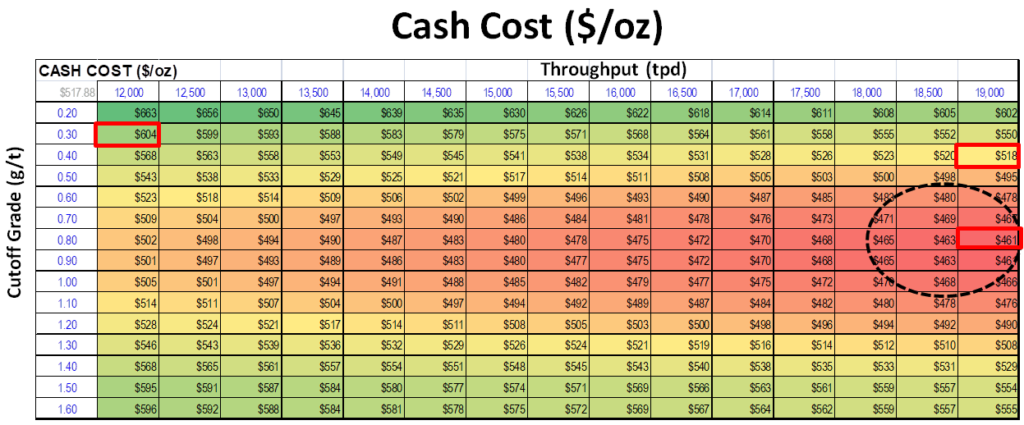

The table below presents the NPV for different mass pull and recovery combinations. The column on the far right represents the NPV for the base case without any pre-con plant. The lower left corner of the table shows the recovery and mass pull combinations where the NPV exceeds the base case. The upper right are the combinations with a reduction in NPV value.

The width of this range surprised me showing that the value generated by pre-con isn’t automatic. The NPV table shown is unique to the input assumptions I used and will be different for every project.

The economic analysis of pre-concentration does not include the possible benefits related to reduced water and energy consumption. These may be important factors for social license and permitting purposes, even if unsupported by the economics. Here’s an article from ThermoFisher on this “How Bulk Ore Sorting Can Reduce Water and Energy Consumption in Mining Operations“.

Conclusion

The objective of this analysis isn’t to demonstrate the NPV of pre-concentration. The objective is to show that pre-concentration might or might not make sense depending on a project’s unique parameters. The following are some suggestions:

1. Every project should at least take a cursory look at pre-concentration to see if it is viable. This should be done on all projects, even if it’s only a cursory mineralogical assessment level.

2. Make certain to verify that all ore types in the deposit are amenable to the same pre-concentration circuit. This means one needs to have a good understanding of the ore types that will be encountered.

3. Anytime one is doing a study using pre-concentration, one should also examine the economics without it. This helps to understand the economic drivers and the risks. You can then decide whether it is worth adding another operating circuit in the process flowsheet that has its own cost and performance risk. The more processing components added to a flow sheet, the more overall plant availability may be effected.

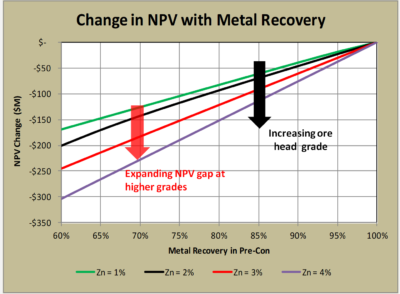

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

5. In my opinion, the best time to decide on pre-con would be at the PEA stage. Although the amount of testing data available may be limited, it may be sufficient to assess whether pre-con warrants further study.

6. Don’t fall in love with or over promote pre-concentration until you have run the economics. It can make it harder to retract the concept if the economics aren’t there.

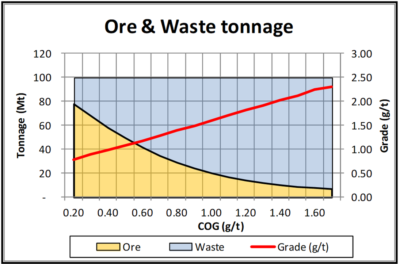

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

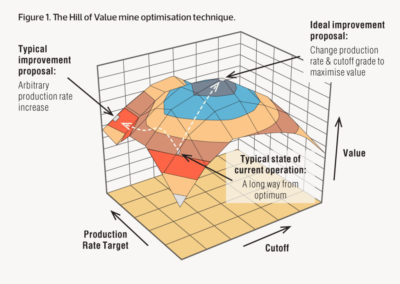

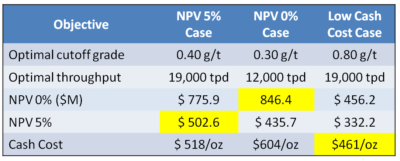

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

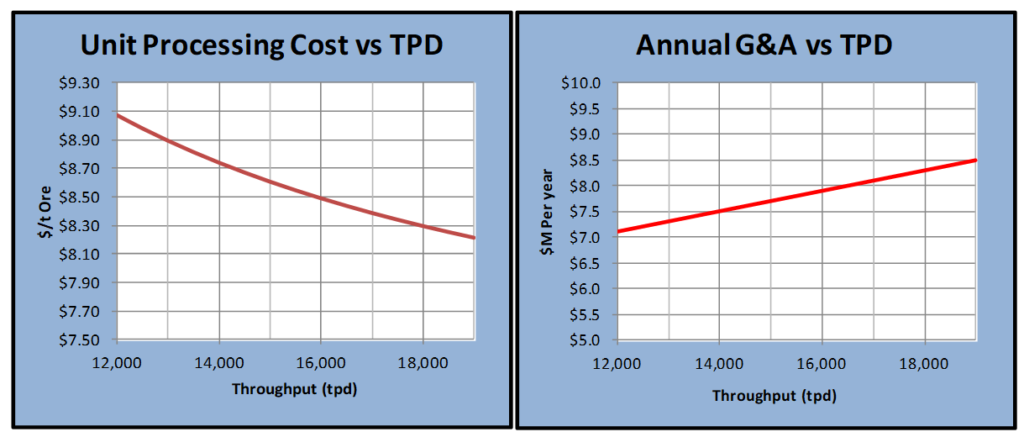

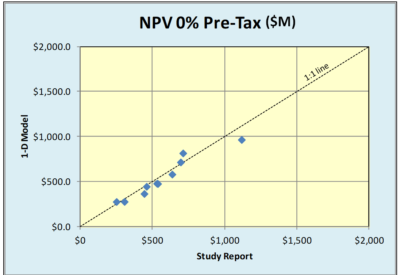

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model.

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model. There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

We often see junior mining companies benchmarking themselves against others. Sometimes corporate presentations provide graphs of enterprise value per gold ounce to demonstrate that a company might be undervalued.

We often see junior mining companies benchmarking themselves against others. Sometimes corporate presentations provide graphs of enterprise value per gold ounce to demonstrate that a company might be undervalued. Lenders may have observers at site monitoring both construction progress and cash expenditures. Shareholders and analysts are watching for news releases that update the capital spending. Their concern is well founded due to several significant cost over-run instances.

Lenders may have observers at site monitoring both construction progress and cash expenditures. Shareholders and analysts are watching for news releases that update the capital spending. Their concern is well founded due to several significant cost over-run instances. It would be a good thing if the mining industry (or other concerned parties) work together to create open source project databases. These would incorporate summary information and cost information for global mining projects. The information is already out there, it just needs to be compiled.

It would be a good thing if the mining industry (or other concerned parties) work together to create open source project databases. These would incorporate summary information and cost information for global mining projects. The information is already out there, it just needs to be compiled. Benchmarking can be a great tool when done correctly. Benchmarking capital costs might bring more transparency to the project development process. It may help convince nervous investors that the proposed costs are reasonable.

Benchmarking can be a great tool when done correctly. Benchmarking capital costs might bring more transparency to the project development process. It may help convince nervous investors that the proposed costs are reasonable.

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due.

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due. I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play.

I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play. Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now.

Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now. It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

In general to get financing and investor interest, development projects must demonstrate a high NPV, high IRR, and short payback period. This requirement tends to apply more to the small and mid tiered companies than to the major companies. The majors normally have different access to financing.

In general to get financing and investor interest, development projects must demonstrate a high NPV, high IRR, and short payback period. This requirement tends to apply more to the small and mid tiered companies than to the major companies. The majors normally have different access to financing. There are several scenarios where NPV analysis decision making may conflict with the objectives of sustainable mining. Here are a few examples.

There are several scenarios where NPV analysis decision making may conflict with the objectives of sustainable mining. Here are a few examples. 4. Low grade ore stockpiling can help to increase early revenue and profit, thereby improving the project NPV and payback. Stockpiling of low grade and prioritization of high grade means that lower grade ore will be processed in the later stages of the project life. Who hasn’t been happy to develop a mine schedule with the grade profile shown on the right?

4. Low grade ore stockpiling can help to increase early revenue and profit, thereby improving the project NPV and payback. Stockpiling of low grade and prioritization of high grade means that lower grade ore will be processed in the later stages of the project life. Who hasn’t been happy to develop a mine schedule with the grade profile shown on the right? 7. Accelerated depreciation, tax and royalty holidays are types of economic factors that will improve NPV and early payback. They are one tool governments use to promote economic activity. These tax holidays will greatly enhance the NPV when combined with high grading and waste stripping deferral.

7. Accelerated depreciation, tax and royalty holidays are types of economic factors that will improve NPV and early payback. They are one tool governments use to promote economic activity. These tax holidays will greatly enhance the NPV when combined with high grading and waste stripping deferral. NPV is one of the standard metrics used to make project decisions. The deferral of upfront costs in lieu of future costs is favorable for cashflow and investor returns. Similarly, increasing early revenue at the expense of future revenue does the same. Both approaches will help satisfy the financing concerns. However they may not be advantageous for creating long term sustainable projects.

NPV is one of the standard metrics used to make project decisions. The deferral of upfront costs in lieu of future costs is favorable for cashflow and investor returns. Similarly, increasing early revenue at the expense of future revenue does the same. Both approaches will help satisfy the financing concerns. However they may not be advantageous for creating long term sustainable projects.

I was at the 2019 Progressive Mine Forum in Toronto and a presentation was given on underground compressed air storage. The company was Hydrostor (

I was at the 2019 Progressive Mine Forum in Toronto and a presentation was given on underground compressed air storage. The company was Hydrostor (

Converting an abandoned mine into a power storage facility will still have its challenges. Cost and economic uncertainty are part of that. In addition, permitting such a facility will still require some environmental study.

Converting an abandoned mine into a power storage facility will still have its challenges. Cost and economic uncertainty are part of that. In addition, permitting such a facility will still require some environmental study.

In the past there would be binders with detailed calculations and backup for the different parts of the study. Typically there was a binder for the Executive Summary and separate sections (i.e. binders) for Geology, Mining, Processing, Infrastructure, Capital Cost, Operating Cost, Environmental, Project Execution, and Economic Analysis, etc.

In the past there would be binders with detailed calculations and backup for the different parts of the study. Typically there was a binder for the Executive Summary and separate sections (i.e. binders) for Geology, Mining, Processing, Infrastructure, Capital Cost, Operating Cost, Environmental, Project Execution, and Economic Analysis, etc. The original intent of the 43-101 Technical Report was for it to be a summary document, only about 80-150 pages in length. The intent was to simplify all the technical work for the benefit of non-technical investors. Currently I have noticed that in many cases the 43-101 report is now the entire feasibility study document.

The original intent of the 43-101 Technical Report was for it to be a summary document, only about 80-150 pages in length. The intent was to simplify all the technical work for the benefit of non-technical investors. Currently I have noticed that in many cases the 43-101 report is now the entire feasibility study document. My recommendation is that, where budgets permit, mining companies return to the days of preparing the comprehensive feasibility study document. It’s the right thing to do.

My recommendation is that, where budgets permit, mining companies return to the days of preparing the comprehensive feasibility study document. It’s the right thing to do. If any mining industry credibility has been lost, re-establishing it should be important. One way to start doing this is to focus on creating the type of reports that best serve the needs of the industry stakeholders.

If any mining industry credibility has been lost, re-establishing it should be important. One way to start doing this is to focus on creating the type of reports that best serve the needs of the industry stakeholders.

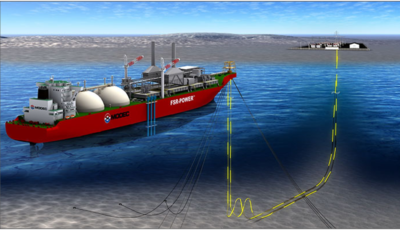

The technology consists of a floating LNG (liquefied natural gas) turbine power plant combined with high capacity seawater desalinization capabilities. MODEC is offering the FSRWP® (Floating Storage Regasification Water-Desalination & Power-Generation) system.

The technology consists of a floating LNG (liquefied natural gas) turbine power plant combined with high capacity seawater desalinization capabilities. MODEC is offering the FSRWP® (Floating Storage Regasification Water-Desalination & Power-Generation) system. From a green mining perspective, the FSRWP produces clean power with the highest thermal efficiency and lowest carbon foot-print.

From a green mining perspective, the FSRWP produces clean power with the highest thermal efficiency and lowest carbon foot-print. Currently there are three mooring options for the floating system that should fit most any tidewater situation.

Currently there are three mooring options for the floating system that should fit most any tidewater situation. The bottom line is that if your mining project is near shore, and has both water supply and power issues, take a look at the FSRWP technology. One might say it is greener technology by using LNG (rather than coal, heavy fuel oil, or diesel) to generate power. At the same time it avoids competition with locals for access to fresh water.

The bottom line is that if your mining project is near shore, and has both water supply and power issues, take a look at the FSRWP technology. One might say it is greener technology by using LNG (rather than coal, heavy fuel oil, or diesel) to generate power. At the same time it avoids competition with locals for access to fresh water.

Each year business leaders are queried about what they view as their major risks. The survey results are summarized in the Global Risk Report.

Each year business leaders are queried about what they view as their major risks. The survey results are summarized in the Global Risk Report.

It is also interesting to look at the detailed 10 year table in the report to see how the risk perceptions have changed over the last decade.

It is also interesting to look at the detailed 10 year table in the report to see how the risk perceptions have changed over the last decade.