Normally at the start of a mining study, the team members receive a matrix of responsibilities. This table shows which people (or groups) are responsible for different aspects of the study, i.e. who is responsible for geology, for mine design, for process design, infrastructure, etc. This is great tool and a necessity in making sure that everyone knows what they are supposed to do.

Next we generate a project schedule based on some work plan. In realty this isn’t the correct sequence.

Sometimes the WBS is forgotten

What often gets forgotten in early stage studies is providing the team members a Work Breakdown Structure (“WBS”). I consider the WBS an equally important component as the responsibility matrix and both should always be provided.

The WBS is a hierarchical breakdown of the project into phases, deliverables, and work packages usually associated with cost estimation. It is a tree based structure, developed by starting with the final objective and then dividing that into manageable components based on size, duration, and responsibility. Typically this is done for the capital cost estimate, breaking it down into individual cost areas and cost components. A WBS can also be used for the operating cost estimate.

The WBS can provide the following information to the team:

The WBS can provide the following information to the team:

-

It assigns the costing responsibility to specific people or group so each know what must be delivered.

-

It provides a consistent format for developing and reporting the capital costs (and operating costs).

-

It helps ensure that no cost components get omitted and no costs get double counted.

-

It provides the cashflow modeler with a clean format to import the capital cost into the cashflow model.

-

The WBS should be developed before the project schedule, not after it.

Any study will benefit from a WBS

Typically a WBS is developed for pre-feasibility and feasibility mining studies but is often ignored at the PEA stage. Some feel it is too detailed for that level of study. I don’t feel this is the case.

Typically a WBS is developed for pre-feasibility and feasibility mining studies but is often ignored at the PEA stage. Some feel it is too detailed for that level of study. I don’t feel this is the case.

The WBS is a communication tool to confirm responsibilities. Thus even a simplified WBS is still useful at the PEA stage.

I have seen some instances where a WBS has been created but does not get wide distribution to the entire team. The WBS should be provided to everyone and ideally a team session be held to walk through the WBS structure.

The idea is not make everyone a costing expert, but rather to ensure all understand how the project cost estimate will be structured.

Conclusion

The bottom line is that regardless of the level of study, a WBS should always be created.

The bottom line is that regardless of the level of study, a WBS should always be created.

Some will say the WBS is not required for early stage studies but I have found benefits in having one, at least for the capital cost estimate. Obviously the level of detail in the WBS should be appropriate to the level of the study.

Once the WBS is in place, then go ahead and build your project schedule.

A competent Study Manager can easily create an initial WBS, thereby mitigating some headaches when the final study is being assembled. You may even want a basis WBs at the proposal stage.

By the way, before awarding a study to anyone, try to have a prepared Request for Proposal beforehand. I have written about the benefit of this document in a blog post titled “Request For Proposal (“RFP”) – Always Prepare One“

My entire blog post library can be found at this LINK with topics ranging from geotechnical, financial modelling, and junior mining investing.

There are numerous factors that will influence the successful completion of a study. They can be related to the quality of the technical team, the budget, the time window, and direction from the Owner. However the key factor that I observed is the competency of the Study Manager (or Project Manager).

There are numerous factors that will influence the successful completion of a study. They can be related to the quality of the technical team, the budget, the time window, and direction from the Owner. However the key factor that I observed is the competency of the Study Manager (or Project Manager). The Study Manager also needs to understand the objectives of the Owner and ensure the team is working towards those objectives.

The Study Manager also needs to understand the objectives of the Owner and ensure the team is working towards those objectives. Often the Environmental Impact Assessment is being conducted concurrently with an engineering study. The level of internal and external communication now becomes even more critical due to the large number of new technical disciplines involved.

Often the Environmental Impact Assessment is being conducted concurrently with an engineering study. The level of internal and external communication now becomes even more critical due to the large number of new technical disciplines involved. The bottom line is that when a project Owner has received proposals for a study and is in the process of awarding that job, the most important consideration is who will be the Study Manager. If possible meet or chat about how they will manage the study and what their experience is. Check references if possible.

The bottom line is that when a project Owner has received proposals for a study and is in the process of awarding that job, the most important consideration is who will be the Study Manager. If possible meet or chat about how they will manage the study and what their experience is. Check references if possible.

One of my past roles was as a mine engineer on the Diavik diamond mine team. Pit geotechnical and hydrogeology were under my domain during project design and permitting from 1997 to 2000.

One of my past roles was as a mine engineer on the Diavik diamond mine team. Pit geotechnical and hydrogeology were under my domain during project design and permitting from 1997 to 2000. The bottom line is that the directional drilling innovation makes a lot of sense and mine operators should take a look at it. It might help improve their pit dewatering systems.

The bottom line is that the directional drilling innovation makes a lot of sense and mine operators should take a look at it. It might help improve their pit dewatering systems.

The RFP sent to bidding consultants should contain (at a minimum) the items listed below. A sole sourced study can have a scaled back RFP document, but many of these key items should be maintained.

The RFP sent to bidding consultants should contain (at a minimum) the items listed below. A sole sourced study can have a scaled back RFP document, but many of these key items should be maintained. If a company is competitively bidding the study, it can be easier to compare multiple proposals if certain parts are presented in the exact same format. Usually different consulting firms have their own proposal format, which is fine, however certain sections of the proposal should be made easily comparable.

If a company is competitively bidding the study, it can be easier to compare multiple proposals if certain parts are presented in the exact same format. Usually different consulting firms have their own proposal format, which is fine, however certain sections of the proposal should be made easily comparable.

Data rooms are typically created for due diligence exercises, or during advanced an engineering stage. Regardless of the purpose, it is helpful for all involved to have a document control person who understands what is in the data room, what is important, and what is non-essential.

Data rooms are typically created for due diligence exercises, or during advanced an engineering stage. Regardless of the purpose, it is helpful for all involved to have a document control person who understands what is in the data room, what is important, and what is non-essential.

Independent consultants will differentiate themselves from large engineering firms in several ways.

Independent consultants will differentiate themselves from large engineering firms in several ways.

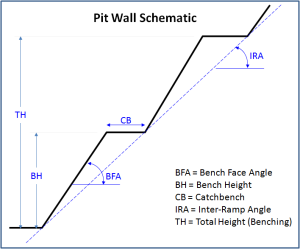

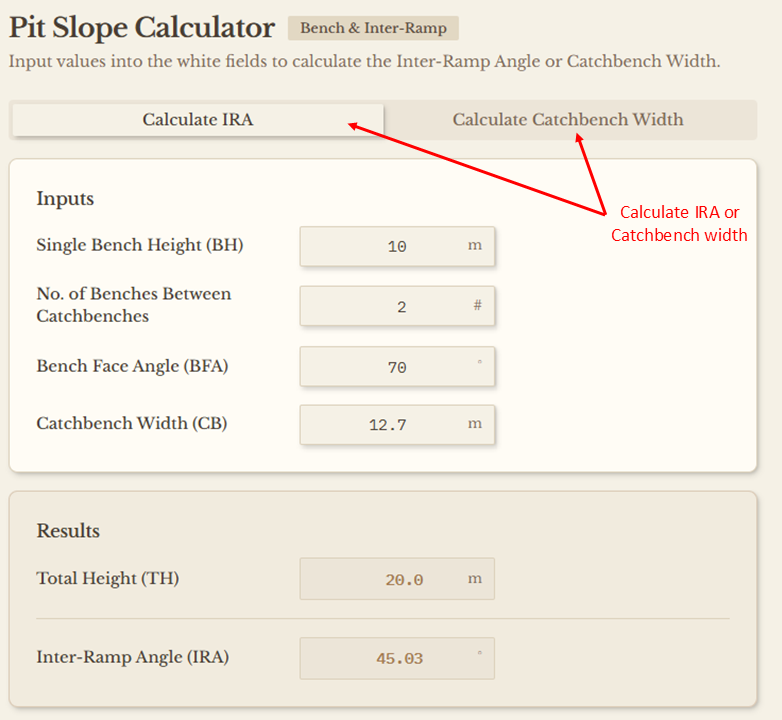

An open pit wall will consist of a series of stacked benches. Geotechnical engineers will normally provide the pit slope design criteria based on the inter-ramp angle (“IRA”) for various sectors around the pit. The IRA represents the toe-to-toe slope angle, as shown in the diagram below.

An open pit wall will consist of a series of stacked benches. Geotechnical engineers will normally provide the pit slope design criteria based on the inter-ramp angle (“IRA”) for various sectors around the pit. The IRA represents the toe-to-toe slope angle, as shown in the diagram below.

I have heard from geologist colleagues that financing grass-roots exploration is still extremely difficult. That is unless company management has had past successes or is well connected to the money scene.

I have heard from geologist colleagues that financing grass-roots exploration is still extremely difficult. That is unless company management has had past successes or is well connected to the money scene. The bottom line is that in order for a project (and the management team) to get serious attention from potential investors is to make sure there is a realistic view of the project itself and have a realistic path forward.

The bottom line is that in order for a project (and the management team) to get serious attention from potential investors is to make sure there is a realistic view of the project itself and have a realistic path forward.

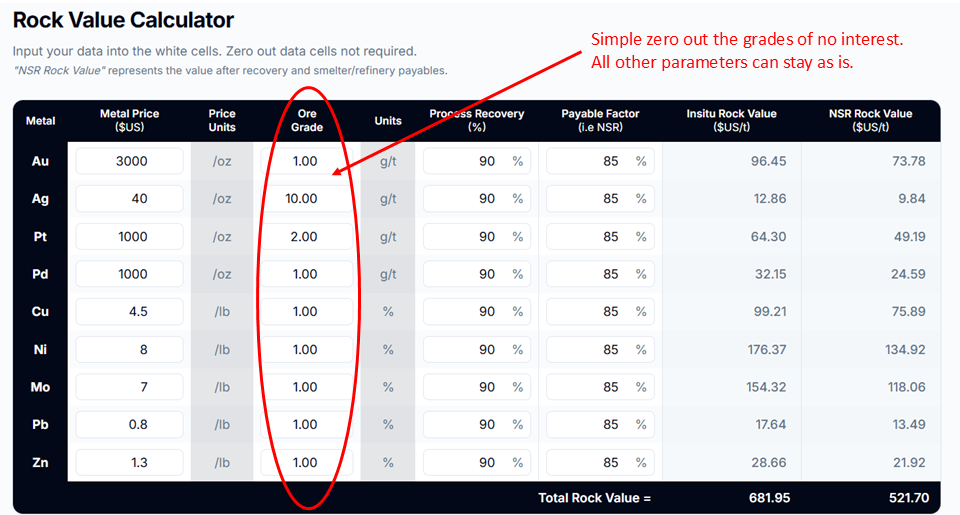

In my view, one of the most important things you need to understand about your orebody is the insitu rock value. Hopefully it is economic, i.e. an ore value. Its the key driver in shaping the economics of any mining project.

In my view, one of the most important things you need to understand about your orebody is the insitu rock value. Hopefully it is economic, i.e. an ore value. Its the key driver in shaping the economics of any mining project.