The mining industry is always on the lookout for new innovations as it strives to keep up with other industries. In that light, periodically I like to highlight new technologies that I become aware of. I’m trying to help spread the word about them, which in turn may assist them in their on-going growth and development.

In this article I want to briefly describe two hardware / software companies that are working on technologies related to mine equipment productivity. In no particular order, the two companies are Loadscan and SedimentIQ. SedimentIQ is more of a startup than Loadscan which has a longer operating track record.

These technology companies are both targeting the open pit and underground markets, looking to provide simpler and less costly productivity solutions. Their technologies may be well suited for small to mid tier mines that cannot afford or don’t require the comprehensive Minestar type fleet management systems.

For the record, I get no fee or commission for promoting these companies; I just like what they are doing.

Loadscan

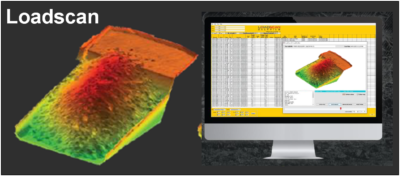

Loadscan has been around for a few years, but I only became aware of it recently. It is a technology that allows the rapid assessment of the load being carried in truck. It does not rely on the use of load cells or weigh scales to measure the payload.

Loadscan has been around for a few years, but I only became aware of it recently. It is a technology that allows the rapid assessment of the load being carried in truck. It does not rely on the use of load cells or weigh scales to measure the payload.

Instead Loadscan uses a laser scanner and proprietary software to three dimensionally map the surface of the truck payload and then calculate its volume. The results will indicate how consistent and optimal truck loading is volumetrically. One can then calculate the payload tonnage by applying a bulk density.

The Loadscan technology will assess whether trucks are being over or under loaded, whether the loads are off-centre, or whether there is excess carryback on the return trip.

Successive truck payloads can be tracked manually or with RFID tags. A cloud based database and web based dashboard are used to store the data and summarize it. The output can include an image of each individual load.

What is interesting about this technology is that it is simple to install in an operation. It does not require retrofitting of a truck.

What is interesting about this technology is that it is simple to install in an operation. It does not require retrofitting of a truck.

Results are immediate. Loadscan provided an example where a message readout board can let the shovel operator immediately know how well each truck was loaded, resulting in improved education and better performance efficiency.

One can also assess how much better shovel bucket factors are in well blasted rock versus in blocky rock.

The Loadscan system is already in use in several mines globally. The vendors can provide more technical data if you need it.

Their website is https://www.loadscan.com/

SedimentIQ

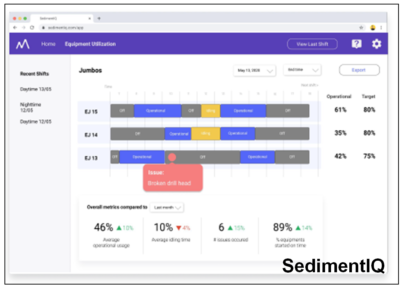

SedimentIQ is a new smartphone vehicle tracking platform that is trying to establish itself. Their proposed technology makes use of a phone’s built-in GPS, Bluetooth, and accelerometer to track vehicle operation. The phone’s sensor can measure vibrations produced by an operating truck or loader.

SedimentIQ is a new smartphone vehicle tracking platform that is trying to establish itself. Their proposed technology makes use of a phone’s built-in GPS, Bluetooth, and accelerometer to track vehicle operation. The phone’s sensor can measure vibrations produced by an operating truck or loader.

Vibration is a fingerprint of a vehicle’s activity. Therefore using machine learning, the SedimentIQ app can produce an “activity score” that decides whether a machine is parked, idling, or performing productive work. The phone is not connected to the machine diagnostics system, so its very easy to install, only needing a power source.

The system will be able to be used on any vehicle, including trucks, drills, loaders, graders, dozers, etc. The system has the capability to monitor equipment location and speed.

In an open pit environment it uses the phone’s GPS to monitor vehicle location. In an underground setting the phone reads inexpensive Bluetooth beacons mounted along the side walls to track location.

The app will identify delay and downtime based on equipment vibration levels. The system currently requires no interaction with the operator, working in the background. Hence it will not identify the cause of delay (i.e. blasting delay, breakdown, inter-equipment delay, etc). I would expect that in the future they could add a feature for the operator to tag delay types on the touch screen.

The SedimentIQ software will aggregate the cycle time and delay information and upload it in real time to a cloud based database. A web-based dashboard allows anyone with access to view the real time production data graphically or export it to Excel.

The SedimentIQ software will aggregate the cycle time and delay information and upload it in real time to a cloud based database. A web-based dashboard allows anyone with access to view the real time production data graphically or export it to Excel.

The SedimentIQ platform is less expensive than high end fleet management software. Although it may not provide all the bells and whistles of the high end software, it may deliver just what you need to monitor productivity in your mining operation. It relies on relatively inexpensive smart phones that are locked to the application.

I recall as a mining student doing time studies. I rode the shift crew bus with pencil in hand, timing the travel from the mine dry to the various shovels to measure start up times. I recall sitting with a stopwatch timing shovel buckets and truck loading times. Both of these tasks can be done for every shift, every truck by equipping the crew bus and mine trucks with the SedimentIQ tech.

The platform is currently being tested at a couple of trials mines and the founders are looking for more mines willing to adopt and further refine their technology. Lets hope they can make a successful go of it.

The website is https://sedimentiq.com/.

Conclusion

Both of these innovative technologies can provide useful information to open pit and underground mine operations. They are in the growth stage, looking for wider adoption. Input from users, whether positive or negative, will assist them with on-going development and enhancements. Their websites obviously have more on what their technology offers, including presentations, white papers, and case studies.

It would be nice to meld these two technologies in some way to allow the SedimentIQ cycle times to also track payloads.

Check them out. Try them out.

The majority of mining projects tend to consist of either open pit only or underground only operations. However there are instances where the orebody is such that eventually the mine must transition from open pit to underground. Open pit stripping ratios can reach uneconomic levels hence the need for the change in direction.

The majority of mining projects tend to consist of either open pit only or underground only operations. However there are instances where the orebody is such that eventually the mine must transition from open pit to underground. Open pit stripping ratios can reach uneconomic levels hence the need for the change in direction. There are several reasons why open pit and underground can be considered as two different projects within the same project.

There are several reasons why open pit and underground can be considered as two different projects within the same project. An underground mine that uses a backfilling method will be able to dispose of some tailings underground. Conversely moving towards a larger open pit will require a larger tailings pond, larger waste dumps and overall larger footprint. This helps make the case for underground mining, particularly where surface area is restricted or local communities are anti-open pit.

An underground mine that uses a backfilling method will be able to dispose of some tailings underground. Conversely moving towards a larger open pit will require a larger tailings pond, larger waste dumps and overall larger footprint. This helps make the case for underground mining, particularly where surface area is restricted or local communities are anti-open pit. Open pit and underground operations will require different skill sets from the perspective of supervision, technical, and operations. Underground mining can be a highly specialized skill while open pit mining is similar to earthworks construction where skilled labour is more readily available globally. Do local people want to learn underground mining skills? Do management teams have the capability and desire to manage both these mining approaches at the same time?

Open pit and underground operations will require different skill sets from the perspective of supervision, technical, and operations. Underground mining can be a highly specialized skill while open pit mining is similar to earthworks construction where skilled labour is more readily available globally. Do local people want to learn underground mining skills? Do management teams have the capability and desire to manage both these mining approaches at the same time? As you can see from the foregoing discussion, there are a multitude of factors playing off one another when examining the open pit to underground cross-over point. It can be like trying to mesh two different projects together.

As you can see from the foregoing discussion, there are a multitude of factors playing off one another when examining the open pit to underground cross-over point. It can be like trying to mesh two different projects together.

This pessimism training started early in my career while working as a geotechnical engineer. Geotechnical engineers were always looking at failure modes and the potential causes of failure when assessing factors of safety.

This pessimism training started early in my career while working as a geotechnical engineer. Geotechnical engineers were always looking at failure modes and the potential causes of failure when assessing factors of safety. When undertaking a due diligence, particularly for a major company or financier, we are not hired to tell them how great the project is. We are hired to look for fatal flaws, identify poorly based design assumptions or errors and omissions in the technical work. We are mainly looking for negatives or red flags.

When undertaking a due diligence, particularly for a major company or financier, we are not hired to tell them how great the project is. We are hired to look for fatal flaws, identify poorly based design assumptions or errors and omissions in the technical work. We are mainly looking for negatives or red flags. It has been my experience that digging in a data room or speaking with the engineering consultants can reveal issues not identifiable in a 43-101 report. Possibly some of these issues were mentioned or glossed over in the report, but you won’t understand the full extent of the issues until digging deeper.

It has been my experience that digging in a data room or speaking with the engineering consultants can reveal issues not identifiable in a 43-101 report. Possibly some of these issues were mentioned or glossed over in the report, but you won’t understand the full extent of the issues until digging deeper. My hesitance in investing in some companies unfortunately can be penalizing. I may end up sitting on the sidelines while watching the rising stock price. Junior mining investors tend to be a positive bunch, when combined with good promotion can result in investors piling into a stock.

My hesitance in investing in some companies unfortunately can be penalizing. I may end up sitting on the sidelines while watching the rising stock price. Junior mining investors tend to be a positive bunch, when combined with good promotion can result in investors piling into a stock. Most times the issue is something we couldn’t fully address given the level of study. We might have been forced to make best guess assumptions to move forward. The review engineers will have their opinions about what assumptions they would have used. Typically the common comment is that our assumption is too optimistic and their assumption would have been more conservative or realistic (in their view).

Most times the issue is something we couldn’t fully address given the level of study. We might have been forced to make best guess assumptions to move forward. The review engineers will have their opinions about what assumptions they would have used. Typically the common comment is that our assumption is too optimistic and their assumption would have been more conservative or realistic (in their view).

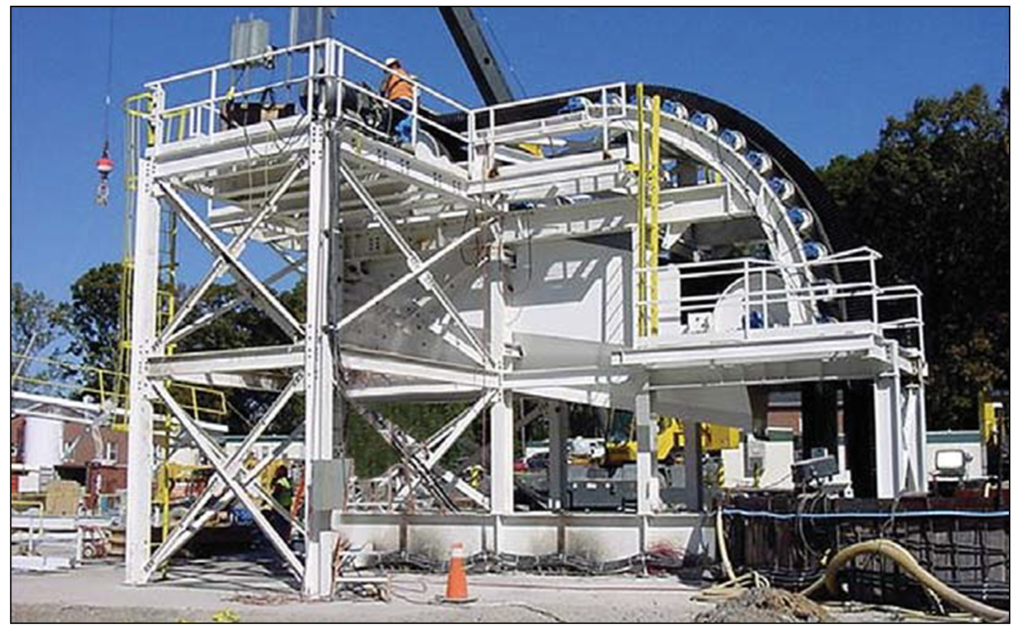

The background information on vertical conveying was provided to me by FKC-Lake Shore, a construction contractor that installs these systems. FKC itself does not fabricate the conveyor hardware. A link to their website is

The background information on vertical conveying was provided to me by FKC-Lake Shore, a construction contractor that installs these systems. FKC itself does not fabricate the conveyor hardware. A link to their website is  The FLEXOWELL®-conveyor system is capable of running both horizontally and vertically, or any angle in between. These conveyors consist of FLEXOWELL®-conveyor belts comprised of 3 components: (i) Cross-rigid belt with steel cord reinforcement; (ii) Corrugated rubber sidewalls; (iii) transverse cleats to prevent material from sliding backwards. They can handle lump sizes varying from powdery material up to 400 mm (16 inch). Material can be raised over 500 metres with reported capacities up to 6,000 tph.

The FLEXOWELL®-conveyor system is capable of running both horizontally and vertically, or any angle in between. These conveyors consist of FLEXOWELL®-conveyor belts comprised of 3 components: (i) Cross-rigid belt with steel cord reinforcement; (ii) Corrugated rubber sidewalls; (iii) transverse cleats to prevent material from sliding backwards. They can handle lump sizes varying from powdery material up to 400 mm (16 inch). Material can be raised over 500 metres with reported capacities up to 6,000 tph. Vendors have evaluated the use of vertical conveying against the use of a conventional vertical shaft hoisting. They report the economic benefits for vertical conveying will be in both capital and operating costs.

Vendors have evaluated the use of vertical conveying against the use of a conventional vertical shaft hoisting. They report the economic benefits for vertical conveying will be in both capital and operating costs. The vendors indicate the conveying system should be able to achieve heights of 700 metres. This may facilitate the use of internal shafts (winzes) to hoist ore from even greater depths in an expanding underground mine. It may be worth a look at your mine.

The vendors indicate the conveying system should be able to achieve heights of 700 metres. This may facilitate the use of internal shafts (winzes) to hoist ore from even greater depths in an expanding underground mine. It may be worth a look at your mine.

Based on my own career, mining has definitely provided me with a chance to travel the world. It will also help anyone overcome their fear of travel. One will also learn that both international and domestic travel can be as equally rewarding. There is nothing wrong with learning more about your own country.

Based on my own career, mining has definitely provided me with a chance to travel the world. It will also help anyone overcome their fear of travel. One will also learn that both international and domestic travel can be as equally rewarding. There is nothing wrong with learning more about your own country.

Business travel has always been one of the best parts of my mining career. I can remember the details about a lot of the travel that I did. Unfortunately the project details themselves will blur with those of other projects.

Business travel has always been one of the best parts of my mining career. I can remember the details about a lot of the travel that I did. Unfortunately the project details themselves will blur with those of other projects.

While waiting for various third-party due diligences to be completed, the company continue to do exploration drilling. There were still a lot of untested showings on the property and geologists need to stay busy.

While waiting for various third-party due diligences to be completed, the company continue to do exploration drilling. There were still a lot of untested showings on the property and geologists need to stay busy. With regards to the Heap Leach PEA, we did not wish to complicate the Feasibility Study by adding a new feed supply to that plant from mixed CIL/HL pits. The heap leach project was therefore considered as a separate satellite operation.

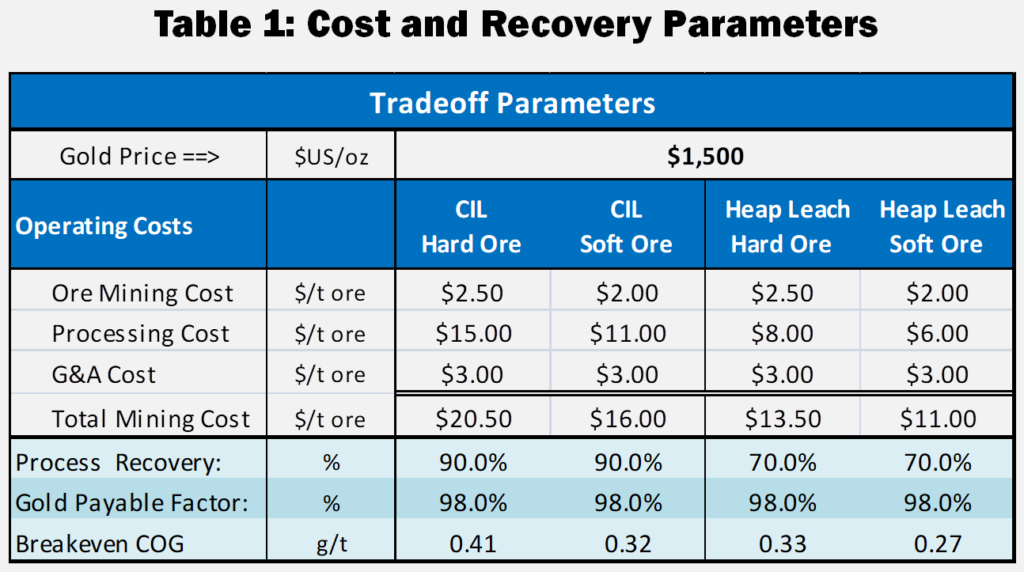

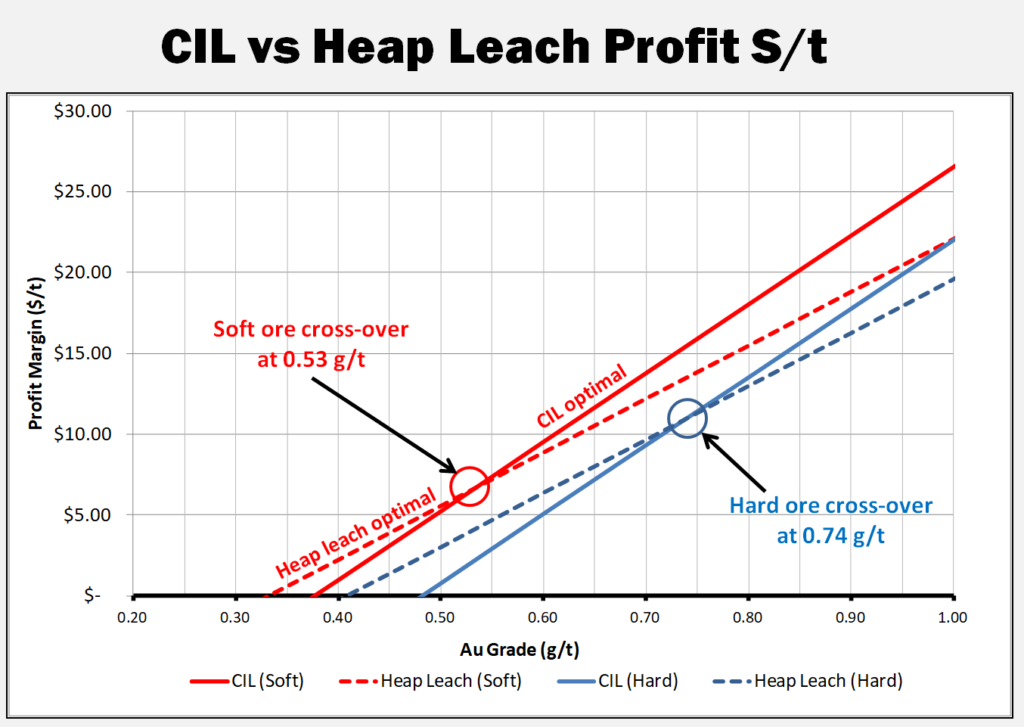

With regards to the Heap Leach PEA, we did not wish to complicate the Feasibility Study by adding a new feed supply to that plant from mixed CIL/HL pits. The heap leach project was therefore considered as a separate satellite operation. I have updated and simplified the trade-off analysis for this blog. Table 1 provides the costs and recoveries used herein, including increasing the gold price to $1500/oz.

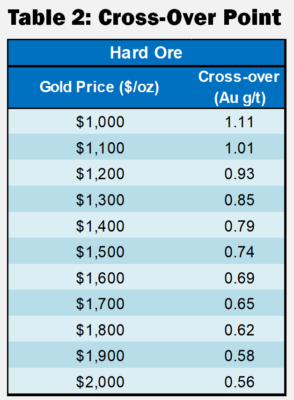

I have updated and simplified the trade-off analysis for this blog. Table 1 provides the costs and recoveries used herein, including increasing the gold price to $1500/oz. These cross-over points described in Table 2 are relevant only for the costs shown in Table 1 and will be different for each project.

These cross-over points described in Table 2 are relevant only for the costs shown in Table 1 and will be different for each project.

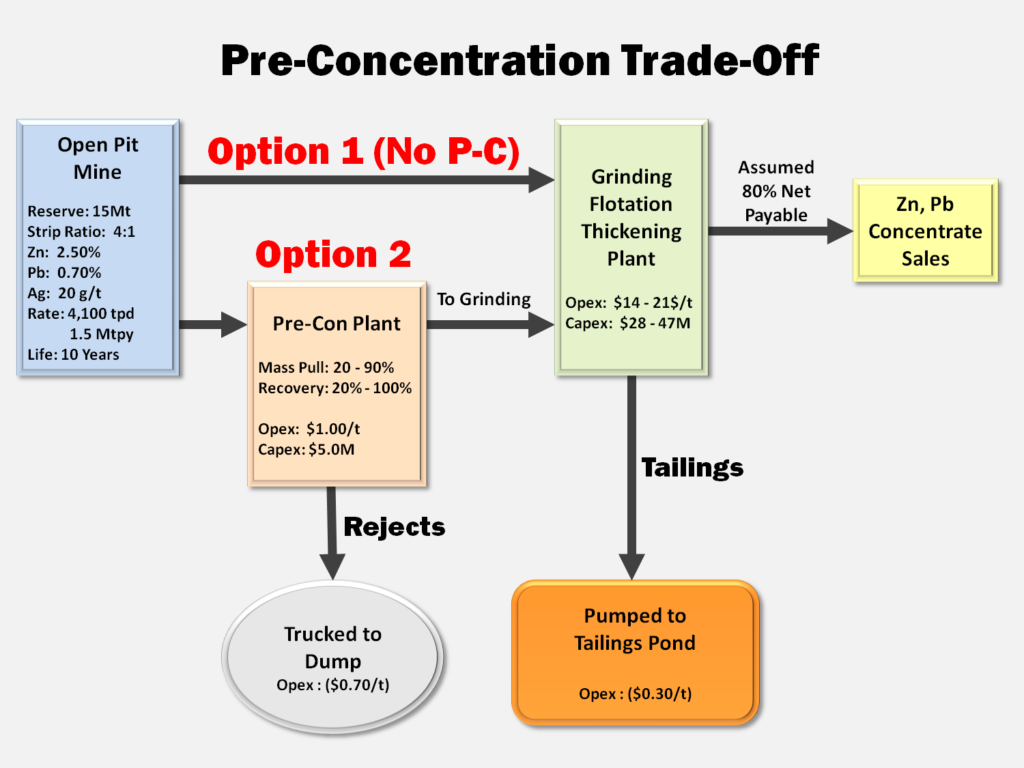

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

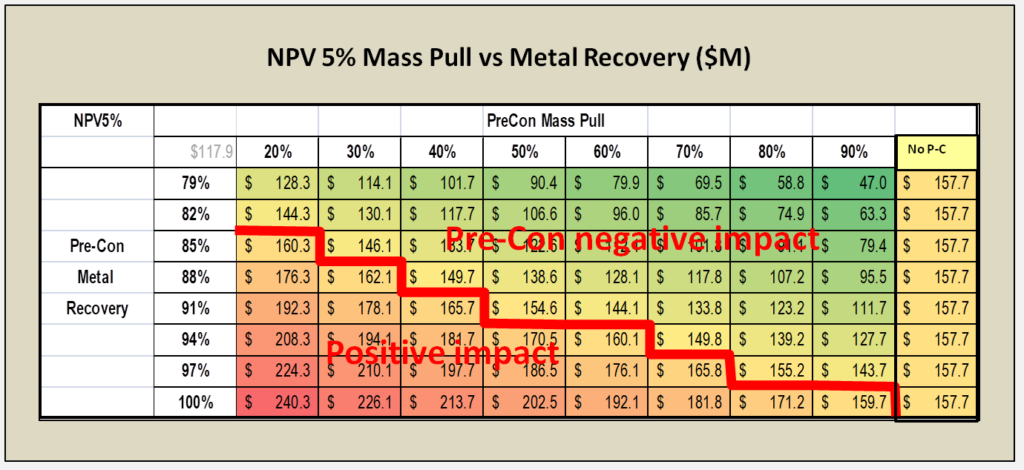

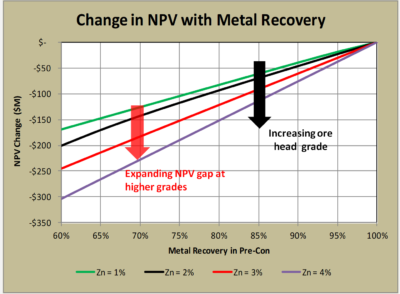

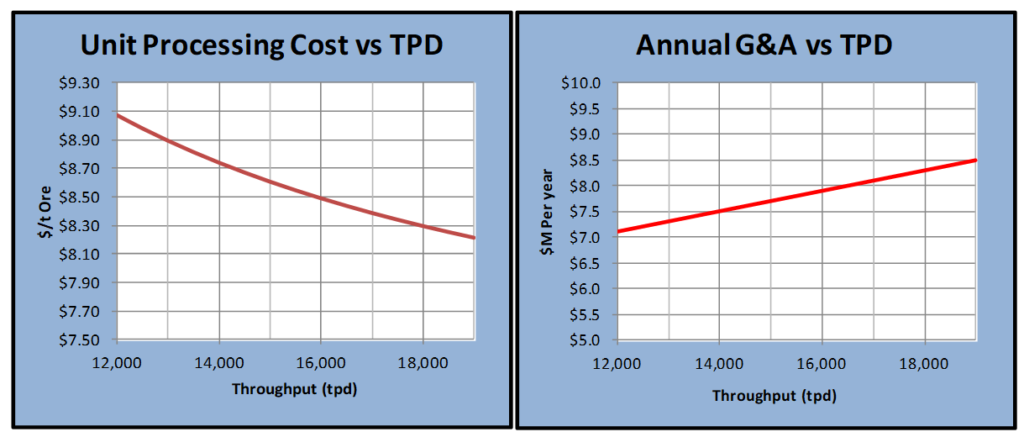

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

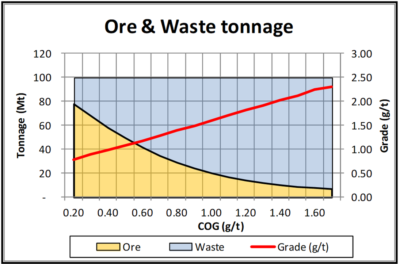

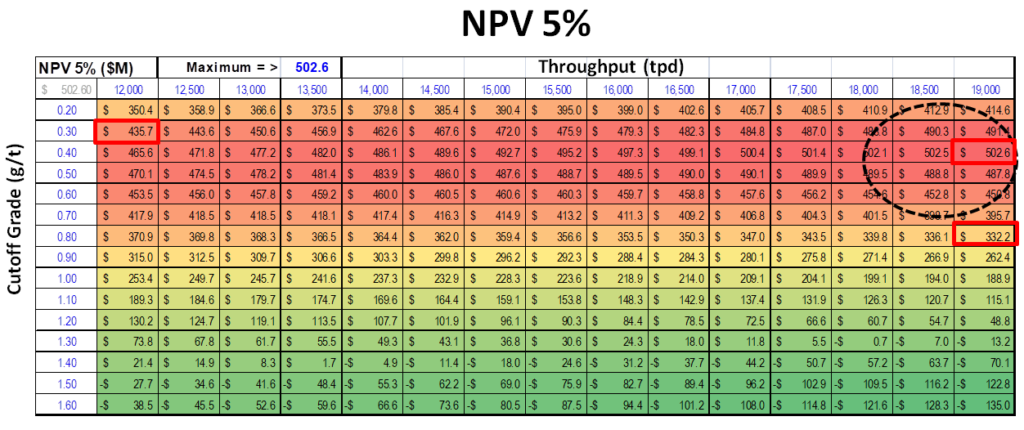

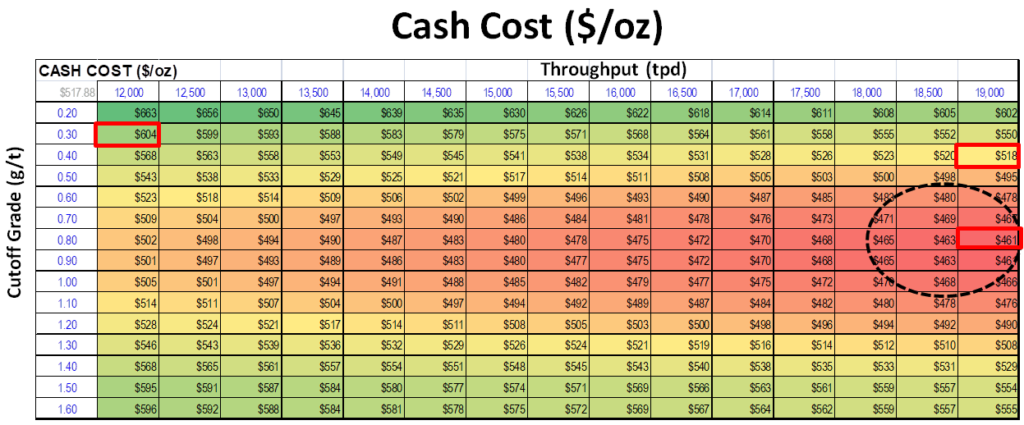

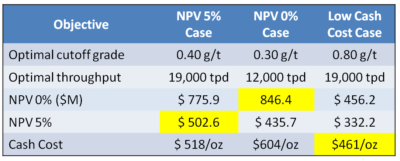

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

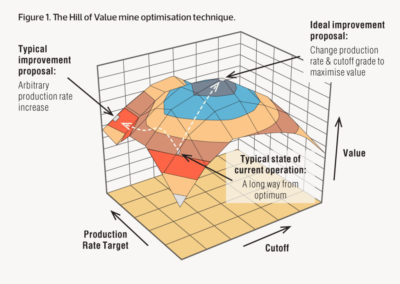

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

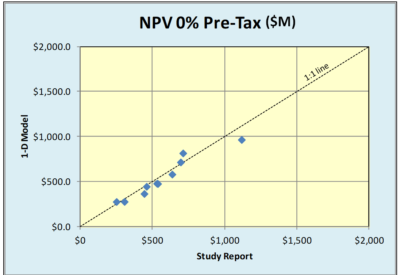

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model.

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model. There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars. Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members.

Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members. Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there.

Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there. As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.