Normally I don’t write about mining stock markets, preferring instead to focus on technical matters. However I have seen some recent discussions on Twitter about stock price trends. For every stock there are a wide range of price expectations. Ultimately some of the expectations and realizations can be linked back to the Lassonde Curve.

Normally I don’t write about mining stock markets, preferring instead to focus on technical matters. However I have seen some recent discussions on Twitter about stock price trends. For every stock there are a wide range of price expectations. Ultimately some of the expectations and realizations can be linked back to the Lassonde Curve.

The Lassonde Curve has been touted by many as a realistic representation of the life stages of a junior mining company. The curve can sometimes be a roller coaster ride for company management.

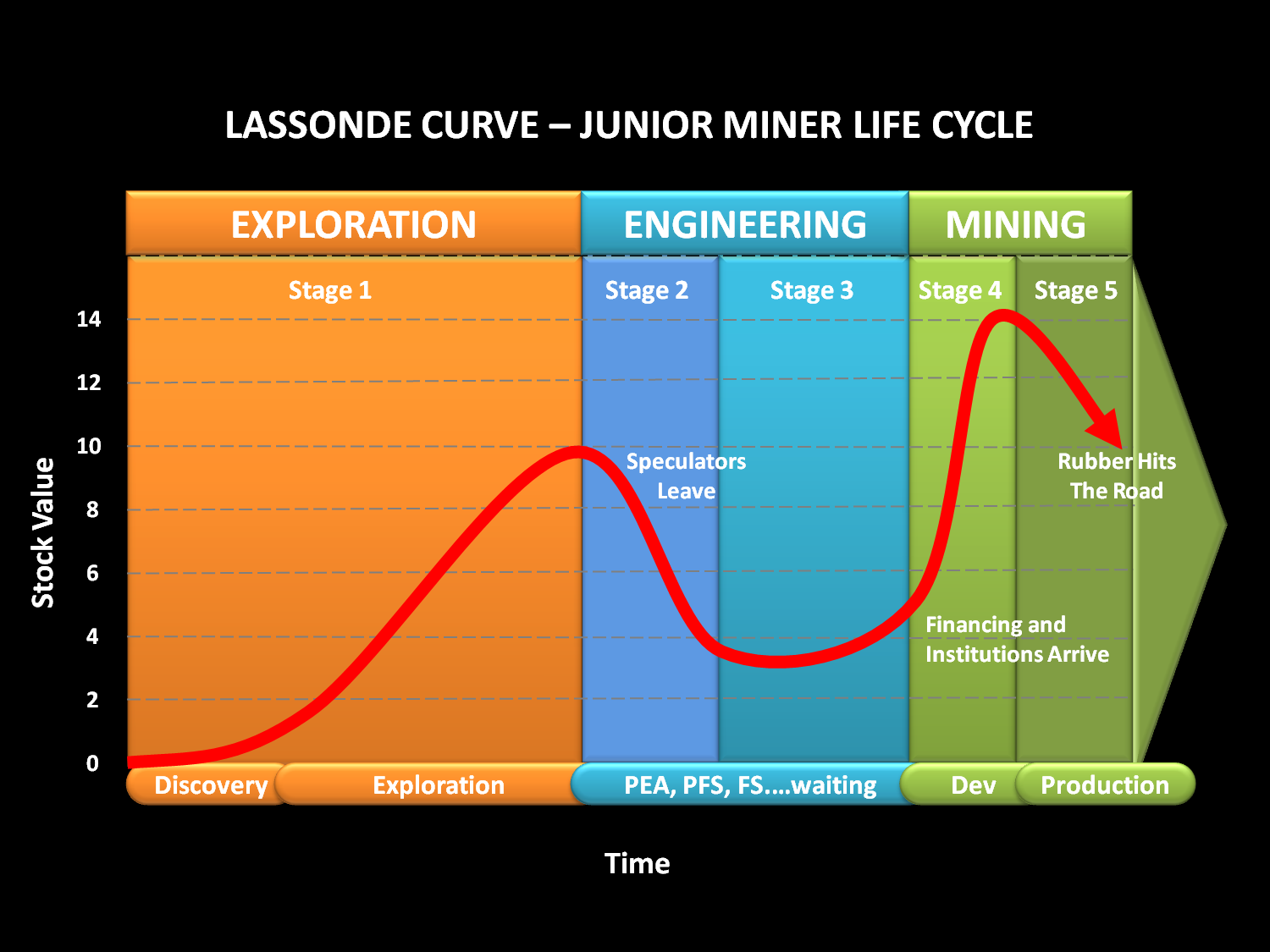

Pierre Lassonde, was one of the founders of Franco-Nevada, the first gold royalty company. Thirty years ago he created his curve, that has now become a foundation in the junior mining business. The Lassonde Curve outlines the company life stages, beginning at exploration and ending at production. It shows the perceived value (i.e. stock value) that investors may assign at each life stage.

The stock price trend illustrated by the curve can, knowingly or unknowingly, impact on a company’s decision making process. So in effect, there are some technical ramifications from it.

People may have differing opinions on what factors are driving the curve. Take a look at it and decide for yourself. Typically people define the curve into four life stages, but I tend to view it in five stages.

Mining Company Stages 1 to 5

Stage 1 Climb

Stage 1 is the earliest stage, consisting of exploration. This period generates rising anticipation from promotion and exciting press releases. The stock value climbs as the perceived value of the insitu geology increases. Great Bear is an example of company currently in Stage 1 (as of June 2020), and appears to be in no hurry to exit from Stage 1.

Stage 2 is when the prospect moves into technical evaluation. In other words, the engineers now climb aboard the ride. This stage encompasses the PEA, PFS, and FS studies. Each of these can take months to complete, meantime new information releases may be lacking.

If the stock value declines, perhaps its because the engineers bring reality into the picture. Investors may see that the project isn’t as easy or great as they anticipated during Stage 1.

Companies can also lose some presence in the market with no new news. Investors may begin looking at other companies that are still in Stage 1 and hence sell their shares.

Some companies may try to shorten Stage 2 and even skip over Stage 3 by going from a PEA directly into Stage 4 construction.

Stage 3 is the period when the studies have largely been completed and a production decision is pending. At this time the company will be seeking strategic partners and project funding. Permitting is also underway. Unfortunately a lack of financing or poor permitting efforts will extend the time in Stage 3, which can extend for decades or even perpetuity. It’s easy to rattle off the names of companies sitting in Stage 3; for example Donlin Creek, Casino, KSM, and Galore Creek. It seems that once locked in a prolonged Stage 3, it can be difficult to get out of it. Company promotion and marketing can be difficult.

Stage 4 begins when the financing is done and construction begins. This is a sign that the project has been figured out, permits approved, and third-party due diligence found no fatal flaws. The stock value may increase on this positive news, especially if construction is on time and on budget. Its even better news if it’s a period of rising commodity prices.

Stage 5 is the start-up and commercial production period, possibly nerve-racking for some investors. This is where the rubber hits the road. The stock price can fall if milled grades, operating costs, or production rates are not as expected.

Stage 5 is the start-up and commercial production period, possibly nerve-racking for some investors. This is where the rubber hits the road. The stock price can fall if milled grades, operating costs, or production rates are not as expected.

Investors may need to decipher press releases to figure out if things are going well or not. Some investors may now bail out at this time to companies in Stage 1 for greater upside (the 10 bagger).

Companies Staying front and center

Companies know that investors can move elsewhere at any time, so they will try to address the Stage 2 and Stage 3 doldrums in different ways. They can:

-

Find new exploration prospects elsewhere while the engineering work is underway.

-

Undertake a series of optimization studies on the same project to keep up the news flow.

-

Continue step out drilling on the same property to expand resources and generate new excitement.

-

Have management appear regularly on podcasts, webinars, conferences, and keep promoting on LinkedIn, Twitter, and with newsletter writers.

Ideally one would like to stagger multiple prospects at different stages of the Curve. While this makes sense, it also takes a fair bit of funding to do it. It also may bring criticism that the company is losing focus on their flagship project. Generally if the stock price is improving, you don’t see this complaint.

Conclusion

Some corporate presentations will highlight the Lassonde Curve, particularly when they are rising in Stage 1. You are less likely to see the curve presented when they are rolling along in Stages 2 or 3.

Some corporate presentations will highlight the Lassonde Curve, particularly when they are rising in Stage 1. You are less likely to see the curve presented when they are rolling along in Stages 2 or 3.

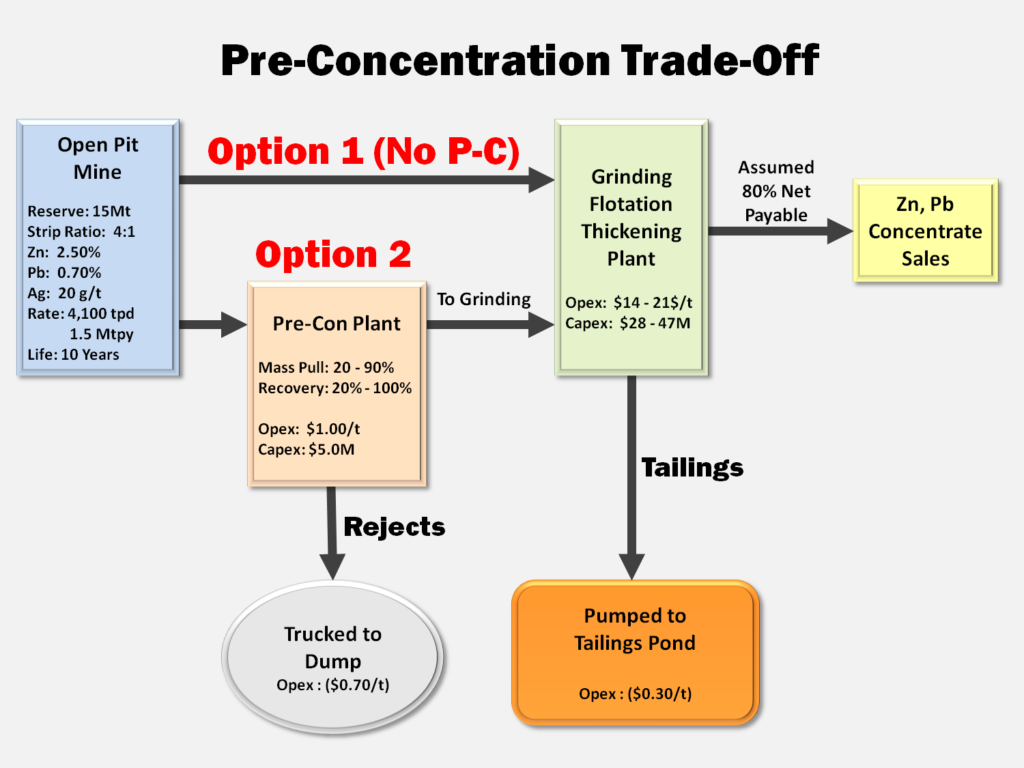

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

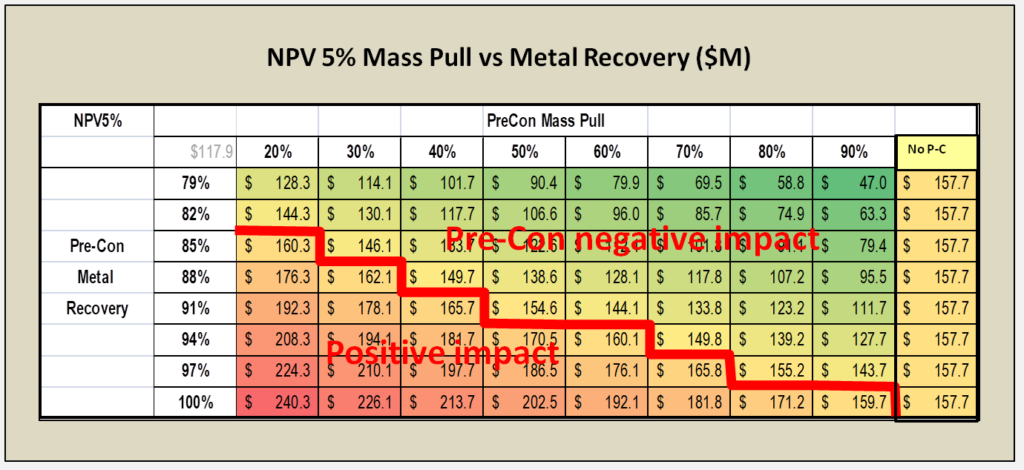

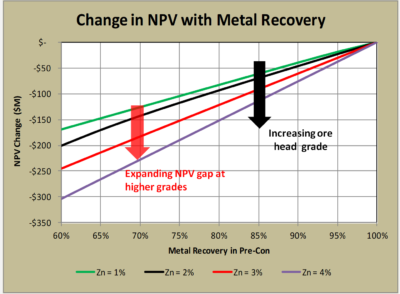

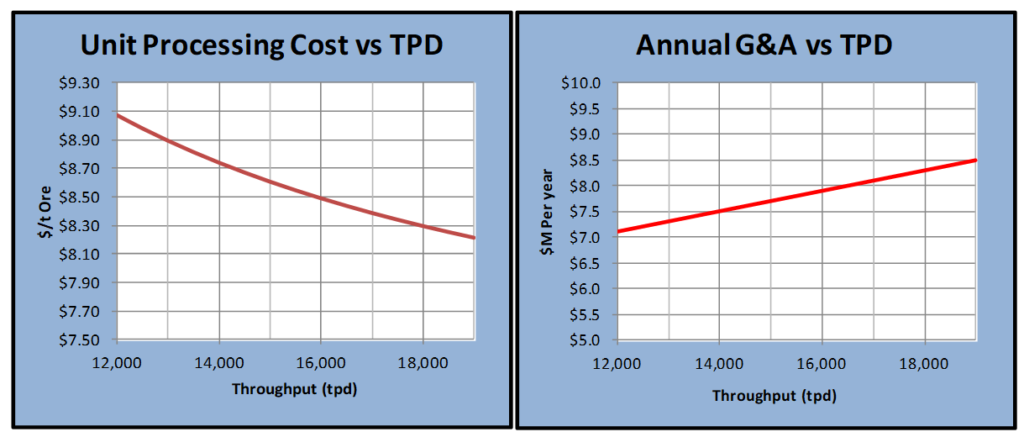

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

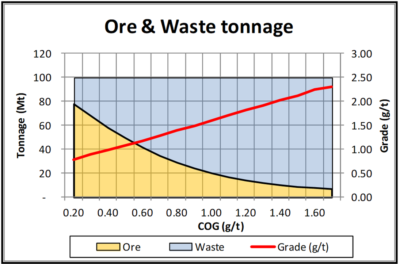

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

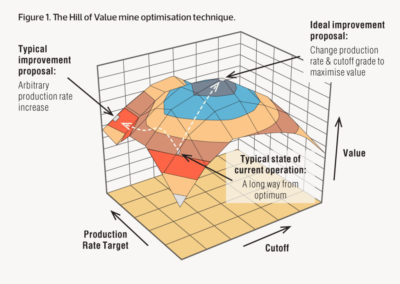

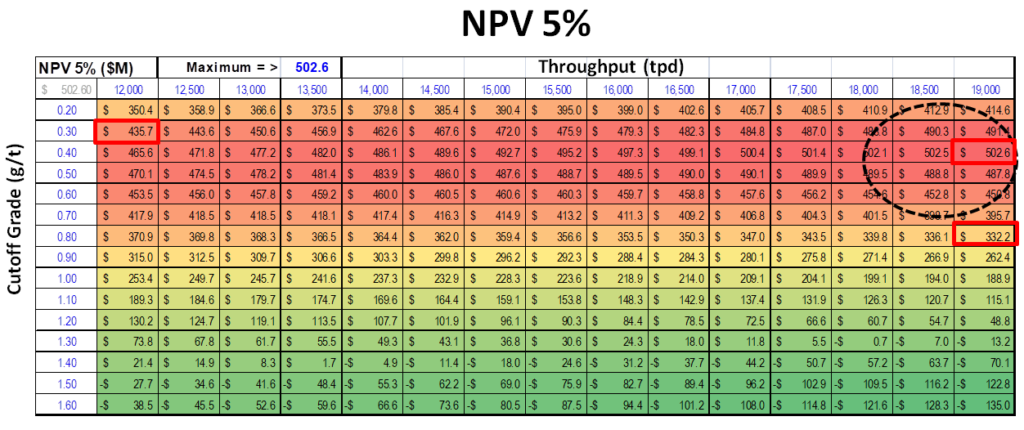

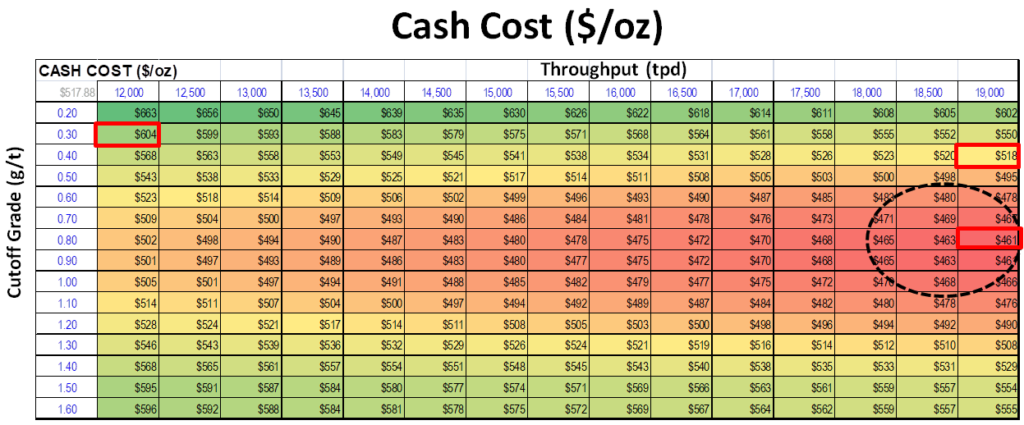

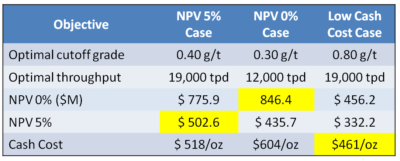

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

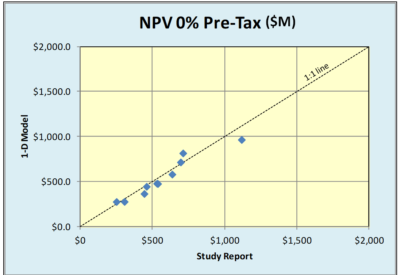

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model.

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model. There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars. Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members.

Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members. Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there.

Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there. As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

The number of independent mining consultants is increasing daily as more people reach retirement age or are made redundant.

The number of independent mining consultants is increasing daily as more people reach retirement age or are made redundant. GLG (

GLG ( Digbee (

Digbee (

We often see junior mining companies benchmarking themselves against others. Sometimes corporate presentations provide graphs of enterprise value per gold ounce to demonstrate that a company might be undervalued.

We often see junior mining companies benchmarking themselves against others. Sometimes corporate presentations provide graphs of enterprise value per gold ounce to demonstrate that a company might be undervalued. Lenders may have observers at site monitoring both construction progress and cash expenditures. Shareholders and analysts are watching for news releases that update the capital spending. Their concern is well founded due to several significant cost over-run instances.

Lenders may have observers at site monitoring both construction progress and cash expenditures. Shareholders and analysts are watching for news releases that update the capital spending. Their concern is well founded due to several significant cost over-run instances. It would be a good thing if the mining industry (or other concerned parties) work together to create open source project databases. These would incorporate summary information and cost information for global mining projects. The information is already out there, it just needs to be compiled.

It would be a good thing if the mining industry (or other concerned parties) work together to create open source project databases. These would incorporate summary information and cost information for global mining projects. The information is already out there, it just needs to be compiled. Benchmarking can be a great tool when done correctly. Benchmarking capital costs might bring more transparency to the project development process. It may help convince nervous investors that the proposed costs are reasonable.

Benchmarking can be a great tool when done correctly. Benchmarking capital costs might bring more transparency to the project development process. It may help convince nervous investors that the proposed costs are reasonable.

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due.

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due. I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play.

I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play. Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now.

Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now. It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

In general to get financing and investor interest, development projects must demonstrate a high NPV, high IRR, and short payback period. This requirement tends to apply more to the small and mid tiered companies than to the major companies. The majors normally have different access to financing.

In general to get financing and investor interest, development projects must demonstrate a high NPV, high IRR, and short payback period. This requirement tends to apply more to the small and mid tiered companies than to the major companies. The majors normally have different access to financing. There are several scenarios where NPV analysis decision making may conflict with the objectives of sustainable mining. Here are a few examples.

There are several scenarios where NPV analysis decision making may conflict with the objectives of sustainable mining. Here are a few examples. 4. Low grade ore stockpiling can help to increase early revenue and profit, thereby improving the project NPV and payback. Stockpiling of low grade and prioritization of high grade means that lower grade ore will be processed in the later stages of the project life. Who hasn’t been happy to develop a mine schedule with the grade profile shown on the right?

4. Low grade ore stockpiling can help to increase early revenue and profit, thereby improving the project NPV and payback. Stockpiling of low grade and prioritization of high grade means that lower grade ore will be processed in the later stages of the project life. Who hasn’t been happy to develop a mine schedule with the grade profile shown on the right? 7. Accelerated depreciation, tax and royalty holidays are types of economic factors that will improve NPV and early payback. They are one tool governments use to promote economic activity. These tax holidays will greatly enhance the NPV when combined with high grading and waste stripping deferral.

7. Accelerated depreciation, tax and royalty holidays are types of economic factors that will improve NPV and early payback. They are one tool governments use to promote economic activity. These tax holidays will greatly enhance the NPV when combined with high grading and waste stripping deferral. NPV is one of the standard metrics used to make project decisions. The deferral of upfront costs in lieu of future costs is favorable for cashflow and investor returns. Similarly, increasing early revenue at the expense of future revenue does the same. Both approaches will help satisfy the financing concerns. However they may not be advantageous for creating long term sustainable projects.

NPV is one of the standard metrics used to make project decisions. The deferral of upfront costs in lieu of future costs is favorable for cashflow and investor returns. Similarly, increasing early revenue at the expense of future revenue does the same. Both approaches will help satisfy the financing concerns. However they may not be advantageous for creating long term sustainable projects.

We hear a lot about the need for the mining industry to adopt sustainable mining practices. Is everyone certain what that actually means? Ask a group of people for their opinions on this and you’ll probably get a range of answers. It appears to me that there are two general perspectives on the issue.

We hear a lot about the need for the mining industry to adopt sustainable mining practices. Is everyone certain what that actually means? Ask a group of people for their opinions on this and you’ll probably get a range of answers. It appears to me that there are two general perspectives on the issue. The solutions proposed to foster sustainable mining depend on which perspective is considered.

The solutions proposed to foster sustainable mining depend on which perspective is considered. There are teams of smart people representing mining companies working with the local communities. These sustainability teams will ultimately be the key players in making or breaking the sustainability of mining industry. They will build and maintain the perception of the industry.

There are teams of smart people representing mining companies working with the local communities. These sustainability teams will ultimately be the key players in making or breaking the sustainability of mining industry. They will build and maintain the perception of the industry.