You read a lot these days about the push for more optimization in mining. Ore grades are declining and high-grade, easy-to-process deposits are becoming scarcer, forcing new projects to face greater risk. To compensate for this, miners are told to optimize and innovate more. They are doing both; including making technological gains.

Mining has gotten better at squeezing more value from each tonne of ore. So why do see mining projects still stumbling and everyone being pushed to do even more optimization?

The answer may be that the industry is confusing optimization with resilience. A mine tuned to perform perfectly under one set of conditions may become fragile when those conditions shift. And in mining, things are always shifting. Maybe the head grades don’t meet expectations or metal prices collapse. Maybe there is a shift in community sentiment or a geotechnical surprise in the mine.

The pursuit of a single “optimal” outcome might leave projects well engineered, yet poorly equipped for reality. Flexibility (or resiliency) aren’t the enemy of efficiency; they may be the only way to make efficiency sustainable.

Which Aspects Should Be Optimized

Is the concept of optimization the most important factor in a project’s design? If so, which aspect is the most important to optimize? A danger is optimizing for a single criteria, for example NPV, at the expense of everything else. Selecting the optimal design for one aspect will likely result in being sub-optimal in some of the others.

Is the concept of optimization the most important factor in a project’s design? If so, which aspect is the most important to optimize? A danger is optimizing for a single criteria, for example NPV, at the expense of everything else. Selecting the optimal design for one aspect will likely result in being sub-optimal in some of the others.

Once one has selected the aspect to optimize, the next issue becomes what to base the optimization on. Optimization typically is founded on a specific set of inputs. When these change, the optimized design will likely require revision. This then forces a new optimization, which can create a never-ending optimization loop because things are always changing in mining.

The design aspects that I have seen recommended for optimization range from:

-

optimize your drill hole locations

-

optimize your pit size

-

optimize your production schedule

-

optimize your throughput and/or recovery

-

optimize your water consumption

-

optimize your carbon footprint

-

optimize your project design

-

optimize your labour productivity

-

optimize either NPV, IRR, or payback

- optimize your metal production cash cost

There are a lot of suggestions and recommendations and people will have differing opinion on which are the most important optimizations. This opinion is typically driven by their own expertise or field of work, not necessarily by what is best for the project.

Optimal vs Resilient Design

Optimization of a mining project can yield meaningful cost and efficiency gains. However mines face inherent constraints, such as ore grade variability, geological surprises, equipment life cycles, and regulatory issues.

Optimization of a mining project can yield meaningful cost and efficiency gains. However mines face inherent constraints, such as ore grade variability, geological surprises, equipment life cycles, and regulatory issues.

Company success is typically driven by a broader set of variables: commodity price cycles, capital availability, asset portfolio quality, ESG and social license, M&A timing, and balance sheet strength. A perfectly optimized mine in a declining commodity or in a politically unstable jurisdiction may underperform a less-optimized mine in the right location at the right time.

Chasing optimization can sometimes lead to over-investment in a single asset, reduced flexibility, or operational fragility. The system performs well only under the ideal conditions.

Hence flexibility is important. If the mine plan is so rigid that it cannot pivot when a new high-grade zone is discovered or a pit wall becomes unstable, then one has optimized for a single scenario rather than for long-term resilience. Rather than designing for the “best case,” design for resilience.

Flexibility builds in the ability to scale production up or down, switch mining sequences, or pivot processing approaches as conditions change. Resilience has real value in mining, where geology, markets, and costs are unpredictable.

Flexibility identifies and can mitigate technical, geopolitical, regulatory, environmental, and market risks. The mines that do run into trouble rarely do so because they weren’t optimized; they fail because key risks weren’t anticipated or managed.

Workforce capability, safety culture, and leadership quality are key predictors of operational success. Optimization alone may not be able to address high turnover, poor safety records, and weak supervisory capacity. These can erode profitability far more than sub-optimal scheduling.

In my experience, the best operations have systems for ongoing learning and improvement rather than seeking a one-time optimal design. However, there is still a place for full optimization in some situations.

When does a flexible project design win?

-

Commodity prices are volatile up and down

-

Geological uncertainty is high (low proportion of Measured Resource)

-

Mining uncertainty (limited geotechnical investigations)

-

Long mine life (10–30+ years), where conditions will certainly change

-

Regulatory or social environments are unpredictable

-

Capital markets may require staged investment rather than full financing

When does an optimal project design win?

-

Shorter mine life where conditions are unlikely to change materially

-

Commodity is stable, well-hedged, or under long term offtake contract pricing

-

Geology and processability is well-understood (mature, well drilled-out deposit)

-

Capital is constrained and upfront efficiency is critical (you need to get it right)

Unfortunately some might view flexibility as a weakness. If a company has to change a plan or pivot, some will view that as a sign that the company is poor at planning and they don’t know what they are doing. In some cases, this might be true. Conversely the company may simply be reacting to unforeseeable outside influences.

The Path to Resiliency

If one decides to pursue the path of operational flexibility, what are the things that help make it happen?

If one decides to pursue the path of operational flexibility, what are the things that help make it happen?

-

Design for flexibility at the start: Build project components that can scale up or down as needed. This might include wider pit ramps, larger infrastructure, some modularization in the processing system and the mine. Building a single rigid optimal design can be a trap. Open pit mines may be inherently more flexible than underground mines.

-

Maintain multiple ore sources: Maintain flexibility across different mining areas and ore zones with different metallurgy or head grades means one can blend ore as needed. Multiple mining areas provide flexibility in the case of geotechnical or weather events. Multiple stockpiling is also part of flexibility in design and operation.

-

Be careful consuming all high grade ore: In order to boost NPV, often most of the high grade ore is consumed early in the schedule, meaning the back part of the schedule relies on low grade material. This reduces economic flexibility if prices decrease in the future and may also miss out on the benefits if prices rise.

-

Real-time data collection and adaptive planning: Real time control systems let operations respond to actual conditions rather than following a fixed weekly plan. The idea is to shorten the time between observation and reaction, not to automate rigidly but enable the system to adapt rapidly.

-

Keep a cross-trained workforce: Operational flexibility may be enhanced if people can fill multiple roles. Cross-training operators means one can redeploy people as needed when conditions change.

-

Maintain financial health: A company with low debt, high cash assets, and easy credit access can keep a mine on basic functionality (or care-and-maintenance) rather than being forced to sell assets or close the doors during a downturn. Financial health will help ensure operational flexibility. The major miners already know this. The junior miners learn it the hard way.

-

Build supplier and contractor relationships before needed: Much like access to credit, long-term supplier arrangements might mean one can find labor and materials faster than competitors scrambling during downturns or upturns.

-

Scenario-plan continuously: Run multiple what-if commodity price, head grade, geotechnical & water management scenarios regularly during operations, not just at the feasibility or permitting stage. Operations change over time, and teams that have already pre-planned “what if this happens” respond better when it really happens.

Flexible mining operations may sacrifice a little efficiency at peak conditions and not meet the fully optimized vision. However this flexibility is a trade-off for the ability to stay profitable over a range of scenarios.

Conclusion

Rather than focus on constant optimization in design, it may be wiser to focus on a flexible design. Adaptability, flexibility, and resilience may be more important than being fully optimized.

Rather than focus on constant optimization in design, it may be wiser to focus on a flexible design. Adaptability, flexibility, and resilience may be more important than being fully optimized.

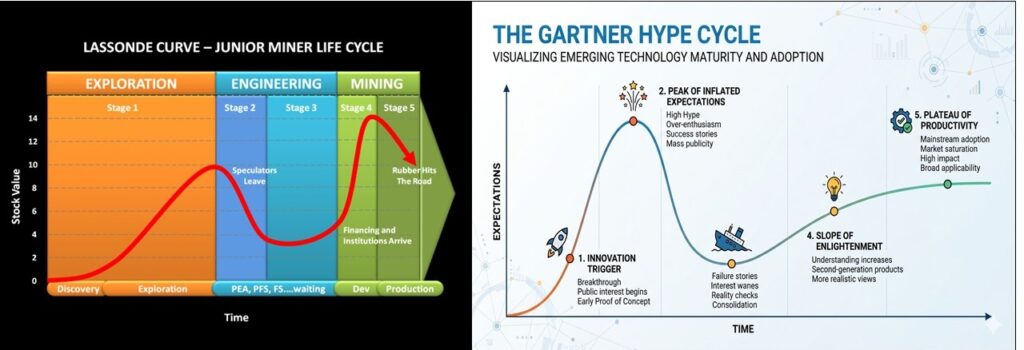

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems.

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems. Exploration spending shares some of the same characteristics of more commonly R&D.

Exploration spending shares some of the same characteristics of more commonly R&D.

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

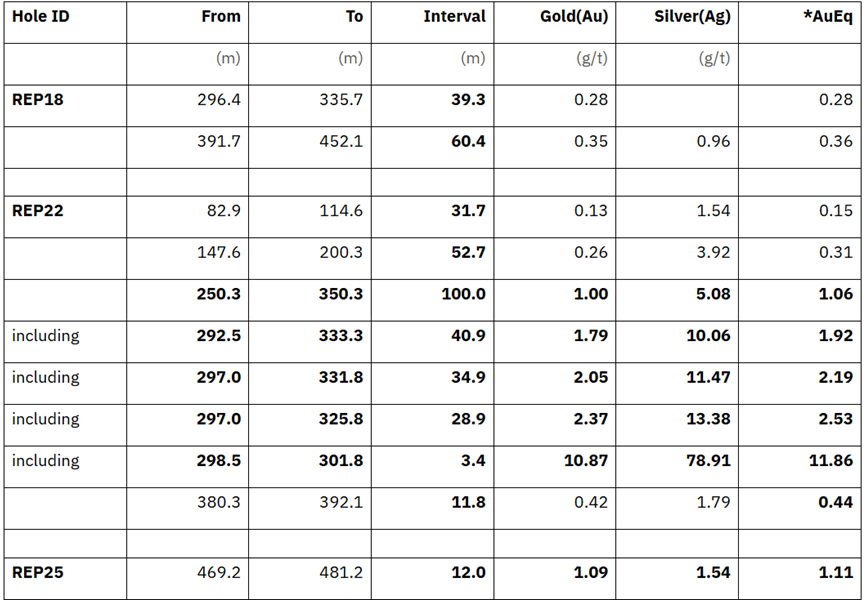

Recently I have been reviewing a few mining projects from an investor’s perspective. This led me to wonder whether junior mining companies should share more than just their drill hole highlights. What about the raw assays? A mining company announces highlighted drill intervals, but what exactly do those numbers represent?

Recently I have been reviewing a few mining projects from an investor’s perspective. This led me to wonder whether junior mining companies should share more than just their drill hole highlights. What about the raw assays? A mining company announces highlighted drill intervals, but what exactly do those numbers represent? There is a sense that many mining investors are becoming more sophisticated, and they want to fully understand the exploration process.

There is a sense that many mining investors are becoming more sophisticated, and they want to fully understand the exploration process.

1. Misinterpretation & “Amateur” Experts: One risk is that someone with a very basic understanding of mining software and limited understanding of the local geology, runs flawed interpretations and publicizes their incorrect conclusions. A company may find that correcting false narratives publicly can be harder than preventing them.

1. Misinterpretation & “Amateur” Experts: One risk is that someone with a very basic understanding of mining software and limited understanding of the local geology, runs flawed interpretations and publicizes their incorrect conclusions. A company may find that correcting false narratives publicly can be harder than preventing them. Once the assay data is public, it may be more difficult for a company to manage the story. A press release lets them frame results in the context of their business plan; a raw data file does not.

Once the assay data is public, it may be more difficult for a company to manage the story. A press release lets them frame results in the context of their business plan; a raw data file does not. For investors trying to assess a junior explorer, or geologists conducting a technical review, or a regulator trying to ensure fair and accurate disclosure, access to raw assay data can play a part in promoting good judgment and accurate disclosure from companies.

For investors trying to assess a junior explorer, or geologists conducting a technical review, or a regulator trying to ensure fair and accurate disclosure, access to raw assay data can play a part in promoting good judgment and accurate disclosure from companies.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening. USER PROMPT: What are the risks of toll milling plan.

USER PROMPT: What are the risks of toll milling plan. RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia.

RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia. The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

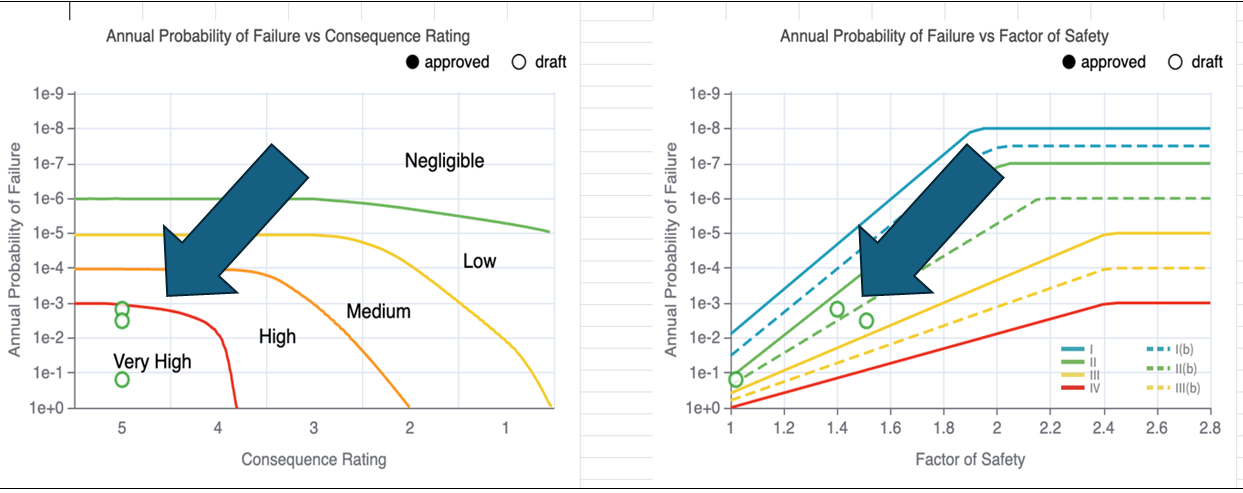

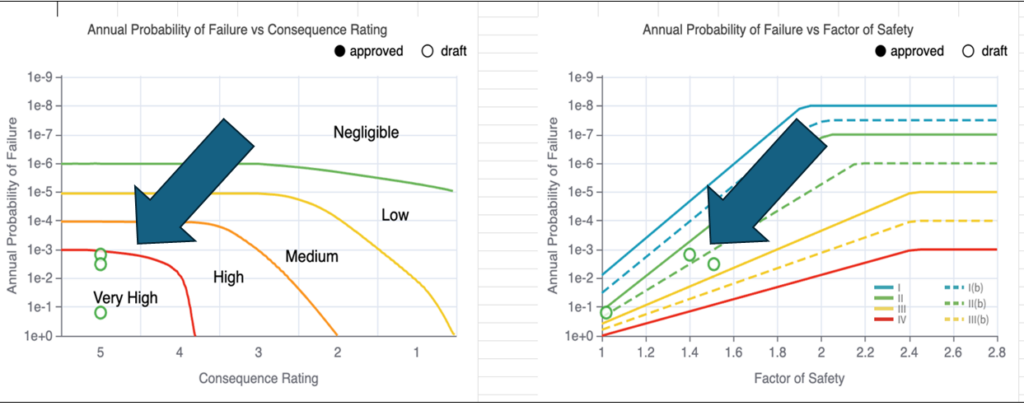

In my view, having a single industry platform for critical infrastructure risk management provides several benefits. These are:

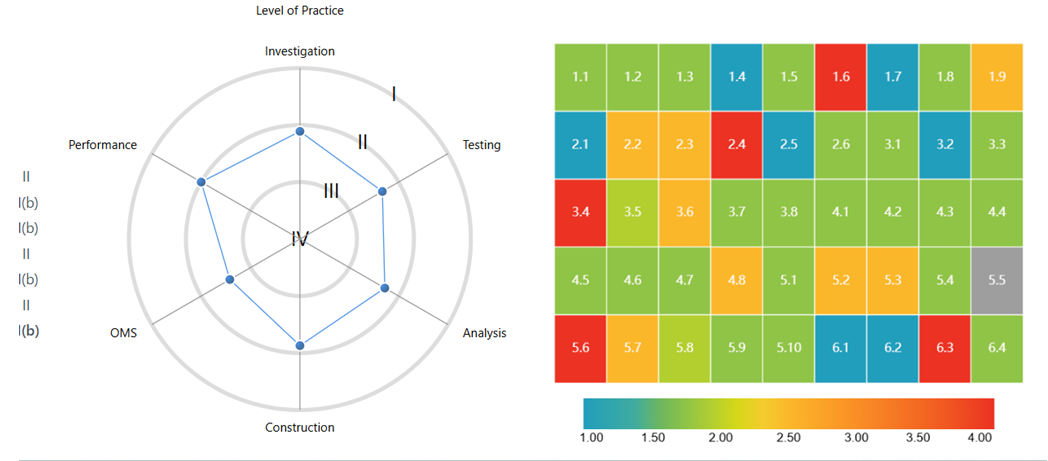

In my view, having a single industry platform for critical infrastructure risk management provides several benefits. These are: Each mine site is unique with its own set of “Facilities”. For example, the individual Facilities could include Tailing Management Area #1, TMA #2, the Heap Leach Pad, Waste Dump #1, Waste Dump #2, etc.

Each mine site is unique with its own set of “Facilities”. For example, the individual Facilities could include Tailing Management Area #1, TMA #2, the Heap Leach Pad, Waste Dump #1, Waste Dump #2, etc. The Level of Practice (LOP) is a measure of the integrity and quality of data used to design and manage a mine facility. The CI-RiskDB platform currently uses 45 criteria to evaluate the LOP associated with a facility. For example, these quality criteria include items such as: current understanding of soil profile; testing & verification between lab and field investigations; stability analysis detail; construction QA/QC undertaken, monitoring programs, etc.

The Level of Practice (LOP) is a measure of the integrity and quality of data used to design and manage a mine facility. The CI-RiskDB platform currently uses 45 criteria to evaluate the LOP associated with a facility. For example, these quality criteria include items such as: current understanding of soil profile; testing & verification between lab and field investigations; stability analysis detail; construction QA/QC undertaken, monitoring programs, etc.

Over confidence of personnel is something that can unfortunately play a role in risk management. However, the more eyes involved with reviews and signoffs, as well as occasional third party audits, the less likely that this occurs (hopefully).

Over confidence of personnel is something that can unfortunately play a role in risk management. However, the more eyes involved with reviews and signoffs, as well as occasional third party audits, the less likely that this occurs (hopefully). In closing, as of this month December 2025, I understand the Critical Infrastructure Risk Decision Basis platform is currently being piloted and implemented at a number of mine sites in Canada, including Agnico Eagle at a corporate level. Additional pilots may be forthcoming in 2026.

In closing, as of this month December 2025, I understand the Critical Infrastructure Risk Decision Basis platform is currently being piloted and implemented at a number of mine sites in Canada, including Agnico Eagle at a corporate level. Additional pilots may be forthcoming in 2026.

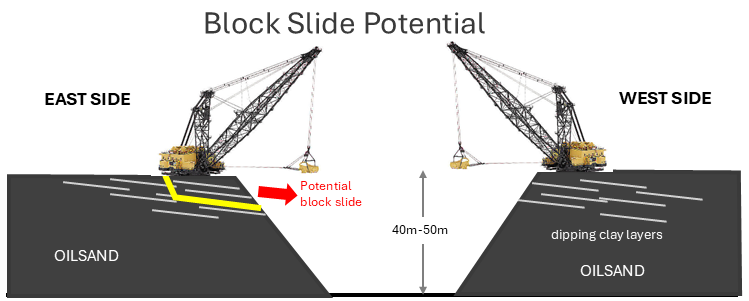

Syncrude had four large walking draglines, each with a 80 cubic metre bucket and 110 metre operating radius. These were very big machines; you could sit one in the end zone of a football field and the bucket would be digging (or dumping) in the other end zone. Two draglines were on the East side of the mine and two were on the West, mining the oilsand in 25 m wide strips.

Syncrude had four large walking draglines, each with a 80 cubic metre bucket and 110 metre operating radius. These were very big machines; you could sit one in the end zone of a football field and the bucket would be digging (or dumping) in the other end zone. Two draglines were on the East side of the mine and two were on the West, mining the oilsand in 25 m wide strips. There were numerous instances of East mine block slides, where large portions of the upper slope would fail as large blocks, 50 metres long and up to 30 metres back from the crest. The fear was that if a dragline happened to be sitting on one of these failing blocks, the entire machine would slide along into the pit. Many block slides did occur over the years, but only a few came close to jeopardizing a machine. The geotechnical monitoring programs in place were successful (described later).

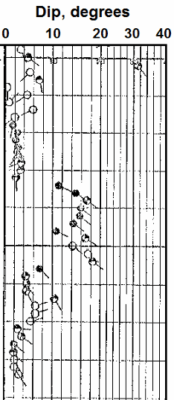

There were numerous instances of East mine block slides, where large portions of the upper slope would fail as large blocks, 50 metres long and up to 30 metres back from the crest. The fear was that if a dragline happened to be sitting on one of these failing blocks, the entire machine would slide along into the pit. Many block slides did occur over the years, but only a few came close to jeopardizing a machine. The geotechnical monitoring programs in place were successful (described later). The insitu clay structures were identified using oil and gas borehole logging technology, with tadpole dipmeter plots (see image) used to analyse the bedding (the tail on the tadpole shows the dip direction). The vertical axis is depth from surface or elevation. The geotech engineers would use this information, combined with structural mapping of previously mined faces, to forecast potentially unstable areas.

The insitu clay structures were identified using oil and gas borehole logging technology, with tadpole dipmeter plots (see image) used to analyse the bedding (the tail on the tadpole shows the dip direction). The vertical axis is depth from surface or elevation. The geotech engineers would use this information, combined with structural mapping of previously mined faces, to forecast potentially unstable areas. The main geotechnical issue on the West side were basal slope failures, termed this due to sliding along weak clays and muds at the base of the highwall. This photo shows a typical basal failure. Basal failures also occured on the East side.

The main geotechnical issue on the West side were basal slope failures, termed this due to sliding along weak clays and muds at the base of the highwall. This photo shows a typical basal failure. Basal failures also occured on the East side. Once our engineer-in-training rotation program was complete, we were to be assigned to a more permanent position. For me, that was going to be as an East side geotechnical engineer – ugh!. It’s at that time I decided to look for greener pastures. Three years was long enough from 1980 to 1983; given the amount of learning and responsibility I had undertaken. Other colleagues left the same time, while many other friends stayed in Ft McMurray for their entire careers.

Once our engineer-in-training rotation program was complete, we were to be assigned to a more permanent position. For me, that was going to be as an East side geotechnical engineer – ugh!. It’s at that time I decided to look for greener pastures. Three years was long enough from 1980 to 1983; given the amount of learning and responsibility I had undertaken. Other colleagues left the same time, while many other friends stayed in Ft McMurray for their entire careers.

In Part 1 of this two part blog post I would like to share some stories from the early days of my career working in Fort McMurray.

In Part 1 of this two part blog post I would like to share some stories from the early days of my career working in Fort McMurray. At the time Syncrude had an excellent engineer-in-training program for new graduates. Every six months they would rotate engineers into different technical areas.

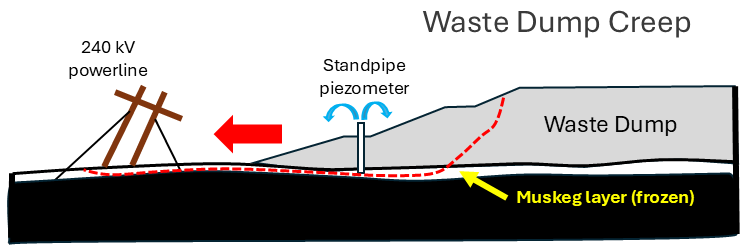

At the time Syncrude had an excellent engineer-in-training program for new graduates. Every six months they would rotate engineers into different technical areas. Next we sampled that depth carefully, revealing that frozen muskeg layers were present. When we installed standpipe piezometers in these holes, we saw water flowing out of the top of the pipes. This means the foundation pore pressure is high, way too high.

Next we sampled that depth carefully, revealing that frozen muskeg layers were present. When we installed standpipe piezometers in these holes, we saw water flowing out of the top of the pipes. This means the foundation pore pressure is high, way too high. For example, one project I had was to monitor the performance of different brands and styles of conveyor idlers. We would track about 2,000 individual idlers; when they were installed on the conveyors; when they were removed, why they were removed (bearing failure, cover failure, something else).

For example, one project I had was to monitor the performance of different brands and styles of conveyor idlers. We would track about 2,000 individual idlers; when they were installed on the conveyors; when they were removed, why they were removed (bearing failure, cover failure, something else).

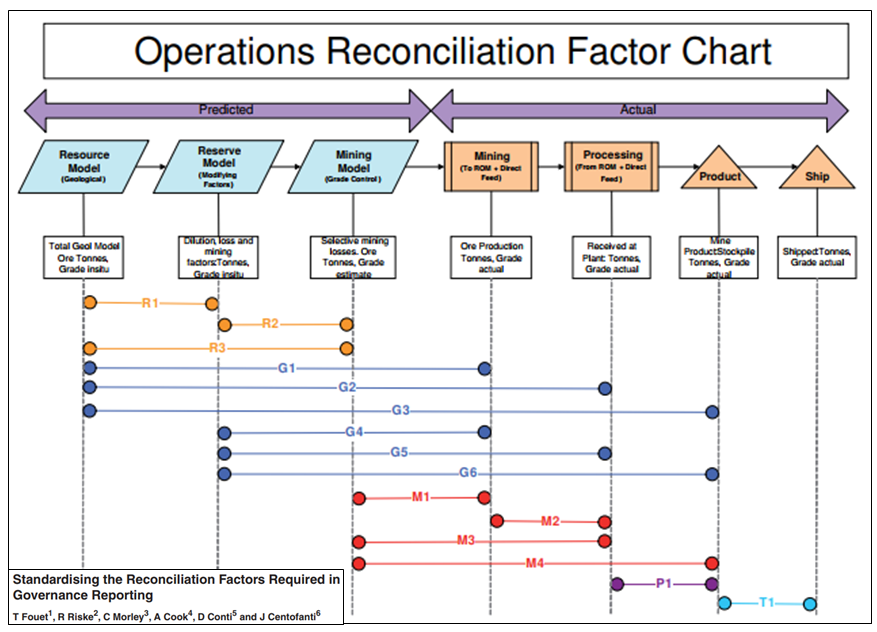

The mining industry is implementing more and more technology in the mining cycle.

The mining industry is implementing more and more technology in the mining cycle. Mine reconciliation requires information such as initial predictions from exploration data and geological models, actual measurement: data from mining sources, such as blast holes, stockpile samples, or mill feed. As well it will need data on the final product being shipped off site. Do the metal quantities balance out throughout the mining operation?

Mine reconciliation requires information such as initial predictions from exploration data and geological models, actual measurement: data from mining sources, such as blast holes, stockpile samples, or mill feed. As well it will need data on the final product being shipped off site. Do the metal quantities balance out throughout the mining operation?

Each mine site may be unique with respect to; ore sources; terminology; ore types; mining methods; stockpiling philosophy; processing methods; technology availability; and personnel capability. So often the easiest approach for mine reconciliation is based on the Excel spreadsheet. (Reconciliation is generally not an easy undertaking).

Each mine site may be unique with respect to; ore sources; terminology; ore types; mining methods; stockpiling philosophy; processing methods; technology availability; and personnel capability. So often the easiest approach for mine reconciliation is based on the Excel spreadsheet. (Reconciliation is generally not an easy undertaking).

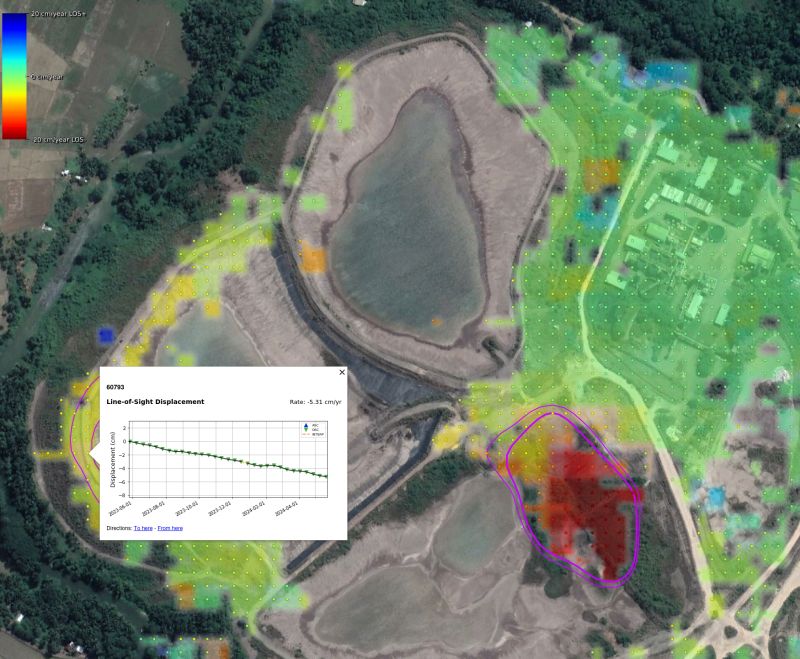

An example of a satellite being used is the Sentinel-1, launched in mid-2015 by the European Space Agency. This satellite information is open-source data. It will have a 6 to 12 day revisit cycle in many locations.

An example of a satellite being used is the Sentinel-1, launched in mid-2015 by the European Space Agency. This satellite information is open-source data. It will have a 6 to 12 day revisit cycle in many locations. On LinkedIn, one can see numerous posts where independent experts are examining historical InSAR data for recent failures to see whether early movement should have been detected. The results seem to be quite positive in that areas that have failed might have been red-flagged prior to failure.

On LinkedIn, one can see numerous posts where independent experts are examining historical InSAR data for recent failures to see whether early movement should have been detected. The results seem to be quite positive in that areas that have failed might have been red-flagged prior to failure. A mining site consists of numerous constructed embankments and slopes of all types and heights. Many of these slopes may be creeping and moving all the time – it’s a living beast.

A mining site consists of numerous constructed embankments and slopes of all types and heights. Many of these slopes may be creeping and moving all the time – it’s a living beast.

Recently I have been seeing more mining studies proposing to use the dry stack approach. In some cases, they no longer even do the typical tailings trade-off study that look at different options. The decision is made upfront that dry stack is the preferred route due to its environmental acceptability and positive perceptions.

Recently I have been seeing more mining studies proposing to use the dry stack approach. In some cases, they no longer even do the typical tailings trade-off study that look at different options. The decision is made upfront that dry stack is the preferred route due to its environmental acceptability and positive perceptions. The Guide covers several topics, including tailings characterization; site closure concepts; filtered tailings stack design; material transport, stacking systems; and tailings dewatering methods. The Guide covers all the basics very well. The one area that jumped out at me is the tailings characterization and testing aspect.

The Guide covers several topics, including tailings characterization; site closure concepts; filtered tailings stack design; material transport, stacking systems; and tailings dewatering methods. The Guide covers all the basics very well. The one area that jumped out at me is the tailings characterization and testing aspect. Major miners, such as BHP and Rio Tinto, typically spare no expense on material testing for metallurgical or geotechnical purposes. They have the funds available to test and engineer to a high level to adequately de-risk the project to meet their investment thresholds.

Major miners, such as BHP and Rio Tinto, typically spare no expense on material testing for metallurgical or geotechnical purposes. They have the funds available to test and engineer to a high level to adequately de-risk the project to meet their investment thresholds.