Recently I’ve seen a few LinkedIn conversations about whether the mining industry is spending enough money on Research and Development (R&D). Usually when one thinks of R&D, one might envision the development of new technology, new drug, equipment or software.

I would suggest that mineral exploration should be viewed through the R&D lens. Exploration (or acquisition of explorers) is the most significant way that the industry can self-manage to grow revenues. If exploration is R&D, that then leads to the observation that Junior Miners are the precursors for today’s Silicon Valley startups.

Before venture capital and “startup culture” became a phenomenon, junior mining companies were already operating on the startup core principles. Small, capital driven explorcos were based on unproven assets, led by specialized technical teams. They were funded by investors accepting risk in the hopes for 10 bagger or 100 bagger upsides. This is effectively the same business model that Silicon Valley would build upon.

This blog post examines whether the junior mining industry was a leader in Tech Startup culture. Even things like the Lassonde Curve and the PEA have their comparables in the current tech world.

Are Junior Miners precursors to Tech Startups

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems.

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems.

Junior mining companies and Tech Startups are both high-risk, high-reward ventures. Junior Miners and Tech Startups are early-stage companies where the vast majority fail. Investors accept enormous risk in exchange for the possibility of enormous returns if a discovery or product is a resounding success. Lets look at some of the similarities.

-

A startup spends years (and millions of dollars) building an MVP (Minimum Viable Product). If the market doesn’t want it or the tech fails to scale, the company goes to zero. Similarly if holes don’t hit or the metallurgy is too complex, the mining asset can face significant headwinds.

-

Both mining and tech are essentially “concept” or “pre-revenue” gambles. A Junior Miner typically has no producing mine, just exploration assets and the dream of an economic mineral deposit. Similarly, many Tech Startups have no revenue, just a product idea or some early traction. Investors in both cases are betting on the team and its future value, not on the non-existing cash flow.

-

Both burn through cash (lots of it) before generating revenue. Mining juniors need constant financing rounds (placements) to fund exploration; startups need financing rounds for R&D and growth. Neither can easily self-fund, although bootstrapping is more common in tech than in mining. Both may rely on exit strategies consisting of acquisition from larger industry players.

-

Both generate proprietary data. A Junior Miner’s most valuable asset is often its geological data (drill results, resource estimates, land tenure). A Tech Startup’s asset is its IP, code, or trade secrets. In both cases, the assets are largely intangible until proven economic.

-

Both rely on quality founders and management. A small, skilled team can make or break the company. A geologist or executive with a great track record (“the Midas touch”) is analogous to a serial tech founder. Often the investors are backing the person more than the project.

-

Both sectors are heavily sentiment-driven (mining likes 2025, tech not so much). A hot commodity cycle floods junior mining with capital. A hot tech cycle (AI, crypto, SaaS) floods startups. When investor sentiment reverses, funding dries up fast and many companies are left to die, possibly to rise again in the next cycle.

-

Both sectors can follow the “Lassonde Curve” (mining) or the “Hype Cycle” (tech). There is an initial surge of excitement during discovery/launch, followed by a “boring” period of technical de-risking (development/user acquisition), and finally a re-rating once they reach production or profitability. (More on the Lassonde Curve later in this blog post).

-

Both sectors require pitching their story to investors. The Tech Startups rely on pitching to angel investor via shows like Shark Tank, pitch summits (t) using 5 minute elevator pitches (“get to the point” pitches). The Junior Miners rely on the numerous mining conferences like PDAC, Mines & Money, Beaver Creek, Zurich, again relying on the PowerPoint pitch to gather eyeballs.

Obviously we should also point out there some differences between juniors and Tech Startups.

-

Juniors work with physical geological reality. You either find the ore body or you don’t. Startups can pivot; geology can’t.

-

Mining has far longer timelines; discovery to production can take 10–20 years vs. a startup’s typical 5–7 year VC cycle. Any longer than that, and a Tech Startups technology can become obsolete.

-

Regulatory, environmental permitting, and social license is a constraint for miners with no real startup equivalent. Viable exploration projects can get blocked through no fault of the miner itself.

-

Junior Miners are more commodity-price dependent. Even a great deposit can be uneconomic at the wrong metal price. Conversely a miner’s asset could become more valuable over time based on metal prices. Tech startup do not rely on a commodity price outside their control.

-

Junior Miners tend to rely on public capital markets for financing right from the start, although the trend toward private equity mining investment may be increasing. Conversely, at early stages, Tech Startups tend to be bootstrapped and financed via private equity, venture capital, and angel investors. Junior Miner investments can provide more liquidity and exit opportunities due to their public listing. Tech investors may be locked in until a liquidity event occurs.

-

The startup world will label their financing rounds (seed, Series A, Series B,..) with the hope that future investors provide financing at higher valuations than earlier investors. The mining industry does not label their placement rounds – perhaps they should.

In conclusion, an analogy between Junior Miners and Tech Startups can help outsiders understand the risk, capital structure, and investor behavior of both industries. One might conclude that Junior Miners were the Tech Startups of decades prior, and are still functioning that way today.

Should exploration expenses be considered R&D

Exploration spending shares some of the same characteristics of more commonly R&D.

Exploration spending shares some of the same characteristics of more commonly R&D.

R&D is uncertain in outcome, generates intellectual property (geological data, resource models), and is expensed before any revenue is realized. A pharma company doesn’t know if a new drug will be a win, similarly a Junior Miner doesn’t know if a drill program will yield an economic deposit. Both activities are investments in discovering something of future value, hopefully.

R&D is about de-risking a concept, and de-risking is a term commonly used by Junior Miners. Every drill hole, soil sample, and geophysical survey is a data point that builds knowledge, and even uneconomic drill holes provide value by focusing the search area.

Much like our drug development example, exploration has a high-failure, high-reward path. Early-stage “lab work” (geochemistry/geophysics) leads to “clinical trials” (core drilling) and eventually “commercialization” (feasibility and production).

There are also some differences between exploration and conventional R&D. R&D will typically create proprietary intellectual property, like a new drug or software platform that can be replicated and marketed globally. A mineral discovery is a unique, non-replicable physical asset in a given location. R&D in tech is about creating something from nothing (innovation), while exploration is about finding something that already exists (discovery).

Exploration also tends to be more binary since it is geologically constrained. You either find an ore body or you don’t. You can’t modify or pivot with an orebody. On the other hand, drug and software R&D can yield partial successes or new technologies, that may have other applications.

Although there are both similarities and differences, the analogy is interesting. Exploration may be considered as a hybrid since it has the uncertainty and knowledge-creation aspect of R&D, but the result is a unique physical asset and not IP. In my view exploration is equivalent to R&D.

Lassonde Curve vs Hype Cycle Curve

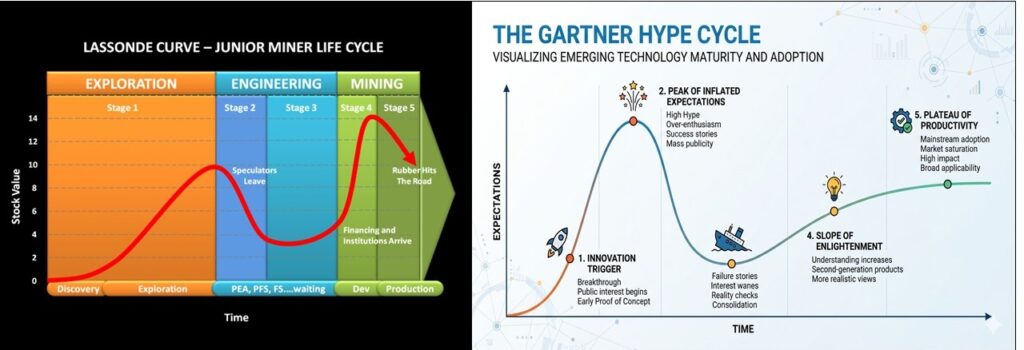

As mentioned previously, junior mining and Tech Startups will follow a cyclic path of hype and despair. In mining it is known as the “Lassonde Curve” and in tech its called the “Gartner Hype Cycle”. Let’s look at the similarities. Which came first?

The Lassonde Curve is the “elder” of the two models, predating the Gartner Hype Cycle by about a decade. I had written a previous blog post on this at Mining’s Lassonde Curve – A Wild Ride.

The image below shows them side by side, and they do look similar. While both charts effectively track the “rollercoaster” of investor psychology and technical de-risking, they emerged from different eras and industries. Both charts have a x-axis that represents time and both have a y-axis that represents expectation ( stock price can be viewed as a measure of expectation).

1. The Lassonde Curve (developed in late 1980s)

Created by Pierre Lassonde, the legendary mining financier and co-founder of Franco-Nevada. The model explains the life cycle of junior mining stocks to investors, explaining why sometimes investors get burned after a discovery even if the project is technically sound.

2. The Gartner Hype Cycle (developed in 1995)

Created by analyst Jackie Fenn at the technology research firm Gartner to help clients distinguish between the “hype” of a new technology and its actual commercial maturity. The model guides corporate IT departments on when to invest in new technologies (e.g., AI, Cloud, VR) without getting burned by the “Peak of Inflated Expectations.”

Does the Gartner HC model use the earlier Lassonde Model as a template? Both models show that humans tend to over-speculate on “newness” (whether it’s a drill hole hit or a new technology) and then lose interest when the hard work begins. It seems that Pierre Lassonde mapped that human behavior a few years before the tech world did. In this aspect, the understanding of investor behavior in junior mining was leading the way for Tech Startup behavior.

Is a PEA Study Like a Tech Product Market Fit (PMF) Study

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

A Preliminary Economic Assessment (PEA or scoping study) is an early-stage technical and economic evaluation of a mineral deposit. Its core purpose is to determine whether a project is potentially viable before committing significant capital to more advanced studies.

Product-Market Fit (PMF) research for a Tech Startup is a structured effort to determine whether a product satisfies a strong market demand. The goal isn’t just to confirm PMF exists; its to understand the who, why, and how it will work before committing to aggressive growth.

Comparing a Preliminary Economic Assessment (PEA) to a Tech Startup’s Product-Market Fit (PMF) stage is a great way to see how both industries similarly “de-risk” an idea before committing big money.

In both worlds, this is the moment where one stops saying “We have a cool idea or a nice deposit” and start saying “We have a viable business.”

1. The “Does This Thing Actually Work?” Test

– Tech (PMF): Once the team has built a beta, they can see if people are using it and are willing to pay for it. They need to prove there is a market for the tech.

– Mining (PEA): The team has found a deposit. The PEA is the first time they can put a dollar sign on it. It’s a conceptual study that predicts “If we build a mine here with these current economic inputs, it should make money.”

2. The Shift from “Geology” to “Economics”

Just as a Tech Startup shifts from coding to customer acquisition cost (CAC), a Junior Miner shifts from geology to metallurgy and CAPEX.

– Tech: It doesn’t matter how good the code is, if it costs >$50 to acquire a customer who only spends $5 it will not be a viable venture.

– Mining: It doesn’t matter if you have 2 million ounces of gold if the rock is difficult to process or if the project costs billions to build. The PEA is the first reality check on these costs.

3. Attracting the Investors

The PEA / PMF stage may be the ultimate gatekeeper for many institutional capitalists.

– Tech: Once you deliver a PMF, Venture Capital (VC) firms may be more willing to provide growth capital to scale the business.

– Mining: Once a positive PEA is released, the company may see a “re-rating.” Larger funds and mid-tier miners may start looking at the project as a real asset rather than just a speculation.

In closing, It is important to remember that both PEA / PMF stages are still early. A tech company with PMF can still be crushed by a competitor or a change in regulatory or platform privacy requirements. A mining project with a PEA can still fail if the Pre-Feasibility Study (PFS) reveals that the environmental permitting or economic factors are not as expected. Neither early stage study is a guarantee for future success, which is another similarity between the two sectors.

Conclusions

There are many parallels between Junior Miners and Tech Startups. The similarities are in how they are built, how they function, and how they acquire funding.

In that way, exploration expenditures can also be viewed through the lens of R&D spending. So it may be improper for some to suggest that the mining industry is not spending enough on R&D, when it actually is spending huge amounts on R&D.

The Junior Mining industry has been around much longer than the Tech Startup world, and hence have led the way in building an ecosystem for speculative investment.

Is it cool to work in the startup world? The answer is yes if its tech, and (unfortunately) no if its mining.

So, you just completed your initial PEA cashflow model and the resulting NPV and IRR are a little disappointing. They are not what everyone was expecting. They don’t meet the ideal targets of an IRR greater than 30% and an NPV that is more than 2x the initial capital cost. The project could now be on life support in the eyes of some.

So, you just completed your initial PEA cashflow model and the resulting NPV and IRR are a little disappointing. They are not what everyone was expecting. They don’t meet the ideal targets of an IRR greater than 30% and an NPV that is more than 2x the initial capital cost. The project could now be on life support in the eyes of some. The discounting of cashflows in a cashflow model means that up-front revenues and costs have a bigger impact on the final economics than those far off in the future. This effect is amplified at higher discount rates.

The discounting of cashflows in a cashflow model means that up-front revenues and costs have a bigger impact on the final economics than those far off in the future. This effect is amplified at higher discount rates. ake to the cashflow model. Sometimes several of the small ones, when compounded together, will result in a significant impact. Here are some of the other cashflow model adjustments that I have seen.

ake to the cashflow model. Sometimes several of the small ones, when compounded together, will result in a significant impact. Here are some of the other cashflow model adjustments that I have seen. Don’t let a disappointing NPV get you down. There may be a few ways to boost the NPV by applying some common practices. However, if after applying all of these adjustments, the NPV still isn’t great, something bigger may be required. That could be an entire project scope re-think.

Don’t let a disappointing NPV get you down. There may be a few ways to boost the NPV by applying some common practices. However, if after applying all of these adjustments, the NPV still isn’t great, something bigger may be required. That could be an entire project scope re-think.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times.

Two dilution approaches are common. One can either construct a diluted block model; or one can apply dilution afterwards in the production schedule. I have used both approaches at different times. Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its service, smoothing the ore delivery to the plant.

Sometimes lower grade stockpiles are built up by the mine each year but only processed at the end of the mine life. Periodically the ore mining rate may exceed the processing rate and other times it may be less. This is where the stockpile provides its service, smoothing the ore delivery to the plant. Once the schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

Once the schedules are finalized, they are normally reviewed by the client for approval. The strip ratio and ore grade profile by date are of interest. One may then be asked to look to at different stockpiling approaches to see if an NPV (i.e. head grade) improvement is possible.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The last task for the mine engineer in Chapter 16 is estimating the open pit equipment fleet and manpower needs. The capital and operating costs for the mining operation will also be calculated as part of this work, but the costs are only presented in Chapter 21.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate.

The support equipment needs (dozers, graders, pickups, mechanics trucks, etc.) are typically fixed. For example, 2 graders per year regardless if the annual tonnages mined fluctuate. These two blog posts hopefully give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

These two blog posts hopefully give an overview of some of the things that mining engineers do as part of their jobs. Hopefully the posts also shed light on the amount of work that goes into Chapter 16 of a 43-101 report. While that chapter may not seem that long compared to some of the others, a lot of the effort is behind the scenes.

So I thought what better way to explain the mining engineer role than by describing the anatomy of a typical Chapter 16 (MINING) in a 43-101 Technical Report. That chapter is a good example of the range of tasks typically undertaken by mining engineers.

So I thought what better way to explain the mining engineer role than by describing the anatomy of a typical Chapter 16 (MINING) in a 43-101 Technical Report. That chapter is a good example of the range of tasks typically undertaken by mining engineers. There is always a mineral resource estimate available before doing a PEA. The way the resource is reported will indicate what type of mine this likely is. The geologists have already done some of the mining engineer’s work.

There is always a mineral resource estimate available before doing a PEA. The way the resource is reported will indicate what type of mine this likely is. The geologists have already done some of the mining engineer’s work. Before starting pit optimization, we require economic inputs from several people. The base case metal prices must be selected (normally with input from the client). The mining operating cost per tonne must be estimated (by the mining engineer). The processing engineers will provide the processing cost and recovery for each ore type.

Before starting pit optimization, we require economic inputs from several people. The base case metal prices must be selected (normally with input from the client). The mining operating cost per tonne must be estimated (by the mining engineer). The processing engineers will provide the processing cost and recovery for each ore type. Once the optimization is run, a series of nested pit shells are created, each with its own tonnes and grade. These shells are compared for incremental strip ratio, incremental head grade, total tonnes, and contained metal.

Once the optimization is run, a series of nested pit shells are created, each with its own tonnes and grade. These shells are compared for incremental strip ratio, incremental head grade, total tonnes, and contained metal. The mining engineer is now ready to undertake the pit design. The pit design step introduces a benched slope profile, smooths out the pit shape, and adds haulroads. Hence a couple of key input parameters are required at this time. The mining engineer will need to know the geotechnical pit slope criteria and the truck size & haul road widths. Let’s look at both of these.

The mining engineer is now ready to undertake the pit design. The pit design step introduces a benched slope profile, smooths out the pit shape, and adds haulroads. Hence a couple of key input parameters are required at this time. The mining engineer will need to know the geotechnical pit slope criteria and the truck size & haul road widths. Let’s look at both of these.

Ramps: Next the mining engineer needs to select the truck size, even though the production schedule has not yet been created.

Ramps: Next the mining engineer needs to select the truck size, even though the production schedule has not yet been created. This ends Part 1. In Part 2 we will discuss the mining engineer’s next tasks; production scheduling; waste dump design; and equipment selection. The mining engineer QP will sign off and take responsibility for all the mine design work done so far. You can read Part 2 at this link “

This ends Part 1. In Part 2 we will discuss the mining engineer’s next tasks; production scheduling; waste dump design; and equipment selection. The mining engineer QP will sign off and take responsibility for all the mine design work done so far. You can read Part 2 at this link “

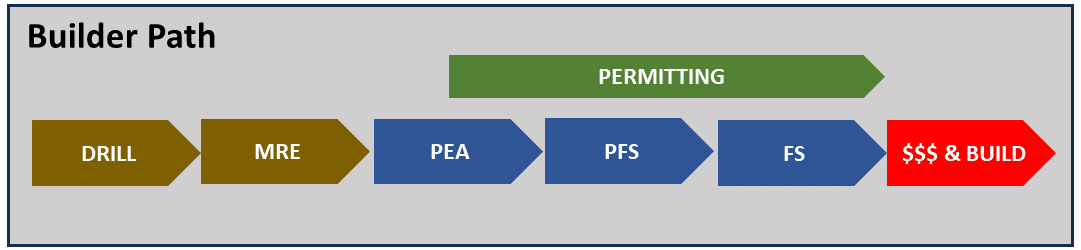

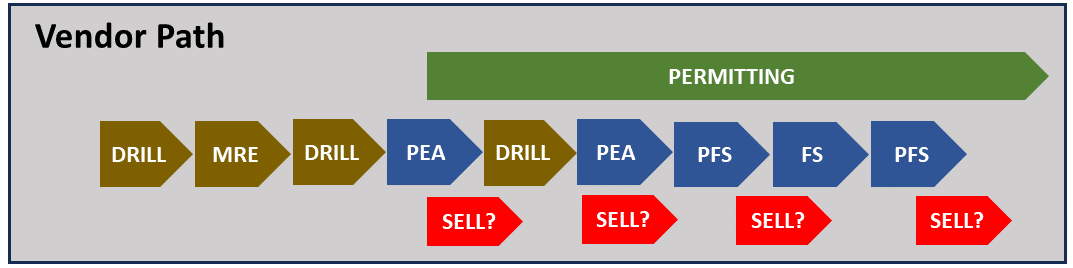

If an engineer understands that a Mine Builder’s project will move from PEA to PFS to FS in rapid succession, then there is more incentive to ensure each study is somewhat integrated.

If an engineer understands that a Mine Builder’s project will move from PEA to PFS to FS in rapid succession, then there is more incentive to ensure each study is somewhat integrated. As an engineer, it is helpful to understand the objectives of the project owner and then tailor the technical studies to meet those objectives. This does not mean low balling costs to make the study a promotional tool. It means focusing on what is important. It means recognizing the path, and what doesn’t need to be engineered in detail at this time. This may save the client time, money, and improve credibility in the long run.

As an engineer, it is helpful to understand the objectives of the project owner and then tailor the technical studies to meet those objectives. This does not mean low balling costs to make the study a promotional tool. It means focusing on what is important. It means recognizing the path, and what doesn’t need to be engineered in detail at this time. This may save the client time, money, and improve credibility in the long run. This post is just a brief discussion of mining project timelines. For those interested, there a few additional project timelines for curiosity purposes. Each path is unique because no two mining projects are the same. You can find these examples at this link “

This post is just a brief discussion of mining project timelines. For those interested, there a few additional project timelines for curiosity purposes. Each path is unique because no two mining projects are the same. You can find these examples at this link “

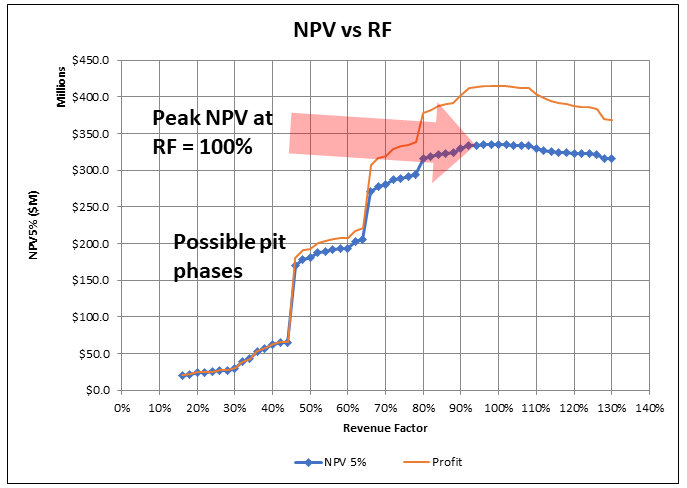

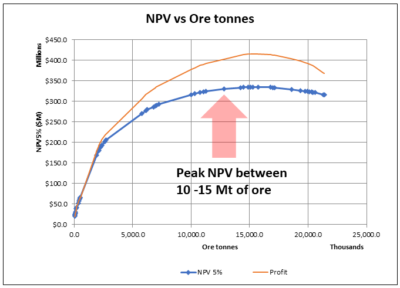

Often in 43-101 technical reports, when it comes to pit optimization, one is presented with the basic “NPV vs Revenue Factor (RF)” curve. That’s it.

Often in 43-101 technical reports, when it comes to pit optimization, one is presented with the basic “NPV vs Revenue Factor (RF)” curve. That’s it.

Pit optimization is a approximation process, as I outlined in a prior post titled “

Pit optimization is a approximation process, as I outlined in a prior post titled “

It’s always a good idea to drill down deeper into the optimization output data, even if you don’t intend to present that analysis in a final report. It will help develop an understanding of the nature of the orebody.

It’s always a good idea to drill down deeper into the optimization output data, even if you don’t intend to present that analysis in a final report. It will help develop an understanding of the nature of the orebody.

While waiting for various third-party due diligences to be completed, the company continue to do exploration drilling. There were still a lot of untested showings on the property and geologists need to stay busy.

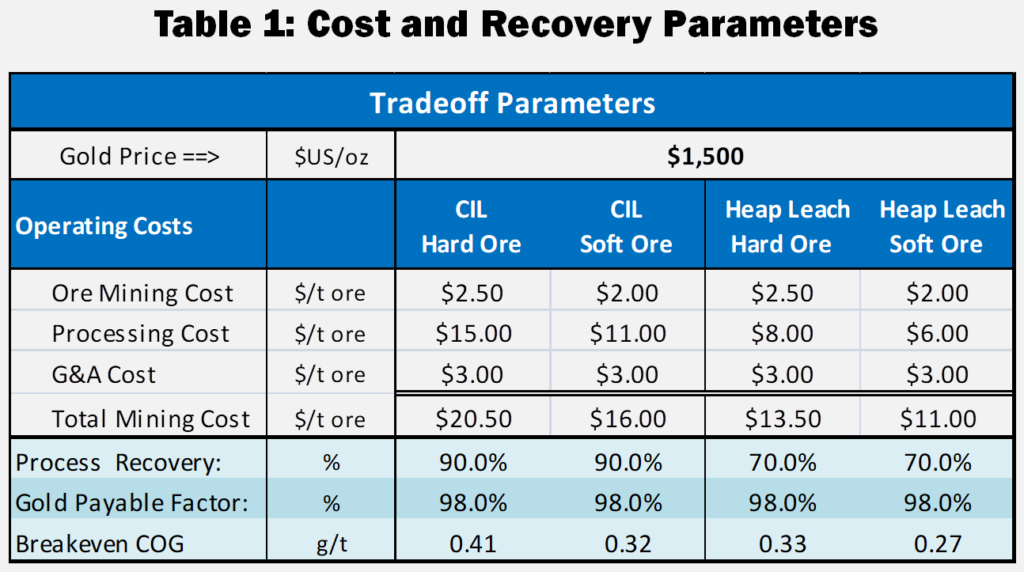

While waiting for various third-party due diligences to be completed, the company continue to do exploration drilling. There were still a lot of untested showings on the property and geologists need to stay busy. With regards to the Heap Leach PEA, we did not wish to complicate the Feasibility Study by adding a new feed supply to that plant from mixed CIL/HL pits. The heap leach project was therefore considered as a separate satellite operation.

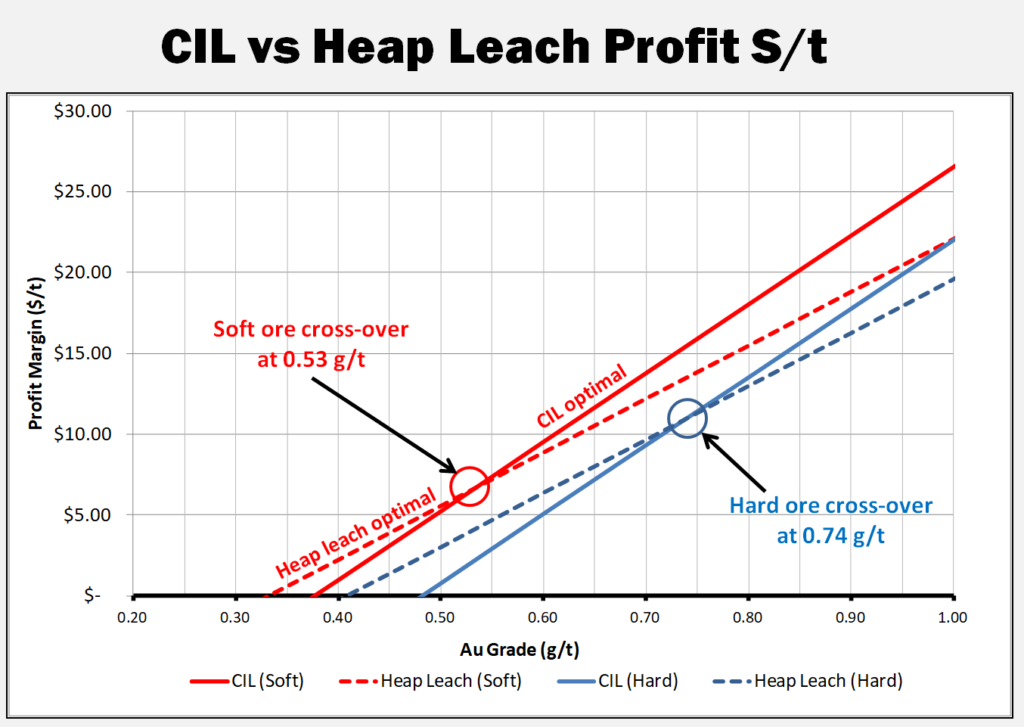

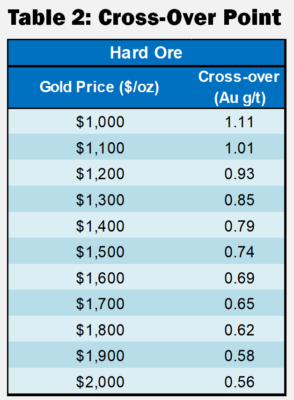

With regards to the Heap Leach PEA, we did not wish to complicate the Feasibility Study by adding a new feed supply to that plant from mixed CIL/HL pits. The heap leach project was therefore considered as a separate satellite operation. I have updated and simplified the trade-off analysis for this blog. Table 1 provides the costs and recoveries used herein, including increasing the gold price to $1500/oz.

I have updated and simplified the trade-off analysis for this blog. Table 1 provides the costs and recoveries used herein, including increasing the gold price to $1500/oz. These cross-over points described in Table 2 are relevant only for the costs shown in Table 1 and will be different for each project.

These cross-over points described in Table 2 are relevant only for the costs shown in Table 1 and will be different for each project.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars. Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members.

Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members. Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there.

Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there. As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

On the site they have a searchable database for tax information for specific countries.

On the site they have a searchable database for tax information for specific countries.