Recently I’ve seen a few LinkedIn conversations about whether the mining industry is spending enough money on Research and Development (R&D). Usually when one thinks of R&D, one might envision the development of new technology, new drug, equipment or software.

I would suggest that mineral exploration should be viewed through the R&D lens. Exploration (or acquisition of explorers) is the most significant way that the industry can self-manage to grow revenues. If exploration is R&D, that then leads to the observation that Junior Miners are the precursors for today’s Silicon Valley startups.

Before venture capital and “startup culture” became a phenomenon, junior mining companies were already operating on the startup core principles. Small, capital driven explorcos were based on unproven assets, led by specialized technical teams. They were funded by investors accepting risk in the hopes for 10 bagger or 100 bagger upsides. This is effectively the same business model that Silicon Valley would build upon.

This blog post examines whether the junior mining industry was a leader in Tech Startup culture. Even things like the Lassonde Curve and the PEA have their comparables in the current tech world.

Are Junior Miners precursors to Tech Startups

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems.

Junior mining companies and Tech Startups share numerous similarities, although they operate in very different worlds. The following comments should recognize that junior mining ecosystem has been around for generations, long before the birth of tech ecosystems.

Junior mining companies and Tech Startups are both high-risk, high-reward ventures. Junior Miners and Tech Startups are early-stage companies where the vast majority fail. Investors accept enormous risk in exchange for the possibility of enormous returns if a discovery or product is a resounding success. Lets look at some of the similarities.

-

A startup spends years (and millions of dollars) building an MVP (Minimum Viable Product). If the market doesn’t want it or the tech fails to scale, the company goes to zero. Similarly if holes don’t hit or the metallurgy is too complex, the mining asset can face significant headwinds.

-

Both mining and tech are essentially “concept” or “pre-revenue” gambles. A Junior Miner typically has no producing mine, just exploration assets and the dream of an economic mineral deposit. Similarly, many Tech Startups have no revenue, just a product idea or some early traction. Investors in both cases are betting on the team and its future value, not on the non-existing cash flow.

-

Both burn through cash (lots of it) before generating revenue. Mining juniors need constant financing rounds (placements) to fund exploration; startups need financing rounds for R&D and growth. Neither can easily self-fund, although bootstrapping is more common in tech than in mining. Both may rely on exit strategies consisting of acquisition from larger industry players.

-

Both generate proprietary data. A Junior Miner’s most valuable asset is often its geological data (drill results, resource estimates, land tenure). A Tech Startup’s asset is its IP, code, or trade secrets. In both cases, the assets are largely intangible until proven economic.

-

Both rely on quality founders and management. A small, skilled team can make or break the company. A geologist or executive with a great track record (“the Midas touch”) is analogous to a serial tech founder. Often the investors are backing the person more than the project.

-

Both sectors are heavily sentiment-driven (mining likes 2025, tech not so much). A hot commodity cycle floods junior mining with capital. A hot tech cycle (AI, crypto, SaaS) floods startups. When investor sentiment reverses, funding dries up fast and many companies are left to die, possibly to rise again in the next cycle.

-

Both sectors can follow the “Lassonde Curve” (mining) or the “Hype Cycle” (tech). There is an initial surge of excitement during discovery/launch, followed by a “boring” period of technical de-risking (development/user acquisition), and finally a re-rating once they reach production or profitability. (More on the Lassonde Curve later in this blog post).

-

Both sectors require pitching their story to investors. The Tech Startups rely on pitching to angel investor via shows like Shark Tank, pitch summits (t) using 5 minute elevator pitches (“get to the point” pitches). The Junior Miners rely on the numerous mining conferences like PDAC, Mines & Money, Beaver Creek, Zurich, again relying on the PowerPoint pitch to gather eyeballs.

Obviously we should also point out there some differences between juniors and Tech Startups.

-

Juniors work with physical geological reality. You either find the ore body or you don’t. Startups can pivot; geology can’t.

-

Mining has far longer timelines; discovery to production can take 10–20 years vs. a startup’s typical 5–7 year VC cycle. Any longer than that, and a Tech Startups technology can become obsolete.

-

Regulatory, environmental permitting, and social license is a constraint for miners with no real startup equivalent. Viable exploration projects can get blocked through no fault of the miner itself.

-

Junior Miners are more commodity-price dependent. Even a great deposit can be uneconomic at the wrong metal price. Conversely a miner’s asset could become more valuable over time based on metal prices. Tech startup do not rely on a commodity price outside their control.

-

Junior Miners tend to rely on public capital markets for financing right from the start, although the trend toward private equity mining investment may be increasing. Conversely, at early stages, Tech Startups tend to be bootstrapped and financed via private equity, venture capital, and angel investors. Junior Miner investments can provide more liquidity and exit opportunities due to their public listing. Tech investors may be locked in until a liquidity event occurs.

-

The startup world will label their financing rounds (seed, Series A, Series B,..) with the hope that future investors provide financing at higher valuations than earlier investors. The mining industry does not label their placement rounds – perhaps they should.

In conclusion, an analogy between Junior Miners and Tech Startups can help outsiders understand the risk, capital structure, and investor behavior of both industries. One might conclude that Junior Miners were the Tech Startups of decades prior, and are still functioning that way today.

Should exploration expenses be considered R&D

Exploration spending shares some of the same characteristics of more commonly R&D.

Exploration spending shares some of the same characteristics of more commonly R&D.

R&D is uncertain in outcome, generates intellectual property (geological data, resource models), and is expensed before any revenue is realized. A pharma company doesn’t know if a new drug will be a win, similarly a Junior Miner doesn’t know if a drill program will yield an economic deposit. Both activities are investments in discovering something of future value, hopefully.

R&D is about de-risking a concept, and de-risking is a term commonly used by Junior Miners. Every drill hole, soil sample, and geophysical survey is a data point that builds knowledge, and even uneconomic drill holes provide value by focusing the search area.

Much like our drug development example, exploration has a high-failure, high-reward path. Early-stage “lab work” (geochemistry/geophysics) leads to “clinical trials” (core drilling) and eventually “commercialization” (feasibility and production).

There are also some differences between exploration and conventional R&D. R&D will typically create proprietary intellectual property, like a new drug or software platform that can be replicated and marketed globally. A mineral discovery is a unique, non-replicable physical asset in a given location. R&D in tech is about creating something from nothing (innovation), while exploration is about finding something that already exists (discovery).

Exploration also tends to be more binary since it is geologically constrained. You either find an ore body or you don’t. You can’t modify or pivot with an orebody. On the other hand, drug and software R&D can yield partial successes or new technologies, that may have other applications.

Although there are both similarities and differences, the analogy is interesting. Exploration may be considered as a hybrid since it has the uncertainty and knowledge-creation aspect of R&D, but the result is a unique physical asset and not IP. In my view exploration is equivalent to R&D.

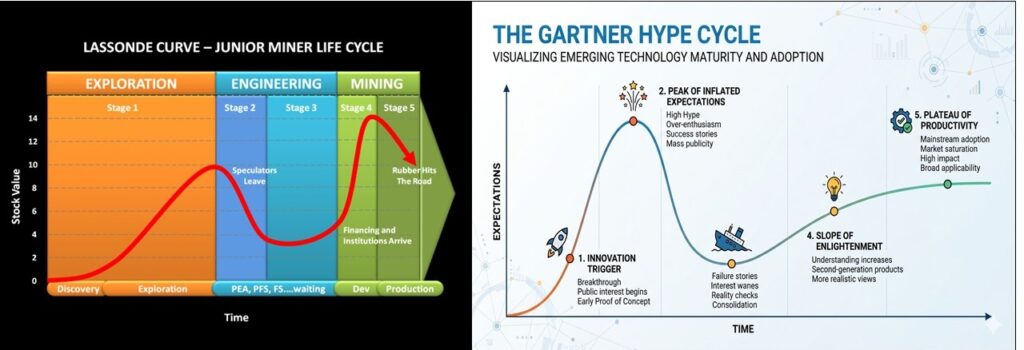

Lassonde Curve vs Hype Cycle Curve

As mentioned previously, junior mining and Tech Startups will follow a cyclic path of hype and despair. In mining it is known as the “Lassonde Curve” and in tech its called the “Gartner Hype Cycle”. Let’s look at the similarities. Which came first?

The Lassonde Curve is the “elder” of the two models, predating the Gartner Hype Cycle by about a decade. I had written a previous blog post on this at Mining’s Lassonde Curve – A Wild Ride.

The image below shows them side by side, and they do look similar. While both charts effectively track the “rollercoaster” of investor psychology and technical de-risking, they emerged from different eras and industries. Both charts have a x-axis that represents time and both have a y-axis that represents expectation ( stock price can be viewed as a measure of expectation).

1. The Lassonde Curve (developed in late 1980s)

Created by Pierre Lassonde, the legendary mining financier and co-founder of Franco-Nevada. The model explains the life cycle of junior mining stocks to investors, explaining why sometimes investors get burned after a discovery even if the project is technically sound.

2. The Gartner Hype Cycle (developed in 1995)

Created by analyst Jackie Fenn at the technology research firm Gartner to help clients distinguish between the “hype” of a new technology and its actual commercial maturity. The model guides corporate IT departments on when to invest in new technologies (e.g., AI, Cloud, VR) without getting burned by the “Peak of Inflated Expectations.”

Does the Gartner HC model use the earlier Lassonde Model as a template? Both models show that humans tend to over-speculate on “newness” (whether it’s a drill hole hit or a new technology) and then lose interest when the hard work begins. It seems that Pierre Lassonde mapped that human behavior a few years before the tech world did. In this aspect, the understanding of investor behavior in junior mining was leading the way for Tech Startup behavior.

Is a PEA Study Like a Tech Product Market Fit (PMF) Study

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

Another similarity between junior mining and tech world is in the way early-stage viability is assessed. This is required to decide whether millions of dollars of further investment is warranted. Miners will complete a PEA. Startups will complete Product-Market Fit research.

A Preliminary Economic Assessment (PEA or scoping study) is an early-stage technical and economic evaluation of a mineral deposit. Its core purpose is to determine whether a project is potentially viable before committing significant capital to more advanced studies.

Product-Market Fit (PMF) research for a Tech Startup is a structured effort to determine whether a product satisfies a strong market demand. The goal isn’t just to confirm PMF exists; its to understand the who, why, and how it will work before committing to aggressive growth.

Comparing a Preliminary Economic Assessment (PEA) to a Tech Startup’s Product-Market Fit (PMF) stage is a great way to see how both industries similarly “de-risk” an idea before committing big money.

In both worlds, this is the moment where one stops saying “We have a cool idea or a nice deposit” and start saying “We have a viable business.”

1. The “Does This Thing Actually Work?” Test

– Tech (PMF): Once the team has built a beta, they can see if people are using it and are willing to pay for it. They need to prove there is a market for the tech.

– Mining (PEA): The team has found a deposit. The PEA is the first time they can put a dollar sign on it. It’s a conceptual study that predicts “If we build a mine here with these current economic inputs, it should make money.”

2. The Shift from “Geology” to “Economics”

Just as a Tech Startup shifts from coding to customer acquisition cost (CAC), a Junior Miner shifts from geology to metallurgy and CAPEX.

– Tech: It doesn’t matter how good the code is, if it costs >$50 to acquire a customer who only spends $5 it will not be a viable venture.

– Mining: It doesn’t matter if you have 2 million ounces of gold if the rock is difficult to process or if the project costs billions to build. The PEA is the first reality check on these costs.

3. Attracting the Investors

The PEA / PMF stage may be the ultimate gatekeeper for many institutional capitalists.

– Tech: Once you deliver a PMF, Venture Capital (VC) firms may be more willing to provide growth capital to scale the business.

– Mining: Once a positive PEA is released, the company may see a “re-rating.” Larger funds and mid-tier miners may start looking at the project as a real asset rather than just a speculation.

In closing, It is important to remember that both PEA / PMF stages are still early. A tech company with PMF can still be crushed by a competitor or a change in regulatory or platform privacy requirements. A mining project with a PEA can still fail if the Pre-Feasibility Study (PFS) reveals that the environmental permitting or economic factors are not as expected. Neither early stage study is a guarantee for future success, which is another similarity between the two sectors.

Conclusions

There are many parallels between Junior Miners and Tech Startups. The similarities are in how they are built, how they function, and how they acquire funding.

In that way, exploration expenditures can also be viewed through the lens of R&D spending. So it may be improper for some to suggest that the mining industry is not spending enough on R&D, when it actually is spending huge amounts on R&D.

The Junior Mining industry has been around much longer than the Tech Startup world, and hence have led the way in building an ecosystem for speculative investment.

Is it cool to work in the startup world? The answer is yes if its tech, and (unfortunately) no if its mining.

**end**

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening.

I recently noticed a few new mining studies that relied on toll milling as their base case operation. This made me wonder if this is a trend and if there are more examples of where this is happening. USER PROMPT: What are the risks of toll milling plan.

USER PROMPT: What are the risks of toll milling plan. RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia.

RESPONSE: The Qualified Person (QP) signing off on a technical study that uses toll milling as the base case carries significant professional and regulatory responsibility, particularly under NI 43-101 in Canada or JORC in Australia. The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

The results given by Claude are quite thorough and insightful. It’s hard to argue with its observations and conclusions. This research took all of 30 seconds, so I can see it is no longer difficult to become a blog writer. Writing isn’t the challenge; finding interesting topics is.

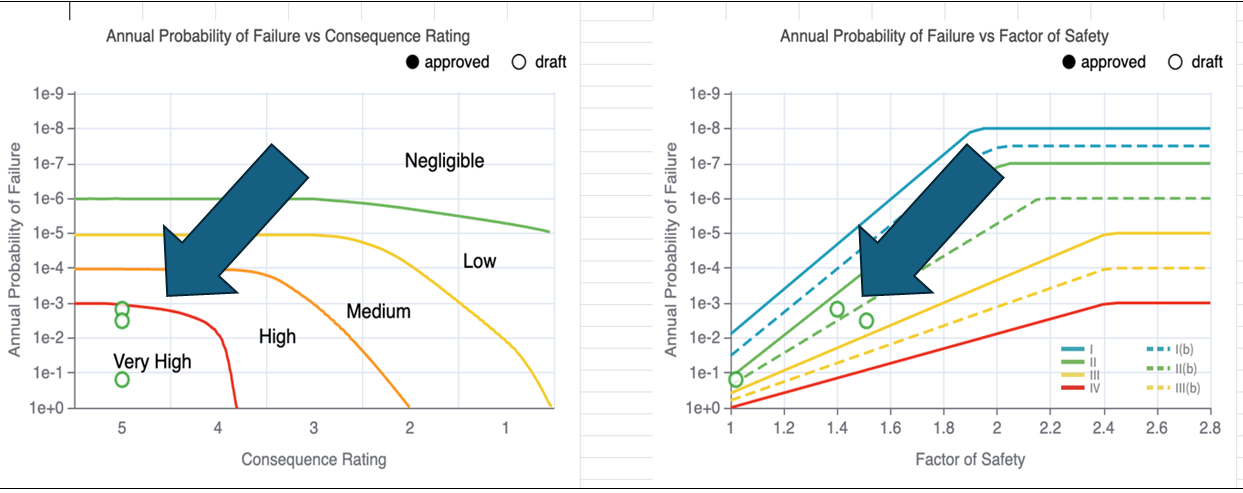

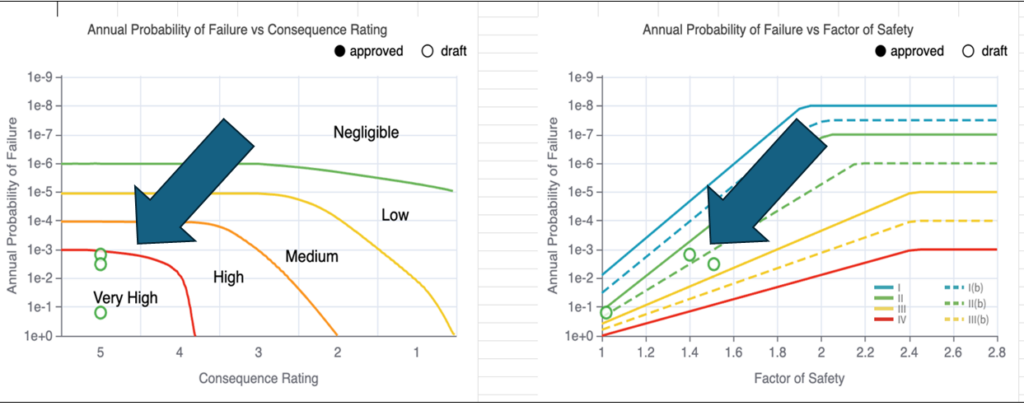

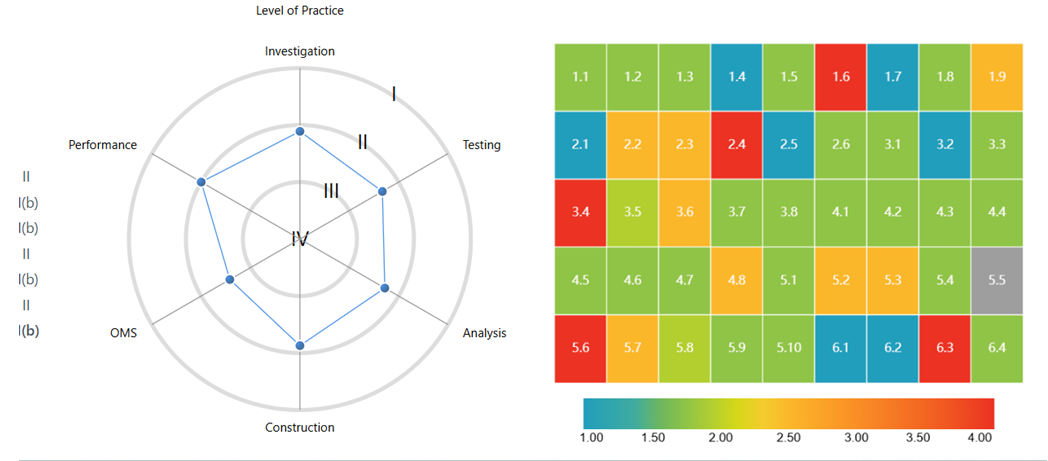

In my view, having a single industry platform for critical infrastructure risk management provides several benefits. These are:

In my view, having a single industry platform for critical infrastructure risk management provides several benefits. These are: Each mine site is unique with its own set of “Facilities”. For example, the individual Facilities could include Tailing Management Area #1, TMA #2, the Heap Leach Pad, Waste Dump #1, Waste Dump #2, etc.

Each mine site is unique with its own set of “Facilities”. For example, the individual Facilities could include Tailing Management Area #1, TMA #2, the Heap Leach Pad, Waste Dump #1, Waste Dump #2, etc. The Level of Practice (LOP) is a measure of the integrity and quality of data used to design and manage a mine facility. The CI-RiskDB platform currently uses 45 criteria to evaluate the LOP associated with a facility. For example, these quality criteria include items such as: current understanding of soil profile; testing & verification between lab and field investigations; stability analysis detail; construction QA/QC undertaken, monitoring programs, etc.

The Level of Practice (LOP) is a measure of the integrity and quality of data used to design and manage a mine facility. The CI-RiskDB platform currently uses 45 criteria to evaluate the LOP associated with a facility. For example, these quality criteria include items such as: current understanding of soil profile; testing & verification between lab and field investigations; stability analysis detail; construction QA/QC undertaken, monitoring programs, etc.

Over confidence of personnel is something that can unfortunately play a role in risk management. However, the more eyes involved with reviews and signoffs, as well as occasional third party audits, the less likely that this occurs (hopefully).

Over confidence of personnel is something that can unfortunately play a role in risk management. However, the more eyes involved with reviews and signoffs, as well as occasional third party audits, the less likely that this occurs (hopefully). In closing, as of this month December 2025, I understand the Critical Infrastructure Risk Decision Basis platform is currently being piloted and implemented at a number of mine sites in Canada, including Agnico Eagle at a corporate level. Additional pilots may be forthcoming in 2026.

In closing, as of this month December 2025, I understand the Critical Infrastructure Risk Decision Basis platform is currently being piloted and implemented at a number of mine sites in Canada, including Agnico Eagle at a corporate level. Additional pilots may be forthcoming in 2026.

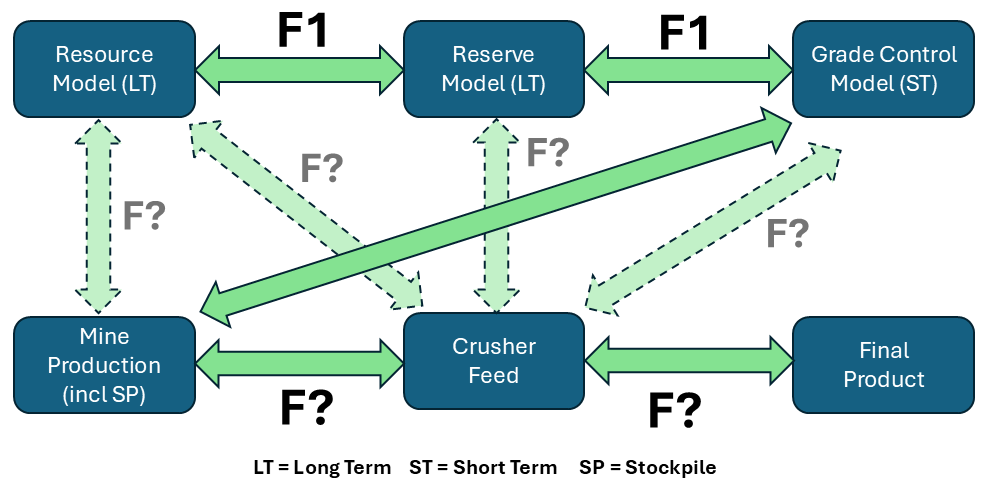

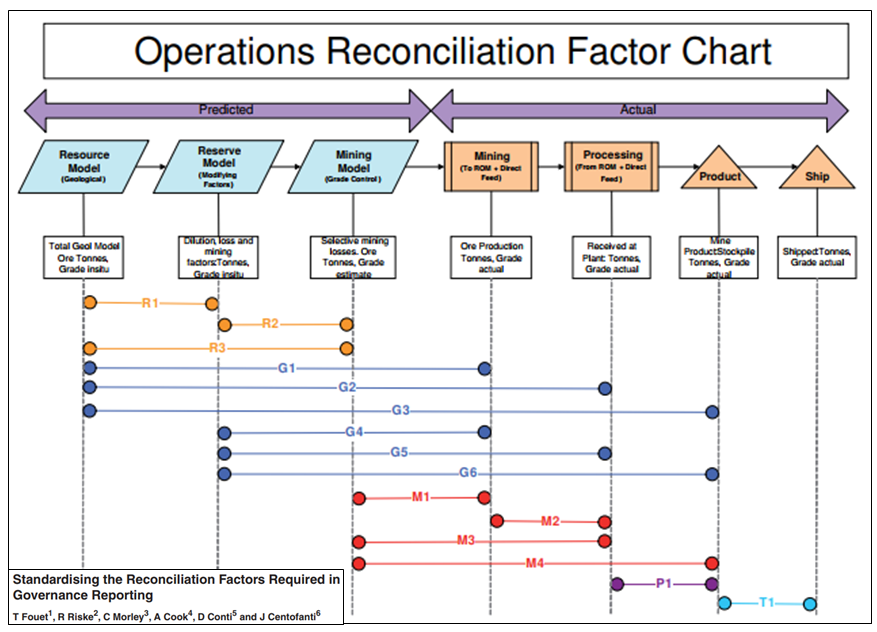

The mining industry is implementing more and more technology in the mining cycle.

The mining industry is implementing more and more technology in the mining cycle. Mine reconciliation requires information such as initial predictions from exploration data and geological models, actual measurement: data from mining sources, such as blast holes, stockpile samples, or mill feed. As well it will need data on the final product being shipped off site. Do the metal quantities balance out throughout the mining operation?

Mine reconciliation requires information such as initial predictions from exploration data and geological models, actual measurement: data from mining sources, such as blast holes, stockpile samples, or mill feed. As well it will need data on the final product being shipped off site. Do the metal quantities balance out throughout the mining operation?

Each mine site may be unique with respect to; ore sources; terminology; ore types; mining methods; stockpiling philosophy; processing methods; technology availability; and personnel capability. So often the easiest approach for mine reconciliation is based on the Excel spreadsheet. (Reconciliation is generally not an easy undertaking).

Each mine site may be unique with respect to; ore sources; terminology; ore types; mining methods; stockpiling philosophy; processing methods; technology availability; and personnel capability. So often the easiest approach for mine reconciliation is based on the Excel spreadsheet. (Reconciliation is generally not an easy undertaking).

On YouTube, there are also a lot of educational videos related to mining. Some of the same audio podcast episodes are also available on the YouTube platform. Given an option, I prefer the audio-only podcast format over YouTube.

On YouTube, there are also a lot of educational videos related to mining. Some of the same audio podcast episodes are also available on the YouTube platform. Given an option, I prefer the audio-only podcast format over YouTube. Pick and choose. One can’t listen to all the podcast episodes available or else you wouldn’t have time to do anything else in life. You would also become bored since much of it can be repetitive.

Pick and choose. One can’t listen to all the podcast episodes available or else you wouldn’t have time to do anything else in life. You would also become bored since much of it can be repetitive. Mining Stock Education (680 episodes)

Mining Stock Education (680 episodes)  Fresh Thinking by Optiro-Snowden (53 episodes) This podcast is hosted by Snowdon – Optiro consultants. They typically focus on resource modelling and grade reconciliation aspects. The episodes are fairly short (15 mins), which is nice. Although I am not a resource modeller, I can always learn more about the black art of resource modelling.

Fresh Thinking by Optiro-Snowden (53 episodes) This podcast is hosted by Snowdon – Optiro consultants. They typically focus on resource modelling and grade reconciliation aspects. The episodes are fairly short (15 mins), which is nice. Although I am not a resource modeller, I can always learn more about the black art of resource modelling. To the best of my knowledge, there are a lack of podcasts related to mine engineering, for topics such as pit optimization, mine design, scheduling, equipment selection, and costing.

To the best of my knowledge, there are a lack of podcasts related to mine engineering, for topics such as pit optimization, mine design, scheduling, equipment selection, and costing. There is no shortage of material in the podcast world about the mining industry. It all depends on what interests you the most. There is even more mining information available on YouTube, if you have the time to sit and watch videos. Nevertheless the audio-only platform is great, although you don’t get to see the charts being discussed. That’s fine with me, particularly if they take a few seconds to describe the chart.

There is no shortage of material in the podcast world about the mining industry. It all depends on what interests you the most. There is even more mining information available on YouTube, if you have the time to sit and watch videos. Nevertheless the audio-only platform is great, although you don’t get to see the charts being discussed. That’s fine with me, particularly if they take a few seconds to describe the chart.

NPV One is targeting to replace the typical Excel based cashflow model with an online cloud model. It reminds me of personal income tax software, where one simply inputs the income and expense information, and then the software takes over doing all the calculations and outputting the result.

NPV One is targeting to replace the typical Excel based cashflow model with an online cloud model. It reminds me of personal income tax software, where one simply inputs the income and expense information, and then the software takes over doing all the calculations and outputting the result. Pros

Pros Like anything, nothing is perfect and NPV may have a few issues for me.

Like anything, nothing is perfect and NPV may have a few issues for me. The NPV One software is an option for those wishing to standardize or simplify their financial modelling.

The NPV One software is an option for those wishing to standardize or simplify their financial modelling.

This game is part of a coal-mining game trilogy created by Thomas Spitzer in Germany. The players take the role of farmers with opportunities to exploit the presence of coal in the Ruhr region of Germany. During the game, players acquire knowledge about coal, extend their farms, and dig deeper in the ground to extract more coal.

This game is part of a coal-mining game trilogy created by Thomas Spitzer in Germany. The players take the role of farmers with opportunities to exploit the presence of coal in the Ruhr region of Germany. During the game, players acquire knowledge about coal, extend their farms, and dig deeper in the ground to extract more coal. In the second game of Spitzer’s trilogy, you are still in the Ruhr region in the 18th century, at the beginning of the industrial revolution. The Ruhr river presented a transportation route from the coal mines. However, the Ruhr was filled with obstacles and large dams, making it incredibly difficult to navigate.

In the second game of Spitzer’s trilogy, you are still in the Ruhr region in the 18th century, at the beginning of the industrial revolution. The Ruhr river presented a transportation route from the coal mines. However, the Ruhr was filled with obstacles and large dams, making it incredibly difficult to navigate. This game may still be in German text only. Players are the administrator of a coal mine, and experience competition while living through a piece of Ruhr Valley history.

This game may still be in German text only. Players are the administrator of a coal mine, and experience competition while living through a piece of Ruhr Valley history. This game takes on a more negative view of the mining industry. It is described as “A bold take on the economics in the brutal industry that is asbestos.” The game players assume the role of a global asbestos company.

This game takes on a more negative view of the mining industry. It is described as “A bold take on the economics in the brutal industry that is asbestos.” The game players assume the role of a global asbestos company. In 1983 my brother, at the age of 10, got his Commodore 64 computer and was eagerly learning to program in BASIC. He was always looking for ideas on what he could write programs about. I had graduated from McGill in Mining Engineering a few years earlier, so I suggested he write a simple computer game about mining as his project.

In 1983 my brother, at the age of 10, got his Commodore 64 computer and was eagerly learning to program in BASIC. He was always looking for ideas on what he could write programs about. I had graduated from McGill in Mining Engineering a few years earlier, so I suggested he write a simple computer game about mining as his project. Over the last few months I decided to learn VBA (Visual Basic for Applications). VBA is a programming language the works with Microsoft Office products, mainly Excel.

Over the last few months I decided to learn VBA (Visual Basic for Applications). VBA is a programming language the works with Microsoft Office products, mainly Excel.

Mining has been a part of my life for as long as I can remember. Being born in Sudbury, many of my family members have been, or are currently involved, in mining through a variety of occupations, including my father who I idolized. However, I never knew my true interest in the industry until my 11th-grade technology class. I had a teacher who was passionate about the mining industry, and he created a project that involved developing a very basic mine design.

Mining has been a part of my life for as long as I can remember. Being born in Sudbury, many of my family members have been, or are currently involved, in mining through a variety of occupations, including my father who I idolized. However, I never knew my true interest in the industry until my 11th-grade technology class. I had a teacher who was passionate about the mining industry, and he created a project that involved developing a very basic mine design. Before my first year of university, I had a summer job tramming at Macassa Mine in Kirkland Lake Ontario, which has been in production since 1933. My mentality was to get the boots on the ground and get the job done, whatever it took (with proper safety precautions of course). Using rail systems, dumping ore cars manually, jackleg drilling, etc. gave me the perspective that mining was archaic, mining was rough, and mining was only about the ounces.

Before my first year of university, I had a summer job tramming at Macassa Mine in Kirkland Lake Ontario, which has been in production since 1933. My mentality was to get the boots on the ground and get the job done, whatever it took (with proper safety precautions of course). Using rail systems, dumping ore cars manually, jackleg drilling, etc. gave me the perspective that mining was archaic, mining was rough, and mining was only about the ounces. To change the negative view around mining, I believe the main focal point should be electric equipment and the ability for remote operation/work. With all this newly developed technology at our fingertips, I know that future operations will be safer and more sustainable, which should be better portrayed.

To change the negative view around mining, I believe the main focal point should be electric equipment and the ability for remote operation/work. With all this newly developed technology at our fingertips, I know that future operations will be safer and more sustainable, which should be better portrayed. Even creating a mining simulation video game where you can run through a story of being a manager, excavator/scoop operator, truck driver, etc. would get the thought of mining brought into the coming generations at a younger age. This would increase the talent pool from the more typical operator because more and more youth are getting skilled at remote operation through video games due to their increased screen time.

Even creating a mining simulation video game where you can run through a story of being a manager, excavator/scoop operator, truck driver, etc. would get the thought of mining brought into the coming generations at a younger age. This would increase the talent pool from the more typical operator because more and more youth are getting skilled at remote operation through video games due to their increased screen time. People get comfortable and people are afraid to leave home, so selling a career that allows for boundless flexibility in job tasks and constant stimulation while living wherever you desire could allow a shrinkage in the current technical gap.

People get comfortable and people are afraid to leave home, so selling a career that allows for boundless flexibility in job tasks and constant stimulation while living wherever you desire could allow a shrinkage in the current technical gap. So do I think the mining industry is archaic…. not anymore.

So do I think the mining industry is archaic…. not anymore. Firstly, I would like to thank this engineer for taking time to write out his well formed thoughts, and for allowing me to share them.

Firstly, I would like to thank this engineer for taking time to write out his well formed thoughts, and for allowing me to share them.

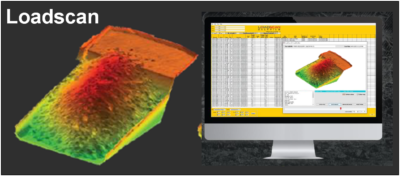

Loadscan has been around for a few years, but I only became aware of it recently. It is a technology that allows the rapid assessment of the load being carried in truck. It does not rely on the use of load cells or weigh scales to measure the payload.

Loadscan has been around for a few years, but I only became aware of it recently. It is a technology that allows the rapid assessment of the load being carried in truck. It does not rely on the use of load cells or weigh scales to measure the payload. What is interesting about this technology is that it is simple to install in an operation. It does not require retrofitting of a truck.

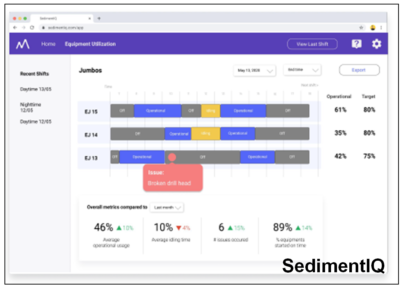

What is interesting about this technology is that it is simple to install in an operation. It does not require retrofitting of a truck. SedimentIQ is a new smartphone vehicle tracking platform that is trying to establish itself. Their proposed technology makes use of a phone’s built-in GPS, Bluetooth, and accelerometer to track vehicle operation. The phone’s sensor can measure vibrations produced by an operating truck or loader.

SedimentIQ is a new smartphone vehicle tracking platform that is trying to establish itself. Their proposed technology makes use of a phone’s built-in GPS, Bluetooth, and accelerometer to track vehicle operation. The phone’s sensor can measure vibrations produced by an operating truck or loader. The SedimentIQ software will aggregate the cycle time and delay information and upload it in real time to a cloud based database. A web-based dashboard allows anyone with access to view the real time production data graphically or export it to Excel.

The SedimentIQ software will aggregate the cycle time and delay information and upload it in real time to a cloud based database. A web-based dashboard allows anyone with access to view the real time production data graphically or export it to Excel.