In a previous article I outlined my thoughts on the usefulness of early stage financial modelling (“Early Stage “What-if” Mine Economic Analysis – Its Valuable”). My observation was that it is useful to take a few days to build a simple cashflow model to help your team better understand your project.

By “simple” I mean really simple.

This blog describes one of the techniques that I use to take a super-quick look at any project; whether it is for a client wishing to understand his project at a high level; or whether it is a project that I have read about. There isn’t any actual study or production schedule available yet. Maybe there is only a mineral resource estimate available.

It takes about 10 minutes to plug the numbers into my template to get fast results. The image below is an example of the simple model that I use, but anyone can build one for themselves.

Screenshot of Simple Economic Model

I use the term one dimensional (“1D”) model since it doesn’t use the typical X-Y matrix with years across the top and production data down the page.

The 1D model simply relies simple on life of mine (“LOM”) totals to estimate the total revenue, total operating cost, and total profit. This determines how much capital expenditure the project can tolerate.

The only caveat is that you need to have some sense for operating and capital costs for similar projects. This analysis can be on both a pre-tax and simple after-tax basis.

Using estimated metal prices and recoveries, the first step is to calculate the incremental revenue generated by each tonne of ore (see a previous article “Ore Value Calculator – What’s My Ore Worth?”).

Next that revenue per tonne is multiplied by the total ore tonnage to arrive at the total revenue over the life of mine.

The second step is to determine the life of mine operating cost, and again this simple calculation is based on estimated unit operating costs multiplied by the total tonnages being handled.

The third step is to calculate the life of mine profit based on total revenue minus total operating cost.

The potential net cashflow would be calculated by deducting an assumed capital cost from the life-of-mine profit. The average annual cashflow is estimated based on the net cashflow divided by the mine life. An approximate NPV can be calculated by determining the Present Value of a series of annual payments at a certain discount rate.

The reasonableness of the 1D model will be examined via benchmarking and this will be summarized once completed. I will include a link to that future blog here.

You need to understand your project

One can easily evaluate the potential impact of changing metal prices, changing recoveries, ore tonnages, operating costs, etc. to see what the economic or operational drivers are for this project. This can help you understand what you might need in order to make the project viable.

One can easily evaluate the potential impact of changing metal prices, changing recoveries, ore tonnages, operating costs, etc. to see what the economic or operational drivers are for this project. This can help you understand what you might need in order to make the project viable.

Conclusion

The bottom line is that a 1D economic calculation is very simplistic but still provides a vision for the project. The next step in the economic modelling process would be a 2D model based on an annual production schedule. The 1D approach is just a quick first step in looking at the potential. You can do it even when you only know the head grades and some generalized orebody information.

The two ways you can apply the simple 1-D model are:

-

evaluate the potential of early stage projects using cost inputs from other studies,

-

examine a project’s sensitives (units costs, recoveries, prices) by calibrating your simple model to the published study (i.e. use the same parameters and make changes as needed.

The entire blog post library can be found at this LINK with topics ranging from geotechnical, financial modelling, and junior mining investing.

Note: If you would like to get notified when new blogs are posted, then sign up on the KJK mailing list on the website.

His topic is interesting and relevant to today’s mining industry. Paul raised many thoughtful points supported by data. He gave me permission to share his information.

His topic is interesting and relevant to today’s mining industry. Paul raised many thoughtful points supported by data. He gave me permission to share his information. I agree with many of the points raised by Paul in his study. The mining industry has some credibility issues based on recent performance and therefore understanding the causes and then repairing that credibility will be important for the future.

I agree with many of the points raised by Paul in his study. The mining industry has some credibility issues based on recent performance and therefore understanding the causes and then repairing that credibility will be important for the future.

My question is why not stockpile the extra gold and wait for gold prices to rise? This might be an option if the company doesn’t really need the money now or doesn’t plan to gamble on exploration or acquisitions.

My question is why not stockpile the extra gold and wait for gold prices to rise? This might be an option if the company doesn’t really need the money now or doesn’t plan to gamble on exploration or acquisitions.

It seems that as soon as there is a price spike or positive market narrative, a commodity specific projects can take on a life of their own. The following list gives a few examples and, when you reflect upon them, ask how many actually came into successful production. These events occur at different times in different economic cycles.

It seems that as soon as there is a price spike or positive market narrative, a commodity specific projects can take on a life of their own. The following list gives a few examples and, when you reflect upon them, ask how many actually came into successful production. These events occur at different times in different economic cycles.

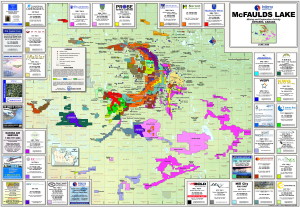

We have all seen the staking rushes that occur when a world class prospect is discovered. I’m sure we can all recall getting the large claim maps (as shown) with their multicolored graphics showing the patchwork of acquisitions around a discovery. PDAC was great for distributing these. They were well done and interesting to study.

We have all seen the staking rushes that occur when a world class prospect is discovered. I’m sure we can all recall getting the large claim maps (as shown) with their multicolored graphics showing the patchwork of acquisitions around a discovery. PDAC was great for distributing these. They were well done and interesting to study. Even mining or processing technologies could get caught up in somewhat of a wave and become a fad for further study. Sometimes this is driven by suppliers or consultants. For the engineers out there, who can recall…

Even mining or processing technologies could get caught up in somewhat of a wave and become a fad for further study. Sometimes this is driven by suppliers or consultants. For the engineers out there, who can recall…

On the site they have a searchable database for tax information for specific countries.

On the site they have a searchable database for tax information for specific countries.

Tailings dam stability is so important that in some jurisdictions regulators may be requiring that mining companies have third party independent review boards or third party audits done on their tailings dams. The feeling is that, although a reputable consultant may be doing the dam design, there is still a need for some outside oversight.

Tailings dam stability is so important that in some jurisdictions regulators may be requiring that mining companies have third party independent review boards or third party audits done on their tailings dams. The feeling is that, although a reputable consultant may be doing the dam design, there is still a need for some outside oversight. Nowadays most small companies do not develop their own in-house resource estimates. The task is generally awarded to an independent QP.

Nowadays most small companies do not develop their own in-house resource estimates. The task is generally awarded to an independent QP.

One downside to a third party review is the added cost to the owner.

One downside to a third party review is the added cost to the owner.

Their corporate website states that they would pay, for a specified period of time, the claim fees/taxes related to existing mineral properties or related to the staking of new mineral properties.

Their corporate website states that they would pay, for a specified period of time, the claim fees/taxes related to existing mineral properties or related to the staking of new mineral properties.

Mining companies are constantly in the media with stories of cost over-runs, mine shutdowns, fatalities, strikes & protests, and environmental incidents.

Mining companies are constantly in the media with stories of cost over-runs, mine shutdowns, fatalities, strikes & protests, and environmental incidents. The larger mining companies will always have their investors like pension funds and mutual funds, however the junior miners may be a different story.

The larger mining companies will always have their investors like pension funds and mutual funds, however the junior miners may be a different story.

Once the optimization step is complete, mining engineers will then design the pit inside that shell, introducing benches and ramps. The pit design should mimic the selected optimized shell as closely as possible.

Once the optimization step is complete, mining engineers will then design the pit inside that shell, introducing benches and ramps. The pit design should mimic the selected optimized shell as closely as possible.