Google Earth is a great tool and it’s free for everyone to use. No doubt that many of us in the mining industry already use it regularly.

Previously I had written an article about how Google Earth can be used to give your entire engineering team a virtual site visit. It’s cheaper than flying everyone to site. That blog is available at this link “Google Earth – Keep it On Hand”.

What else can Google Earth do for me?

The Investor Relations (IR) department in a mining company can also take advantage of Google Earth’s capabilities. Typically the IR team are responsible for creating a myriad of PowerPoint investor presentations. Their slideshows will include graphics highlighting the project location, showing exploration drilling and planned site facilities for advanced projects. This is where Google Earth can be used to create a more interactive experience for investors.

Google Earth with 3D Buildings

Rather than relying only on PowerPoint, the technical team can create drillhole maps, 3D infrastructure layouts, open pit plans, 3D tailings dams, and import them into Google Earth.

By creating a KMZ file, one can share this information with investors, analysts, and stakeholders. This will provide an interactive opportunity to view the information themselves.

Viewers could fly around the site, zoom in and out as needed, examine things in 3D, and even measure distances. Viewers can even save the project in Google Earth and return back whenever curiosity dictates.

I have been a part of engineering teams where Google Earth has been used to share layout information. However I have not yet seen such information offered as a downloadable KMZ file to external parties. If you know of any companies that are currently doing this, please let me know (kjkltd@rogers.com) and I will share their link here.

There also is VRIFY

VRIFY is a new cloud based platform that provides 3D viewing capability. It provides a map based graphic tool to IR departments for sharing project information. VRIFY can also enhance collaboration among engineering teams by enabling a group to view a virtual project and sketch on the image in real time.

VRIFY desktop screenshot

VRIFY also allows more detailed information to be displayed in the form of hotspots within a project. Click on them to get more information on that topic (see image to the right).

Although I have only been given a demo of VRIFY, it appears to be a nice package that provides more functionality than Google Earth. Unfortunately VRIFY is not free for a company to use. The minimum subscription cost is about $10,000 (plus extras).

In June 2019 VRIFY made a deal with Kirkland Lake Gold whereby interested property vendors can submit their project to Kirkland Lake management for their review.

Here is the link (https://vrify.com/dealroom). In the proposed approach, the project information is submitted using the VRIFY platform. Essentially some of the same information presented in a PowerPoint is now provided in a more interactive fashion. Participating companies must first enter into a client service agreement with VRIFY. We will see how this idea works, since it does add a cost and new complexity for the property vendor.

There is another cloud based service called Reality Check, which offers virtual reality site visits.

Conclusion

The bottom line is that the trend in the mining industry is towards more open data sharing whether you’re connecting with the public or within your own engineering team. New and old cloud based platform tools can be used to do this. It just depends on your budget.

Note: If you would like to get notified when new blogs are posted, then sign up on the KJK mailing list on the website. Otherwise I post notices on LinkedIn, so follow me at: https://www.linkedin.com/in/kenkuchling/.

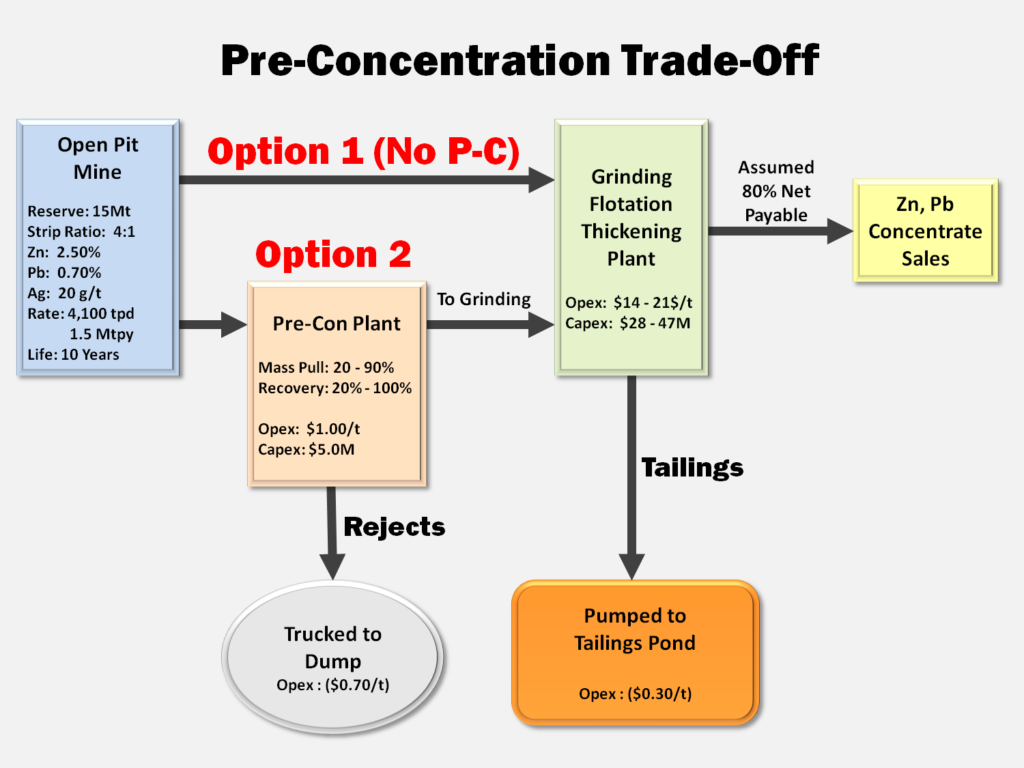

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

Concentrate handling systems may not differ much between model options since roughly the same amount of final concentrate is (hopefully) generated.

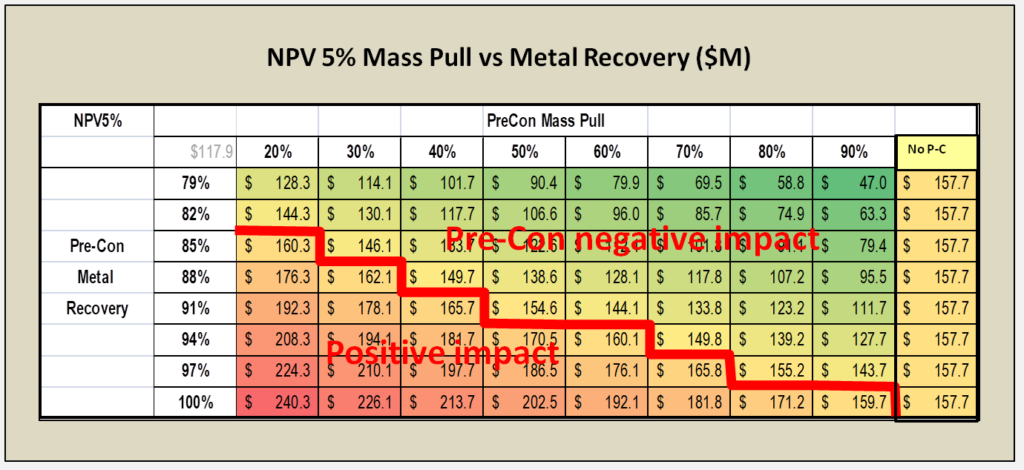

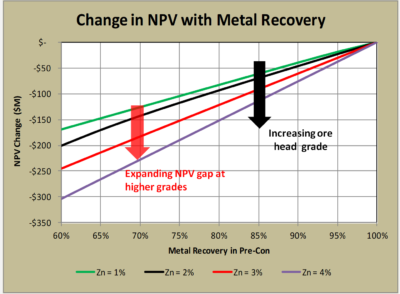

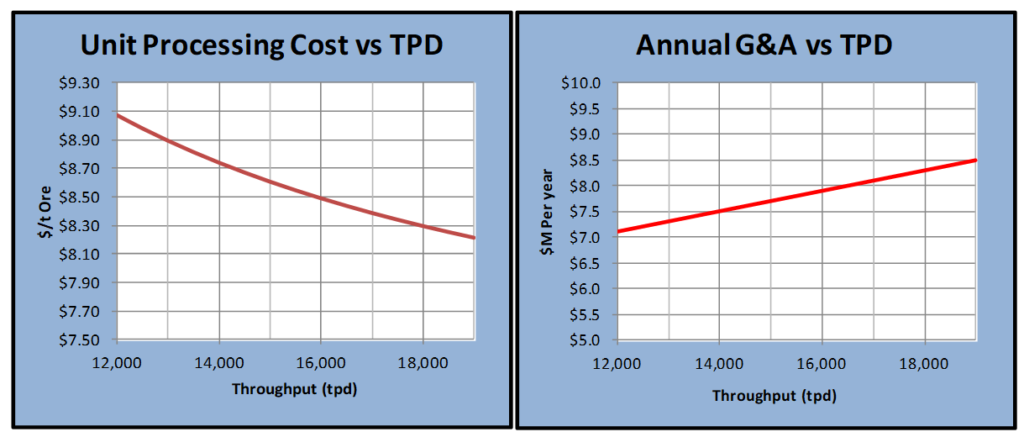

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

4. The head grade of the deposit also determines how economically risky pre-concentration might be. In higher grade ore bodies, the negative impact of any metal loss in pre-concentration may be offset by accepting higher cost for grinding (see chart on the right).

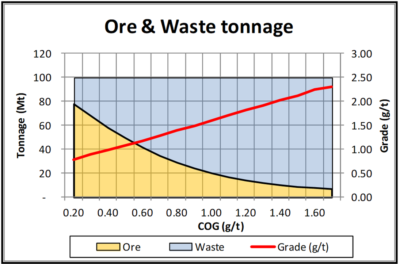

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

I had a grade tonnage curve, including the tonnes of ore and waste, for a designed pit. This data is shown graphically on the right. Essentially the mineable reserve is 62 Mt @ 0.94 g/t Pd with a strip ratio of 0.6 at a breakeven cutoff grade of 0.35 g/t. It’s a large tonnage, low strip ratio, and low grade deposit. The total pit tonnage is 100 Mt of combined ore and waste.

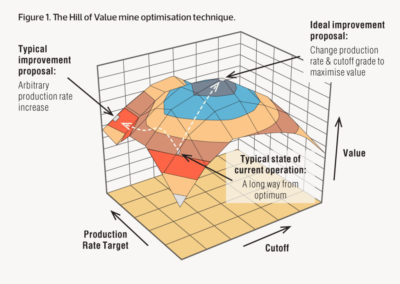

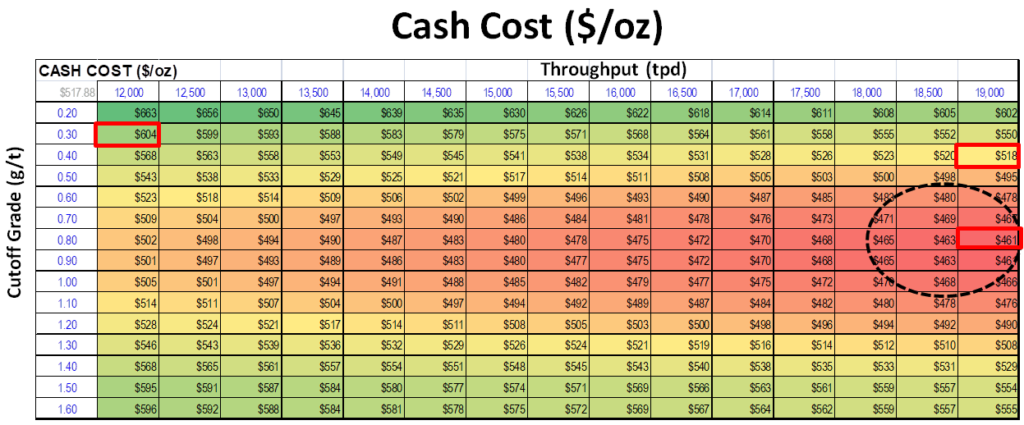

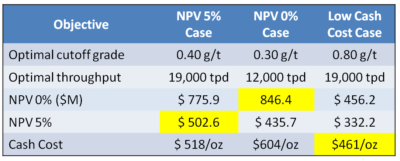

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

The Hill of Value is an interesting optimization concept to apply to a project. In the example I have provided, the optimal project varies depending on what the financial objective is. I don’t know if this would be the case with all projects, however I suspect so.

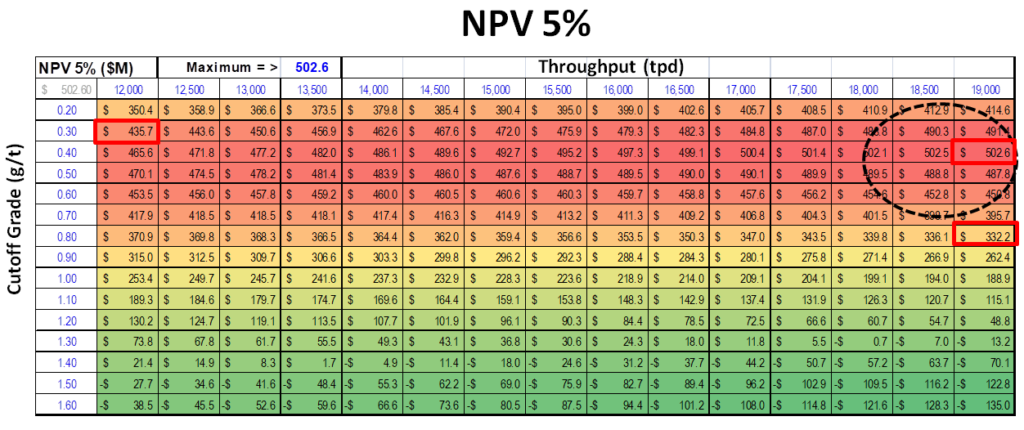

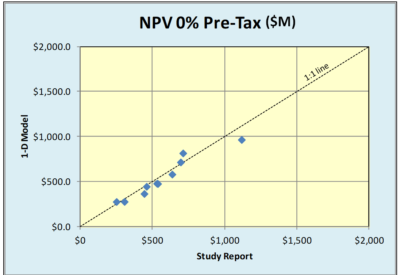

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model.

One of the questions I have been asked is how valid is the 1D approach compared to the standard 2D cashflow model. In order to examine that, I have randomly selected several recent 43-101 studies and plugged their reserve and cost parameters into the 1D model. There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

There is surprisingly good agreement on both the discounted and undiscounted cases. Even the before and after tax cases look reasonably close.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars.

Perhaps with technology, like Zoom, one can replicate the personal feel of a trade show booth. One can still have back and forth conversations with investors rather than just doing lecture style webinars. Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members.

Management teams should introduce more than just the CEO or COO. Include VP’s of geology, engineering, corporate development, from time to time. Don’t hesitate to let the public meet more of your team. Trade show booths are often manned by different team members. Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there.

Better communication with investors can increase confidence in a management team. Although some investors may not enjoy technical discussions, I think there is a subset that will find them very helpful and interesting. There will likely be an audience out there. As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

As an aside, if you are using Zoom make sure the host has configured the right settings. There are instances where anonymous participants can suddenly share their own computer screen, i.e. with questionable videos, to the group. It’s been referred to as “zoom bombing”.

The number of independent mining consultants is increasing daily as more people reach retirement age or are made redundant.

The number of independent mining consultants is increasing daily as more people reach retirement age or are made redundant. GLG (

GLG ( Digbee (

Digbee (

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due.

Reading it further, it was apparent that their study consultant, Ausenco, was being paid in company stock in lieu of cash. The arrangement included an initial financing of $750k with a further $375k to follow once the pre-feasibility study was 75% complete. Upon completion of the study another share payment was due. I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play.

I have never been in a situation where I was consulting with company shares as my compensation. Neither have I ever managed a study where outside consultants were being paid in shares. However I can see the possibility of interesting dynamics at play. Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now.

Regarding the first item “impartiality”, in the past there have been questions raised about the impartiality of engineering firms. I first recall reading this claim many years ago in a public response to a mining EIA application. Unfortunately I cannot find the exact source now. It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

It would be interesting to know how many consulting firms would be willing to accept compensation solely in shares. Stock prices move up and down and the outcome of the study itself can have an impact on share performance.

It’s always open to debate who these 43-101 technical reports are intended for. Generally we can assume correctly that they are not being written mainly for geologists. However if they are intended for a wider audience of future investors, shareholders, engineers, and C-suite management, then (in my view) greater focus needs to be put on the physical orebody description.

It’s always open to debate who these 43-101 technical reports are intended for. Generally we can assume correctly that they are not being written mainly for geologists. However if they are intended for a wider audience of future investors, shareholders, engineers, and C-suite management, then (in my view) greater focus needs to be put on the physical orebody description. I would like to suggest that every technical report includes more focus on the operational aspects of the orebody.

I would like to suggest that every technical report includes more focus on the operational aspects of the orebody. Improving the quality of information presented to investors is one key way of maintaining trust with investors. Accordingly we should look to improve the description of the mineable ore body for everyone. In many cases it is the key to the entire project.

Improving the quality of information presented to investors is one key way of maintaining trust with investors. Accordingly we should look to improve the description of the mineable ore body for everyone. In many cases it is the key to the entire project.

Each year business leaders are queried about what they view as their major risks. The survey results are summarized in the Global Risk Report.

Each year business leaders are queried about what they view as their major risks. The survey results are summarized in the Global Risk Report.

It is also interesting to look at the detailed 10 year table in the report to see how the risk perceptions have changed over the last decade.

It is also interesting to look at the detailed 10 year table in the report to see how the risk perceptions have changed over the last decade.

The mining industry will see positive impacts from digitalization. Unfortunately more reliance on technology also brings with it significant risks. These risks are related to cyber security.

The mining industry will see positive impacts from digitalization. Unfortunately more reliance on technology also brings with it significant risks. These risks are related to cyber security. As your mining company continues to move into the digital world, you must ask:

As your mining company continues to move into the digital world, you must ask: The bottom line is that there is no stopping the digitalization of the mining industry. It is here whether anybody likes it or not. At the same time, there is likely no stopping the growth of cyber crime.

The bottom line is that there is no stopping the digitalization of the mining industry. It is here whether anybody likes it or not. At the same time, there is likely no stopping the growth of cyber crime.